Breaking Down UBER Stock Ahead of Earnings

Trading 45% from its highs, investors will be closely watching Uber Technologies UBER Q3 earnings release on November 1. Investors and Wall Street alike will want to see if the company is getting closer to profitability amid a challenging operating environment for most companies.

At this stage in the company’s development, positive guidance, and a stronger outlook appears to be the main catalyst for the stock post-earnings. Uber was incorporated in 2009 and launched its IPO in 2019. Uber runs technology applications and platforms to enable independent providers of ridesharing services. In addition to this, Uber also incorporates delivery services and meal preparations to transact with riders and eaters.

The company has expanded its presence outside of the U.S. into multiple countries across the globe Latin America, Europe, the Middle East, and Asia. Investors hope that Uber’s aggressive expansion along with its food delivery service can help the stock continue to outpace competitor Lyft LYFT.

Image Source: Zacks Investment Research

Both stocks have struggled, but their Internet-Services Industry is currently in the top 31% of over 250 Zacks Industries. Uber investors hope the company can begin to capitalize on the re-emergence of ride-sharing post-pandemic. The rebounding ride-hailing business in addition to its Uber Eats service could help the stock bounce back and become the viable investment many still believe it can be.

Investors ultimately hope Uber can innovate like many other big tech companies with lofty visions and expansion goals such as Amazon AMZN and Netflix NFLX

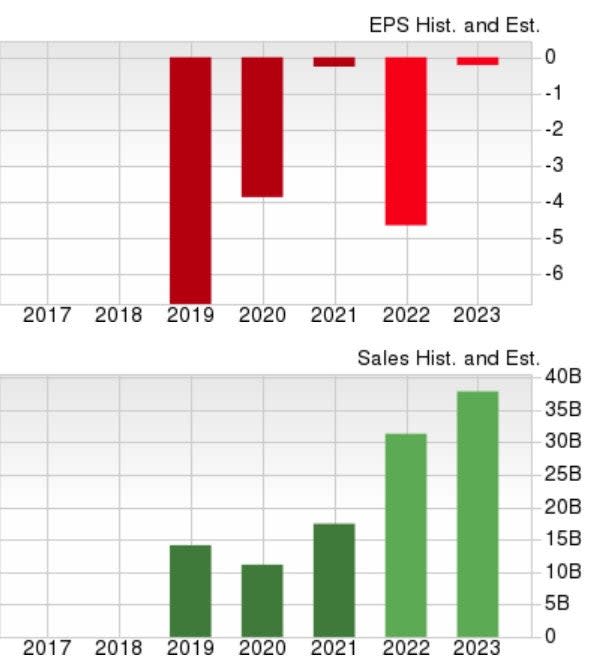

Road to Profitability

Uber is still looking ahead to its first profitable quarter. This year, higher gas prices have also weighed on the stock, as did the Omnicom variant earlier in the year.

Image Source: Zacks Investment Research

Last quarter, revenue grew 105% YoY to $8.1 billion but the company had a net loss of $2.6 billion. Uber had a $1.7 billion net headwind related to the company’s equity investments in Zomato, Aurora, and Grab.

Zomato is an Indian multinational restaurant aggregator and food delivery company. Aurora Innovation Inc. is an autonomous vehicle company that Uber has a $400 million stake in for 26% ownership. The company’s ownership is 40% when considering the stakes held by employees and investors of Uber’s autonomous driving division which was previously sold to Aurora. Lastly, Grab is a taxi-hailing app that includes ride-hailing, food, grocery, and package delivery. Uber’s stake in Grab increases its presence in Southeast Asia.

After these write-downs, Uber missed last quarter’s earnings expectations by -432% at -$1.33 compared to the expected -$0.25. Investors will be hoping that Uber’s expansion efforts will pay off once operating costs stabilize as the company has beaten sales expectations for five consecutive quarters. This makes the company’s outlook and guidance critical at this juncture.

Q3 Outlook

The Zacks Consensus Estimate for UBER’s Q3 earnings is - $0.17 per share, compared to -$0.23 in Q3 2021. Sales for Q3 are expected to be up 67% at $8.08 billion. Earnings estimates for the period have slightly gone up from -$0.18 at the beginning of the quarter.

Year over year, Uber earnings are expected to decline to -$4.64 compared to -$0.26 per share in 2021, due to its expansion efforts. However, FY23 earnings are expected to stabilize and rise 95% at -0.21 per share. Top line growth is expected, with sales projected to be up 81% this year and rise another 21% in FY23 to $38.26 billion.

Performance & Valuation

Year to date UBER is down -36% to underperform the S&P 500’s -19% and the Nasdaq’s-30%. Since its IPO three years ago, the stock is now down –15% to underperform the benchmark and the Nasdaq.

Image Source: Zacks Investment Research

UBER currently trades 41% below its IPO price of $45 per share. UBER does not have a P/E because the company is not profitable. Its price to sales (P/S) has become far more reasonable. UBER’s P/S is now 2.1X and far below its high of 10.4X over the last three years and the median of 4.7X. UBER also trades lower than the benchmark’s P/S of 3.5X.

Image Source: Zacks Investment Research

Bottom Line

UBER currently lands a Zacks Rank #3 (Hold) and the Average Zacks Price Target suggests 76% upside from current levels. The price of UBER shares is starting to look more attractive when considering where it traded in the past and the price investors are paying for its sales.

Investors will want to continue to monitor UBER’s path to profitably amid expansion efforts in a tougher operating environment. UBER does have strong revenue and could be a very viable investment if it can stabilize operation costs as the company matures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Uber Technologies, Inc. (UBER) : Free Stock Analysis Report

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Netflix, Inc. (NFLX) : Free Stock Analysis Report

Lyft, Inc. (LYFT) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research