The right retirement state of mind can boost your savings, analysis finds

Making decisions about retirement savings can feel monumental. But what if someone told you that, money aside, your mindset may be the magic elixir?

In a new report, Goldman Sachs Asset Management and Syntoniq, a behavioral finance research firm, surveyed 5,261 US workers and retirees and teased out four psychological factors that can close the gaps between your retirement savings goals and your future reality.

People who are highly optimistic, forward-looking with high financial literacy and who focus more on rewards than risks tend to have higher retirement savings than those on the opposite end of the spectrum, according to the research.

That positive mojo also translates to less angst about managing savings than those who don’t have high levels of those behaviors experience.

Read more: Retirement planning: A step-by-step guide

In reality, though, very few people have all four factors in their wheelhouse. Only a slim 10% of those surveyed do. Most people — 85% — possess a blend of these traits, the research found.

“Investing and savings psychology is important to understand because it helps explain ‘why’ people make certain financial decisions,” Chris Ceder, a senior retirement strategist with Goldman Sachs Asset Management, told Yahoo Finance.

According to the report, bright-eyed, glass-half-full types generally have a higher level of savings, are more likely to have their savings on track, and have a personalized financial plan for retirement. They review savings at least annually, have adequate emergency savings, and avoid retirement cash-outs when they change jobs. Meanwhile, they have no problem asking for help with their finances.

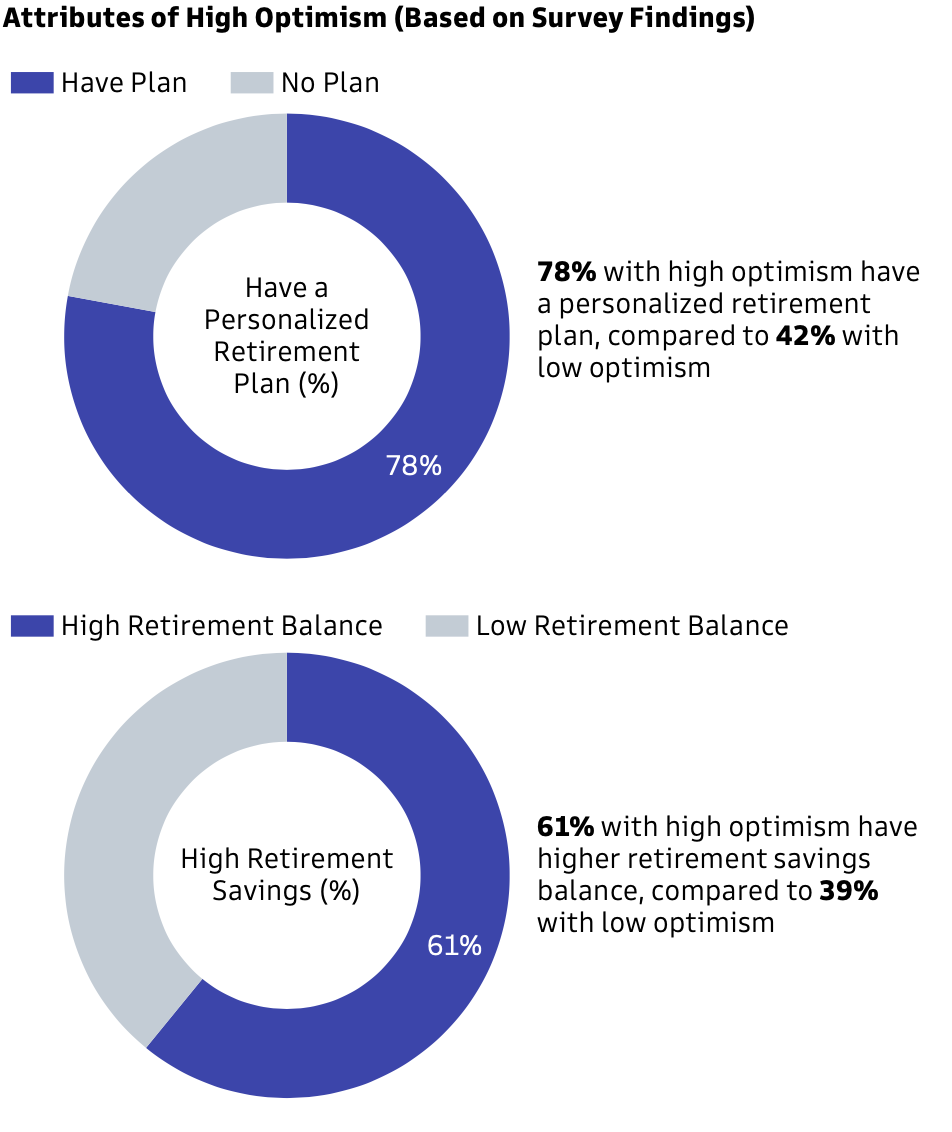

Although all four behavioral variables on their own contribute toward more robust retirement savings, high optimism tops the charts, according to the report.

Folks who are upbeat about their future are more apt to create a budget for today, live below their means, and are clear-eyed about the rewards that come from actively saving for the future, according to the data. Moreover, nearly 8 in 10 (78%) of highly optimistic people have a written personalized retirement plan versus 42% with low optimism.

These raging optimists step it up to actively manage their finances when there’s high inflation or when there’s considerable market volatility, according to the research. In fact, they’re more likely to change their investment allocation, hire a financial advisor, and add to their emergency savings accounts during those stressful times compared with those folks with low levels of optimism who tend to be passive.

Don’t stop believing

Those who wholeheartedly expect things to turn out well and believe that they have the ability to make good things happen are more likely to view their retirement savings as on track or ahead of schedule (83% vs 41%).

Forward-thinkers, like optimists, are more likely to maintain emergency savings and adjust their portfolios, for instance, if the economy hits headwinds, than people who live solely for today. Those without that future-tuned inner compass, for example, tend to cash out their retirement plans when they change jobs. And they're also more likely to say that credit card debt and monthly expenses interfere with retirement savings.

Knowledge is empowering

The report also links people with high financial literacy to having a better chance of meeting their retirement savings needs than those without that knowledge. That’s because financial literacy reflects a level of understanding of basic financial concepts, such as compound interest, inflation, and diversification, Ceder said. Those with high financial literacy report that they regularly review their retirement savings, have substantial emergency savings, and keep spending in check.

While that’s not terribly shocking, it’s a topic that gets a lot of attention these days.

“We don't learn by just absorbing and looking at the world around us,” Annamaria Lusardi, a senior fellow at the Stanford Institute for Economic Policy Research and co-author of the paper, “The Importance of Financial Literacy,” told me when I spoke to her at the Stanford Center on Longevity’s two-day 2023 Century Summit, where I also moderated a panel on navigating our financial futures. “This has to be a formal education starting as early as possible. I think actually it should start when the tooth fairy comes and you get the money.”

Many people don't even know what an interest rate is and cannot do a 2% calculation in the context of interest rate, she added.

“This level of knowledge is just as important today as reading and writing,” she said. “If you don't empower people with that basic knowledge, you can’t empower people to be financially secure.”

All good, but financial literacy that ups someone’s savings game needs to be personal, experts say. We need to make “education relevant to the individual’s circumstances and what they need to learn to make key decisions on their own retirement savings,” Ceder said.

Totally automatic

All of the behaviors this study pinpoints are certainly worth cultivating, but solving the lack of retirement readiness is a non-starter if people can’t or are unable to open an account.

One way is auto-enrollment —when a worker automatically contributes a percentage of pay into a 401(k) plan unless they opt out — which has been a huge success.

“Let's first automate as much of this financial literacy as possible,” Chris Farrell, one of the Stanford panelists and author of “Unretirement” and “Purpose and a Paycheck,” told me.

Read more: How much can you contribute to your 401(k) in 2024?

Plans with auto-enrollment had a 93% participation rate, compared with a participation rate of 70% for plans with voluntary enrollment, according to the “How America Saves 2023” report by Vanguard.

Employees who worked for companies that have auto-enrollment plans also saved more — an average of 11% of their paycheck — including both employee and employer contributions. Employees who had to make their own decision to enroll in a plan saved an average of 8% of their paycheck when combined with their employer’s match.

But those are the lucky Americans. Nearly half of US private-sector workers — roughly 57 million people — don’t have access to an employer-sponsored pension, such as a 401(k).

“And if you don't have access to an employer-sponsored retirement savings plan, you don't save for retirement,” Farrell said. “It's not because people don't want to be saving. It’s not because they're having that Starbucks coffee latte.”

The other thing is that life is hard, Farrell added.

“Look, you lose your job. You're taking care of aging parents. You have a medical issue, Your child is sick,” he said. “There are lots of interruptions throughout a life that really makes it hard for people to save.”

Ceder conceded that automating savings is vital, but financial literacy can’t be ignored if future financial security is at stake. Per Ceder, “the challenge with this perspective is if participants are defaulted throughout their retirement savings period, they will be ill-equipped to manage the financial challenges that often derail retirement savings.”

He added: “While default features are important to get people saving quickly, the goal should be to engage and prepare individuals to navigate the financial challenges they will face until and in retirement.”

Kerry Hannon is a Senior Reporter and Columnist at Yahoo Finance. She is a workplace futurist, a career and retirement strategist, and the author of 14 books, including "In Control at 50+: How to Succeed in The New World of Work" and "Never Too Old To Get Rich." Follow her on Twitter @kerryhannon.

Read the latest financial and business news from Yahoo Finance