How to Plan for Retirement if You're Self-Employed

The gig and freelancing economy are growing, which means for many, retirement planning looks different. While earning income on your own terms can be wonderful, there are some employer perks you miss out on — namely retirement accounts. There are retirement planning options available to keep you on track if you’re self-employed, though. Here’s what the experts suggest.

Related: How to Protect Yourself from Financial Ruin in Retirement

Some employers enroll employees automatically in their company 401(k) plan. This means company-employed workers often don’t even have to think about saving. When you’re self-employed, it helps to create behavioral reinforcements for yourself much as an employer would, says Rob Williams, managing director of financial planning at Schwab.

Related: The Worst Things No One Tells You About Retirement

Part of planning for retirement involves setting goals to design the life you want after you finish working. Self-employed workers should develop long-term goals and design a financial plan to achieve those objectives, says Matthew Fleming, a senior financial adviser with Vanguard Personal Advisor Services. For those who plan to retire early or want to support a more extravagant lifestyle, planning becomes even more important.

Related: Early Retirement Secrets and Strategies You Need to Know

As a business owner, there is a lot to keep track of, including taxes. “Take time to develop a baseline understanding of the tax code tools that are available to self-employed individuals for retirement savings. Focus on what you do well and ask for help in areas where you may lack expertise,” recommends John Trapani, a wealth adviser with Trapani Calvert, a Northwestern Mutual private client group.

Related: 11 Situations Where It's Probably a Bad Idea to Do Your Own Taxes

If you’re not sure how to plan for retirement, consider consulting a trusted adviser. “Meeting with a financial adviser can help you understand how to set yourself up for success both financially and entrepreneurially and help you understand the ins and outs of the overall process,” Trapani says. “When you have a plan, you [get] a better idea of how and where to invest your money and how your investments will impact you in the long run.”

Related: 14 Questions to Ask Before Hiring a Financial Adviser

Make a plan to maximize your earnings for retirement. With most retirement accounts, your contributions can’t exceed your business income. In some cases, contribution rules mean the more you earn, the more you may contribute, up to the amount determined by the Internal Revenue Service for each plan.

Related: 9 Myths About Early Retirement

When you’re first starting your own business, money can be tight. But retirement is an area where you don’t want to skimp. If saving for retirement feels impossible on a tight budget, don’t be discouraged. “The most important thing is to save regularly,” Williams says. “If you can’t save a lot, save a little.”

Related: 15 Ways Living in an RV Can Help You Retire Early

The reason it is so important to start saving early is compound interest, which builds money exponentially over time. “Time is one of the most important factors when it comes to building up your retirement fund. Regardless of the plan you choose, it’s important to get started as early as possible,” says Rita Assaf, vice president of Retirement Leadership at Fidelity Investments.

Related: 12 Reasons NOT to Retire Early

If you think you’re out of luck on tax-advantaged savings when you’re self-employed — those being IRAs, 401(k)s, and the like — think again. Being self-employed gives you more freedom in your retirement planning than most workers have. “Self-employed individuals have several options to choose from to help them save for retirement, all of which offer tax advantages,” Assaf says.

Related: 30 Money Mistakes You're Probably Making and How to Avoid Them

A traditional IRA is available to anyone getting taxable compensation, including business owners, freelancers, or gig workers. In fact, it is one of the simplest retirement plans available, and you can open one with many financial institutions. Those under 50 can contribute up to $6,000 to a traditional IRA in 2021; those 50 or older can go up to $7,000. As long as you are still working, there is no age limit to contributing to a traditional IRA, and if you don’t have a workplace retirement savings plan, your contribution might be fully tax-deductible.

Related: 10 Types of Retirement Accounts to Help Build Your Nest Egg

A Roth IRA is another option if you earn taxable compensation in the contribution year. This plan allows for post-tax contributions, regardless of age. Although there are no immediate tax benefits, you can withdraw contributions at any time without penalty. And when retirement arrives, qualified withdrawals are tax free — making this plan typically best when you expect your income tax rate to be higher in retirement than now. Whether and how much you can contribute to a Roth depends on income and filing status, and high earners might not be eligible. You can save up to $6,000 yearly if you are under 50, and $7,000 if you are 50 or older.

For more smart retirement tips tips, please sign up for our free newsletters.

Many experts agree an individual or solo 401(k) is ideal if you’re self-employed, with no employees except a spouse. Contributions are pretax, and the money grows tax-deferred, meaning you pay when you make withdrawals in retirement. “Your contributions may also make you eligible for added tax breaks,” Assaf says. “If your business is not incorporated, you can generally deduct contributions for yourself from your personal income. If your business is incorporated, you can count the contributions as a business expense.” Further, when you’re self-employed, you are considered both the employer and employee and can contribute more as a result: As an employer, as much as 25% of your salary; as an employee, up to $19,500 a year. (Plus an additional $6,500 if you’re over 50.) You can contribute only up to 100% of your compensation, Williams says, but the combined maximum tax-advantaged contribution this year is $58,000.

Related: 31 Tax Credits and Deductions That Could Save You Thousands

The difference to an individual Roth 401(k) is when you’ll see the tax break: Roth solo 401(k) contributions are made with after-tax dollars. There are no immediate tax benefits, but you can make qualified withdrawals tax-free after reaching age 59½ as long as you’ve had the account for at least five years. Also, you cannot double up on contributions, and if you have a traditional 401(k) and a Roth 401(k), your total contributions between the two cannot exceed $58,000 in 2021. Keep in mind: If you contribute any money to a 401(k) through an employer, this amount also counts toward the $58,000 max.

The SIMPLE in this retirement savings plan stands for Savings Incentive Match Plan for Employees, but Williams says it’s also simple to set up and administer — and best for small businesses with up to 100 employees. “Penalties may be more severe for withdrawals from SIMPLE IRAs before age 59½ than those for 401(k)s or SEP IRAs,” Williams notes, and compared with a solo 401(k), employee contribution limits are relatively low: $13,500 a year, plus another $3,000 in catch-up contributions if you are 50 or older. Another major drawback is that employers are required to contribute every year. IRS regulations require making a matching contribution up to 3% of compensation (not limited by the annual compensation limit), or a 2% nonelective contribution for each eligible employee.

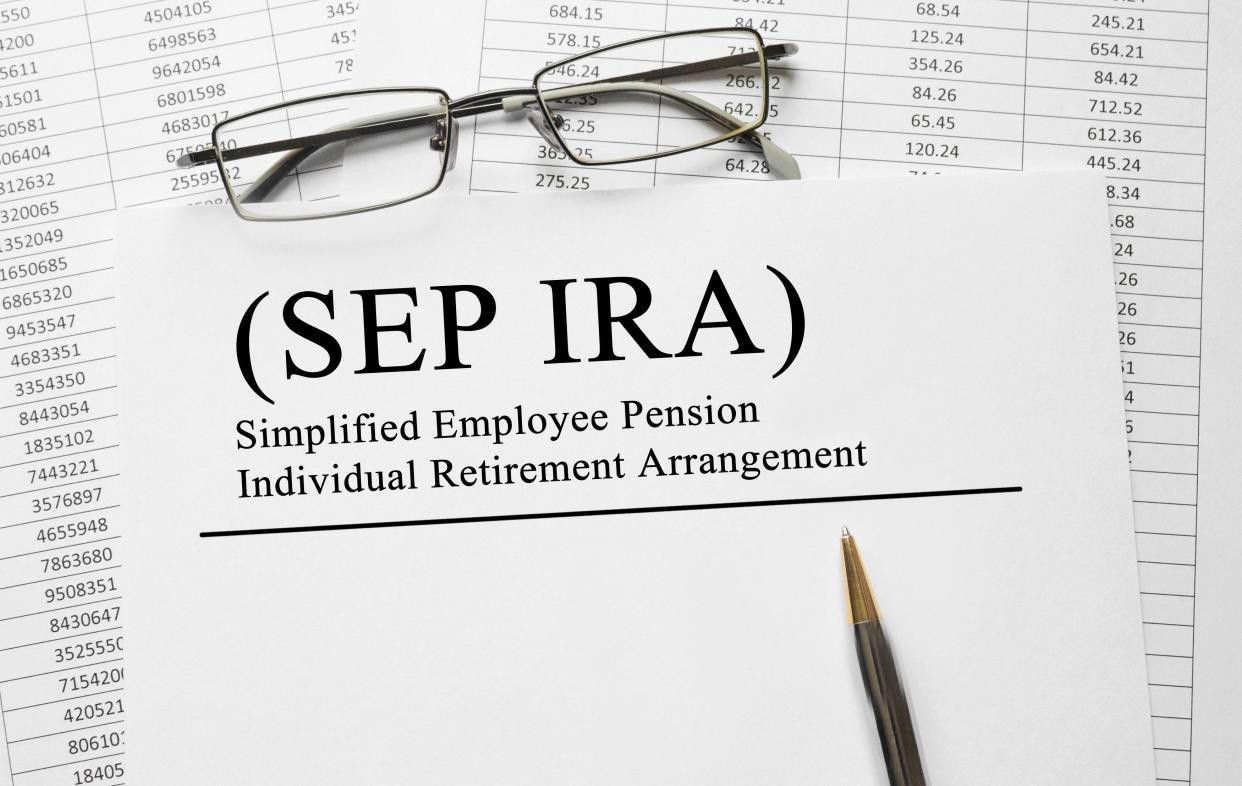

A Simplified Employee Pension plan allows for tax-deferred retirement savings and is good for those who are self-employed or have income from freelancing and for businesses with less than 20 employees, Assaf says. One major benefit is flexibility: You don’t have to contribute every year as you do with a SIMPLE IRA, so if you hit a rough patch in your business you can decrease or pause contributions. If you have employees who want to contribute a portion of their income, the SEP IRA may not be the best choice, though, because only employers pay in. If you’re self-employed, you can contribute the lesser of 20% of your earnings or $58,000 a year in 2021, but if you contribute for yourself in a year, you must contribute the same percentage of salary to each eligible employee's account as well.

A personal defined benefit plan essentially acts as your own pension, and involves a much more complicated startup process and higher administrative costs than most other plans. “You set the benefit you want in retirement and then hire an actuary to determine your annual contributions based on age and expected investment returns,” Williams says. Then comes a set schedule of contributions you must follow, making it much less flexible than a solo 401(k). But if you want to contribute large sums to your nest egg and have the stable cash flow to do so, these plans allow for up to $230,000 yearly as a pension. That would exceed the contribution limitations of other self-employment retirement plans.

Related: 20 Painless Ways to Grow Your Emergency Fund

This is not technically a retirement account, but offers tax benefits before and during retirement. If you have a high-deductible health plan, you can set aside money pretax for an HSA and take tax-free withdrawals to pay for medical expenses. If you don’t need the money for medical expenses, you can withdraw it and pay taxes (but no penalties) after age 65. You can contribute up to $3,600 yearly as an individual or up to $7,200 for a family. You can even contribute to an HSA if you have no earned income, which differs from traditional retirement plans available to self-employed individuals. Once you enroll in Medicare, you are no longer eligible to contribute, so plan accordingly.