'Excess savings' are just regular savings now

This is The Takeaway from today's Morning Brief, which you can sign up to receive in your inbox every morning along with:

The chart of the day

What we're watching

What we're reading

Economic data releases and earnings

As the pandemic-era economy recedes from view, some of the frameworks that defined this moment have been abandoned.

Demand is just demand, rather than pent-up demand.

Supply chain problems are just supply chain problems — see: the Mississippi River's record low levels — rather than an outgrowth of pandemic-created economic whiplash.

And now the concept of consumer savings is no longer being seen as one defined by "excess" — either consumers have savings or they don't.

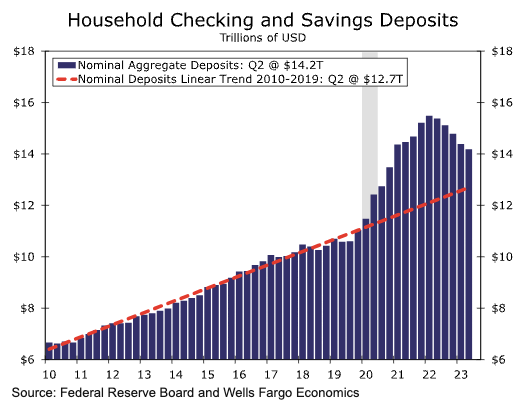

In a note to clients on Thursday, economists at Wells Fargo led by Tim Quinlan wrote the firm will move away from thinking about the concept of "excess savings" from US consumers and trying to estimate how long these savings will last.

Instead, the firm plans to focus on measuring aggregate household checking and savings account balances relative to pre-pandemic trends.

"For many households, the excess savings is long gone," the firm wrote.

"For others, especially wealthy ones, it can last much longer. If you don’t draw the money down, it can last indefinitely. ... Whatever the measure, excess liquidity will be less of a driver of spending going forward."

Wells Fargo's decision to move on from estimates of how quickly savings have been spent was largely spurred by recent revisions to government data that changed prior estimates on how much in "excess savings" was left in the economy by roughly $700 billion.

As the firm wrote: "... it is not sensible to hang your hat on an estimate subject to such comically large revisions. Households still have excess savings upon which to fund spending and that pool of money is getting smaller. This insight need not rely upon data subject to such massive revisions."

The concept of "excess savings" was always a murky one. And as the pandemic's fog lifts from the economy, these uniquely variable variables become less essential to understanding where things stand.

This shift also brings in a more straightforward framework for understanding the economy than what was required so often in the months and years after the pandemic's most acute impacts.

In the first Morning Brief of 2023, we explored estimates from economists about how much of this pandemic-era "excess savings" had been spent and how much remained in consumers' coffers. But the kicker in that post cited work from Pantheon Macroeconomics' Ian Shepherdson, who argued the labor market — rather than accumulated cash from stimulus programs and other forced lifestyle changes — would be the biggest influence on consumer habits.

And this has largely borne out, if perhaps not quite on the same timeline as many had expected when 2022 turned to 2023.

For much of this year, the labor market remained more resilient than expected. In turn, so did consumer spending. And softening in the labor market in recent months has drawn attention as a potential sign the US economy's long-anticipated recession may finally be nearing.

"If the labor market retreats as we have in our forecast," Wells Fargo wrote, "that would clearly limit the capacity of consumer spending and would contribute to the mild contraction in Personal Consumption Expenditures that we have in our forecast."

The firm expects spending to fall at an annualized rate in each of the first two quarters next year with the economy losing jobs in the second and third quarters of 2024.

The timing and magnitude of the economy's shifts in the year ahead matter less, however, than a restoration of the relationship between employment, spending, and growth.

After nearly three years in which unprecedented fiscal stimulus left many economic models about how these variables interact largely inert, something resembling order has been slowly restored to Wall Street's macro conversation.

Click here for the latest stock market news and in-depth analysis, including events that move stocks

Read the latest financial and business news from Yahoo Finance