Did 401(k)s Replace Pension Plans? (& Which Is Better For You?)

401(k) vs Pension Plan: Differences and Which is Better For You

A 401(k) plan is a retirement savings plan in which employees contribute to a tax-deferred account via paycheck deductions (and often with an employer match). A pension plan is a different kind of retirement savings plan in which a company sets money aside to give to future retirees.

Over the past few decades, defined-contribution plans like the 401(k) have steadily replaced pension plans as the private-sector, employer-sponsored retirement plan of choice. While both a 401(k) plan and a pension plan are employer-sponsored retirement plans, there are some significant differences between the two.

What Is the Difference Between a Pension and a 401(k)?

The main distinction between a 401(k) vs. a pension plan is that pension plans are largely employer driven, while 401(k)s are employee driven.

These are some of the key differences between the two plans.

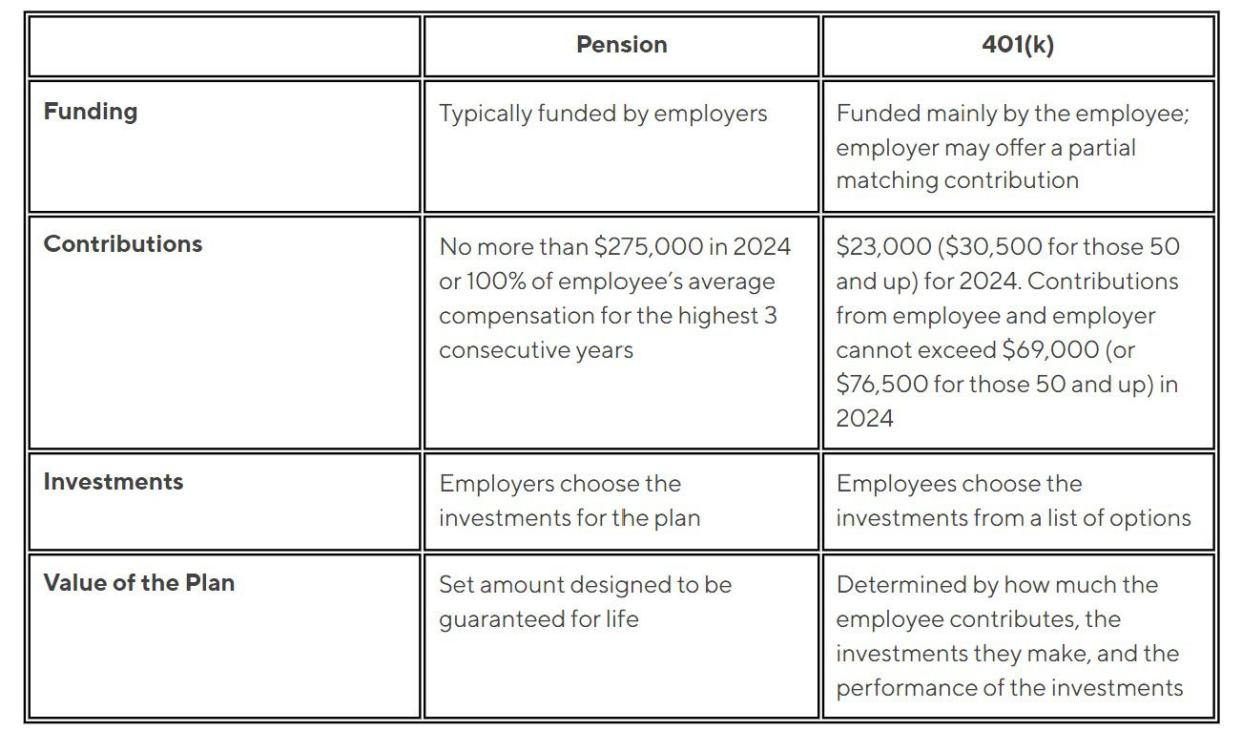

Funding

Employees typically fund 401(k) plans through regular contributions from their paychecks to help save for retirement, while employers typically fund pension plans.

Investments

Employees can choose investments (from several options) in their 401(k). Employers choose the investments that fund a pension plan.

Value

The value of a 401(k) plan at retirement depends on how much the employee has saved, in addition to the performance of the investments over time. Pensions, on the other hand, are designed to guarantee an employee a set amount of income for life.

Pension Plan Overview

A pension plan is a type of retirement savings plan where an employer contributes funds to an investment account on behalf of their employees. The earnings are paid out to the employees once they retire.

Types of Pension Plans

There are two common types of pension plans:

Defined-benefit pension plans, also known as traditional pension plans, are the most common type of pension plans. These employer-sponsored retirement investment plans are designed to guarantee the employee will receive a set benefit amount upon retirement (usually calculated with set parameters, i.e. employee earnings and years of service). Regardless of how the investment pool performs, the employer guarantees pension payments to the retired employee. If the plan assets aren’t enough to pay out to the employee, the employer is typically on the hook for the rest of the money. According to the IRS, contributions to a defined-benefit pension plan cannot exceed 100% of the employee’s average compensation for the highest three consecutive calendar years of their employment or $265,000 for tax year 2023 and $275,000 for 2024.

Defined-contribution pension plans are employer-sponsored retirement plans to which employers make plan contributions on their employee’s behalf and the benefit the employee receives is based solely on the performance of the investment pool. Meaning: There is no guarantee of a set monthly payout.

Like 401(k) plans, employees can contribute to these plans, and in some cases, employers match the contribution made by the employee. Unlike defined-benefit pension plans, however, the employee is not guaranteed a certain amount of money upon retirement. Instead, the employee receives a payout based on the performance of the investments in the fund.

When it comes to pension plan withdrawals, employees who take out funds before the age of 59 ½ must pay a 10% early withdrawal penalty as well as standard income taxes. This is similar to the penalties and taxes associated with early withdrawal from a traditional 401(k) plan.

Pros and Cons

There are benefits to and drawbacks of pension plans. It’s important to understand both in order to maximize your participation in the plan.

Advantages of a pension plan include:

Funded by employers

For employees, a pension plan is retirement income from your employer. In most cases, an employee does not need to contribute to a defined-benefit pension plan in order to get consistent payouts upon retirement.

Higher contribution limits

When compared to 401(k)s, defined-contribution pension plans have significantly higher contribution limits and, as such, present an opportunity to set aside more money for retirement.

A set amount in retirement

A pension plan typically provides employees with regular fixed payments in retirement, usually for life.

Disadvantages of a pension plan include:

Lack of control

Employees can’t choose how the money in a pension plan is invested. If the investments don’t pan out, the plan could struggle to pay out the funds.

Vesting

Employees may need to work for the employer for a set number of years to become fully vested in the plan. If you leave the company before then, you might end up forfeiting the pension funds. Find out what the vesting schedule is for your pension plan.

Earnings and years employed

How much an employee gets in retirement with a pension plan generally depends on their salary and how long they work for the employer.

401(k) Overview

A traditional 401(k) plan is a tax-advantaged defined-contribution plan where workers contribute pre-tax dollars to the investment account via automatic payroll deductions. These contributions are sometimes fully or partially matched by their employers, and withdrawals are taxed at the participant’s marginal tax rate.

With a 401(k), employees and employers may both make contributions to the account (up to a certain IRS-established limit), but employees are responsible for selecting the specific investments. They can typically choose from offerings from the employer, which may include a mixture of stocks and bonds that vary in levels of risk depending on when they plan to retire.

Contribution Limits and Withdrawals

To account for inflation, the IRS periodically adjusts the maximum amount an employer or employee can contribute to a 401(k) plan.

For 2024, annual employee contributions can’t exceed $23,000 for workers under 50, and $30,500 for workers 50 and older (this includes a $7,500 catch-up contribution). The total annual contribution by employer and employee in 2024 is capped at $69,000 for workers under 50, and $76,500 for workers 50 and over.

For 2023, annual employee contributions can’t exceed $22,500 for workers under 50, and $30,000 for workers 50 and older (this includes a $7,500 catch-up contribution). The total annual contribution paid by employer and employee in 2023 is capped at $66,000 for workers under 50, and $73,500 for workers 50 and over.

Some plans allow employees to make additional after-tax contributions to their 401(k) plan, within the contribution limits outlined above.

Money can be withdrawn from a 401(k) in retirement without penalties. But taxes will be owed on the funds withdrawn. The IRS considers the removal of 401(k) funds before the age of 59 ½ an “early withdrawal.” The penalty for removing funds before that time is an additional tax of 10% of the withdrawal amount (there are exceptions, notably a hardship distribution, where plan participants can withdraw funds early to cover “immediate and heavy financial need”).

Pros and Cons

While a 401(k) plan might not offer as clearly-defined a retirement savings picture as a pension plan, it still comes with a number of upsides for participants who want a more active role in their retirement investments.

Advantages of a 401(k) include:

Self-directed investment opportunities

Unlike employer-directed pension plans, in which the employee has no say in the investment strategy, 401(k) plans offer participants more control over how much they invest and where the money goes (within parameters set by their employer). Plans typically offer a selection of investment options, including mutual funds, individual stocks and bonds, exchange traded funds (ETFs).

Tax advantages

Contributions to a 401(k) come from pre-tax dollars through payroll deductions, reducing the gross income of the participant, which may allow them to pay less in income taxes. Also, 401(k) contributions and earnings in the plan may grow tax-deferred.

Employer matching

Many 401(k) plan participants are eligible for an employer match up to a certain amount, which essentially means free money.

Disadvantages of a 401(k) include:

No guaranteed amount in retirement

How much you have in your 401(k) by retirement depends on how much you contributed to the plan, whether your employer offered matching funds, and how the investments you chose fared.

Contributions are capped

The amount you can contribute to a 401(k) annually is capped by the IRS, as described above.

Less stability

How the market performs generally affects the performance of 401(k) investments. That could make it difficult to know how much money you’ll have for retirement, which could complicate retirement planning.

Which Is Better, a 401(k) or a Pension Plan?

When considering a 401(k) vs. pension, most people prefer the certainty that comes with a pension plan.

But for those who seek more control over their retirement savings and more investment vehicles to choose from, a 401(k) plan could be the more advantageous option.

In the case of the 401(k), it really depends on how well the investments perform over time. Without the safety net of guaranteed income that comes with a pension plan, a poorly performing 401(k) plan has a direct effect on a retiree’s nest egg.

Did 401(k)s Replace Pension Plans?

The percentage of private sector employees whose only retirement account is a defined benefit pension plan is just 4% today, versus 60% in the early 1980s. The majority of private sector companies stopped funding traditional pension plans in the last few decades, freezing the plans and shifting to defined-contribution plans like 401(k)s.

When a pension fund isn’t full enough to distribute promised payouts, the company still needs to distribute that money to plan participants. In several instances in recent decades, pension fund deficits for large enterprises like airlines and steel makers were so enormous they required government bailouts.

To avoid situations like this, many of today’s employers have shifted the burden of retirement funding to their workers.

What Happens to a 401(k) or Pension Plan If You Leave Your Job?

With a 401(k), if you leave your job, you can take your 401(k) with you by rolling it over to your new employer’s 401(k) plan or into an IRA. The process is fairly easy to do.

If you leave your job and you have a pension plan, however, the plan generally stays with your employer. You’ll need to keep track of it through the years and then apply in retirement to begin receiving your money.

The Takeaway

Pension plans are employer-sponsored, employer-funded retirement plans that are designed to guarantee a set income to participants for life. On the other hand, 401(k) accounts are employer-sponsored retirement plans through which employees make their own investment decisions and, in some cases, receive an employer match in funds. The post-retirement payout varies depending on market fluctuations.

While pension plans are far more rare today than they were in the past, if you have worked at a company that offers one, that money will still come to you after retirement even if you change jobs, as long as you stayed with the company long enough for your benefits to vest.

Some people have both pensions and 401(k) plans, but there are also other ways to take an active role in saving for retirement. An IRA is an alternative to 401(k) and pension plans that allows anyone to open a retirement savings account. IRAs have lower contribution limits but a larger selection of investments to choose from. And it’s possible to have an IRA in addition to a 401(k) or pension plan.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

SoFi Invest®

INVESTMENTS ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE

SoFi Invest encompasses two distinct companies, with various products and services offered to investors as described below: Individual customer accounts may be subject to the terms applicable to one or more of these platforms.

1) Automated Investing and advisory services are provided by SoFi Wealth LLC, an SEC-registered investment adviser (“SoFi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC.

2) Active Investing and brokerage services are provided by SoFi Securities LLC, Member FINRA (www.finra.org)/SIPC(www.sipc.org). Clearing and custody of all securities are provided by APEX Clearing Corporation.

For additional disclosures related to the SoFi Invest platforms described above please visit SoFi.com/legal.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform.

Investment Risk: Diversification can help reduce some investment risk. It cannot guarantee profit, or fully protect in a down market.

Exchange Traded Funds (ETFs): Investors should carefully consider the information contained in the prospectus, which contains the Fund’s investment objectives, risks, charges, expenses, and other relevant information. You may obtain a prospectus from the Fund company’s website or by email customer service at investsupport@sofi.com. Please read the prospectus carefully prior to investing.

Shares of ETFs must be bought and sold at market price, which can vary significantly from the Fund’s net asset value (NAV). Investment returns are subject to market volatility and shares may be worth more or less their original value when redeemed. The diversification of an ETF will not protect against loss. An ETF may not achieve its stated investment objective. Rebalancing and other activities within the fund may be subject to tax consequences.