One way to look at crypto from a macro investor perspective

This post was originally published on TKer.co

Stocks rallied last week, with the S&P 500 surging 5.9%. The index is now up 11.6% from its October 12 closing low of 3,577.03 and down 16.8% from its January 3 closing high of 4,796.56.

A big driver of the recent market move was Thursday’s cooler-than-expected consumer price index (CPI) report, which was followed by one of the biggest single-day stock market rallies in history. (More on the CPI report below.)

But with last week’s sudden and spectacular implosion of crypto exchange FTX, I thought I’d share some thoughts on cryptocurrencies and blockchain.

Ever since Bitcoin made mainstream news about a decade ago, I’ve done my best to read up on cryptos and blockchain technology. Unfortunately, I’m not sure I totally understand what the big deal is.

I believe blockchain represents a technological breakthrough, and I’m convinced there’s some value in being able to own and exchange digital objects that can’t be copied.

I’m just not convinced there’s an urgent need for any of this. If there were, I’d think there’d be much wider adoption. But the individuals and entities going all-in on cryptos and blockchain are largely detached from anything that matters to me.

That said, I’m also not convinced that cryptos and blockchain will never matter. There may be a day that this technology becomes central to how assets and information are exchanged.

But I also don’t think you need to own a bunch of today’s cryptocurrencies and invest in today’s blockchain companies to benefit. If the technology is indeed all it’s cracked up to be, then everyone should eventually gain from cost savings and reduced frictions across the economy.

As far as the price swings in cryptocurrencies are concerned, here’s an analogy that I think I’m happy with: Blockchain is like the internet and cryptocurrencies are like websites. During the advent of the internet, there were lots of internet companies you could invest in and there were lots of websites you could visit. Today, everybody uses the internet and everybody visits a lot of websites. But a lot of the early internet companies have gone bust and a lot of yesterday’s popular websites aren’t popular today. Maybe some of today’s cryptocurrencies will become tomorrow’s Amazon or Google, but many will also go down like Pets.com or Webvan.

A quick note about fraud: Anything that looks like a financial opportunity is going to come with a lot of crooks who’ll take advantage of those attracted by the prospect of getting rich quick. But the existence of crooks in the crypto world doesn’t necessarily mean that crypto itself is problematic. It just means that there needs to be more education and probably some regulation.

In summary, I think blockchain technology is interesting, but I don’t think the need is urgent. And just because you don’t own a bunch of cryptocurrencies and you don’t invest in a bunch of blockchain companies doesn’t mean you won’t benefit should the technology become widely adopted.

Reviewing the macro crosscurrents 🔀

There were a few notable data points from last week to consider:

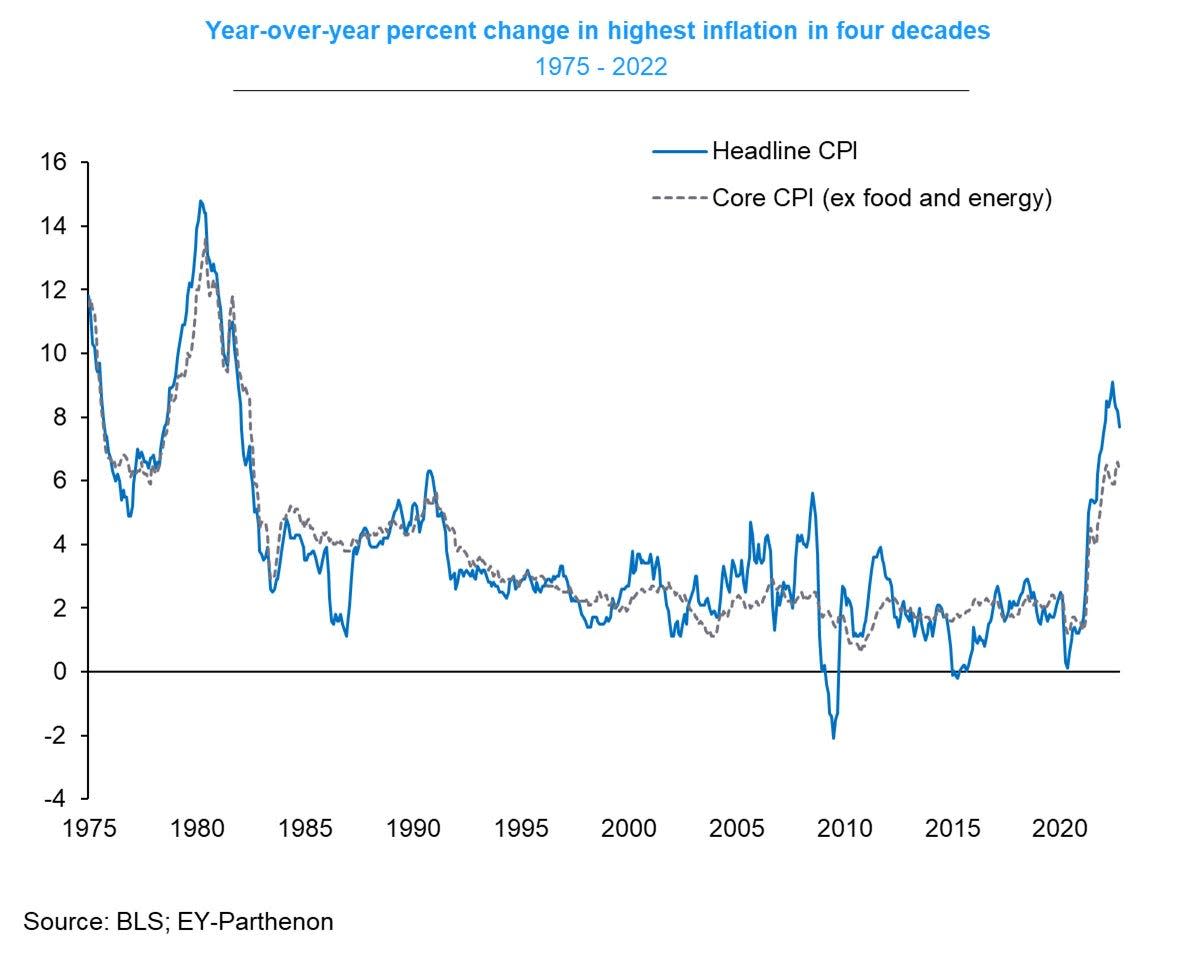

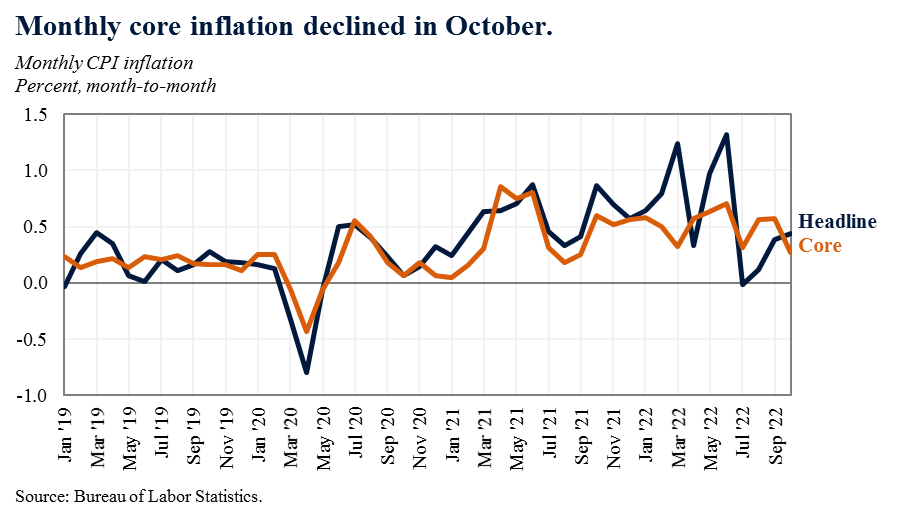

🚨 Inflation cools a bit. The consumer price index (CPI) in October was up 7.7% from a year ago. Adjusted for food and energy prices, core CPI was up 6.3%. Both measures were down from September levels and both were cooler than economists’ expectations.

On a month-over-month basis, CPI was up 0.4% and core CPI was up 0.3%. Again, both measures were cooler than expected.

Core services prices cooled and core goods prices fell.

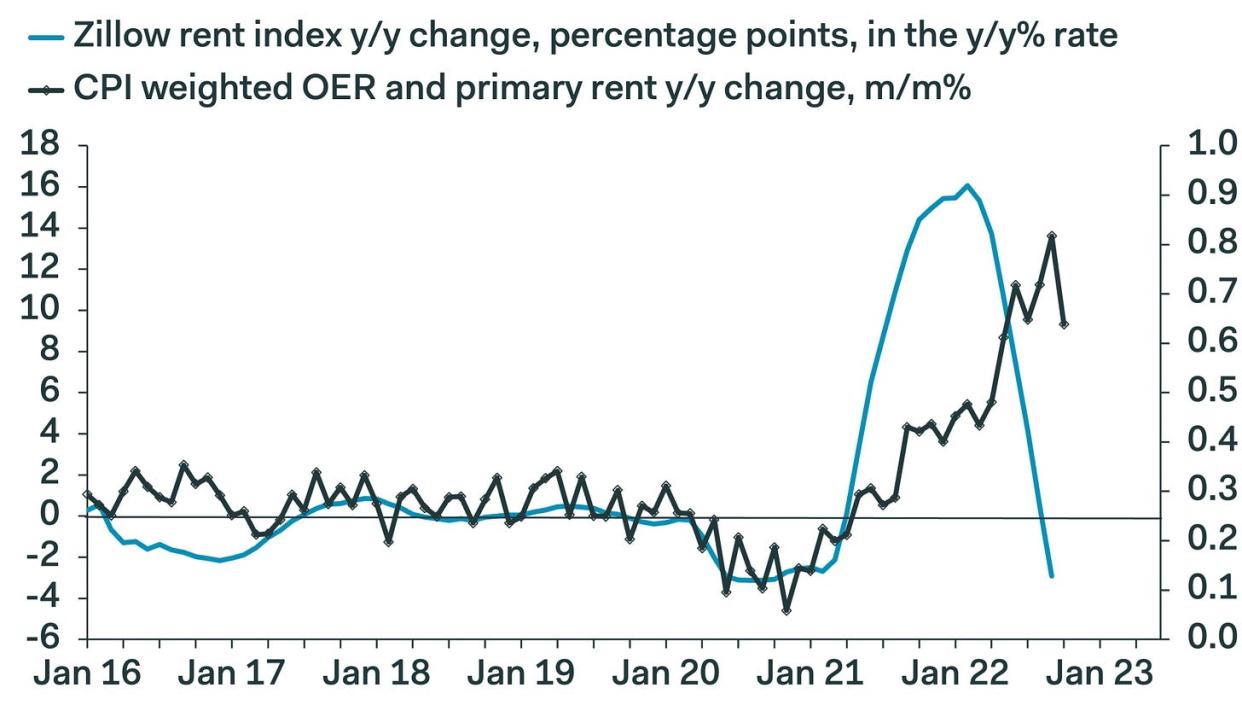

Rent of primary residence (a.k.a., tenants’ rent) and owners’ equivalent rent (i.e., how much a homeowner would have to pay to rent their currently owned home) cooled a bit as they catch up with the decline in market rents.

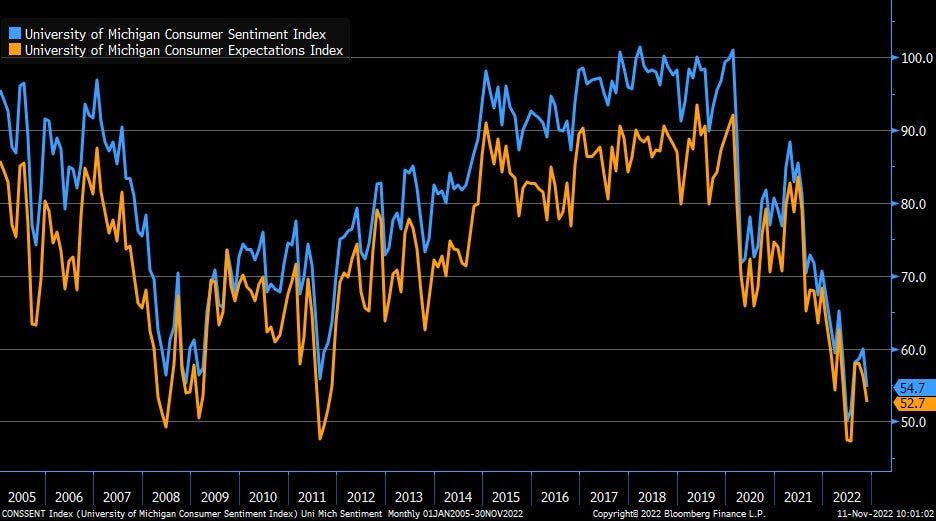

😞 Consumer sentiment is deteriorating again. From the University of Michigan’s November Survey of Consumers: “Consumer sentiment fell about 9% below October, erasing about half of the gains that had been recorded since the historic low in June. All components of the index declined from last month, but buying conditions for durables, which had markedly improved last month, decreased most sharply in November, falling back 21% on the basis of high interest rates as well as continued high prices. Overall, declines in sentiment were observed across the distribution of age, education, income, geography, and political affiliation, showing that the recent improvements in sentiment were tentative. Instability in sentiment is likely to continue, a reflection of uncertainty over both global factors and the eventual outcomes of the election.“

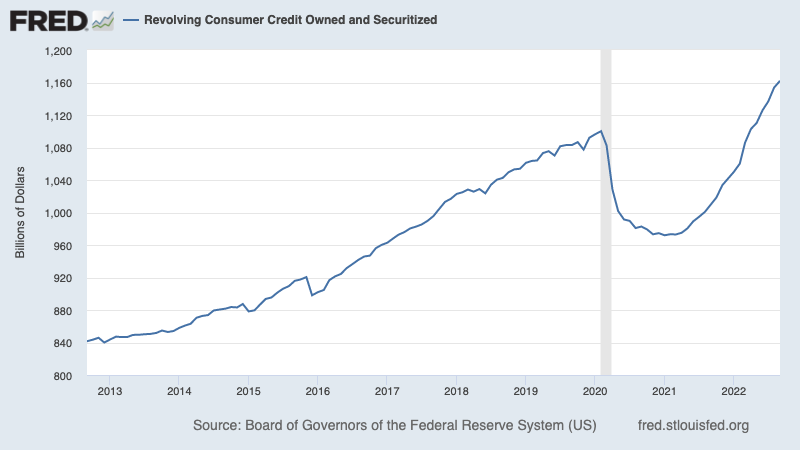

💳 Consumers are taking on more debt. According to Federal Reserve data, total revolving consumer credit outstanding increased to $1.16 trillion in September. Revolving credit consists mostly of credit card loans.

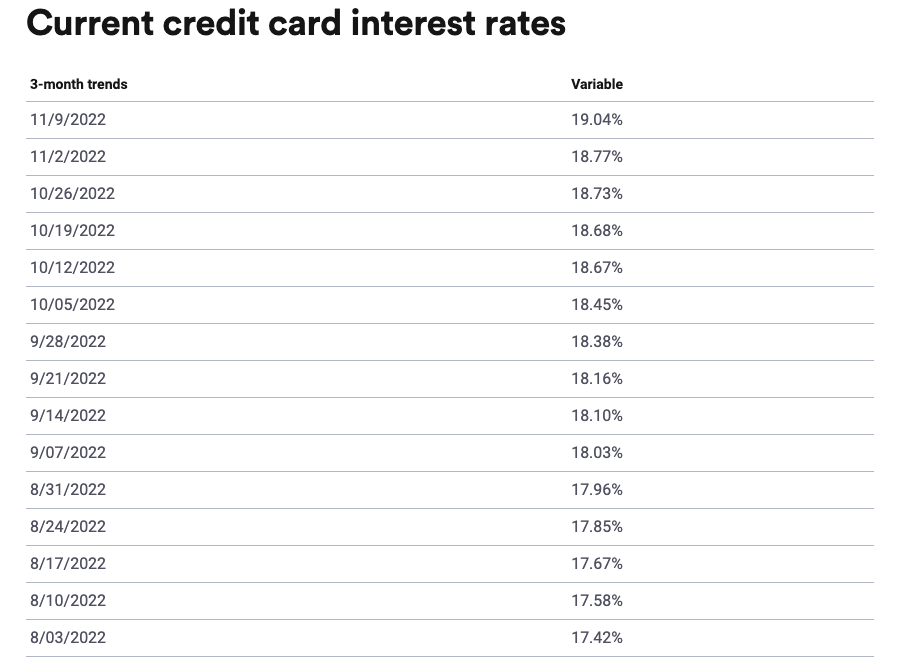

📈 Credit card rates are rising. From CNN Business: “The Federal Reserve’s war on inflation has driven up the average credit card APR (annual percentage rate) to 19.04% as of November 9, according to Bankrate.com. That’s the highest rate since Bankrate.com’s database began in 1985, beating the prior record of 19% set in July 1991.“

😞 It’s getting harder to borrow: According to Federal Reserve’s Senior Loan Officer Opinion Survey, bank lending standards got significantly tighter during Q3.

👎 Personal bankruptcies are ticking up. From Axios: “ In October, there were 14,161 new cases, a 27% increase from the same month a year ago, according to Epiq Bankruptcy Analytics. Yes, but: Don't fret about the state of the American consumer just yet — bankruptcy filings remain far below pre-pandemic norms. Back in 2019, the monthly average was 23,570, or about 66% higher than last month's tally.“

🛍 Consumers still expect to shop this holiday season. From the National Retail Federation: “Holiday spending is expected to be healthy even with recent inflationary challenges, as the National Retail Federation today forecast that holiday retail sales during November and December will grow between 6% and 8% over 2021 to between $942.6 billion and $960.4 billion. Last year’s holiday sales grew 13.5% over 2020 and totaled $889.3 billion, shattering previous records. Holiday retail sales have averaged an increase of 4.9% over the past 10 years, with pandemic spending in recent years accounting for considerable gains.“ From NRF CEO Matthew Shay: “In the face of these challenges, many households will supplement spending with savings and credit to provide a cushion and result in a positive holiday season.“

⏳ But they’re waiting for a deal. From Morgan Stanley: “Consumers are waiting for a deal; 70% of shoppers said they are waiting for stores to offer discounts before they begin their holiday shopping (Exhibit 7). Shoppers are looking to see substantial discounts before they begin spending; 30% of shoppers are waiting for 10% - 20% discounts while 27% are looking for 21% - 30% discounts. In the absence of last year’s supply issues consumers will have plenty of choices this year and will feel free to shop around for the best prices. Stores offering the best deals will be able to grab the largest wallet share but at a hit to margins.“

🛍Holiday sales are off to a slow start. From BofA: “In fact, holiday sales, which include categories that usually receive a big boost in sales during the winter holidays such as clothing and electronics, continue to show some weakness in goods spending for the winter holiday season relative to last year (Exhibit 3).“

💼 Unemployment claims remain low.Initial claims for unemployment benefits rose to 225,000 during the week ending Nov. 5, up from 218,000 the week prior. While the number is up from its six-decade low of 166,000 in March, it remains near levels seen during periods of economic expansion.

📋 Small businesses say labor shortages continue. From the NFIB’s Bill Dunkelberg: “Inflation, supply chain disruptions, and labor shortages continue to limit the ability of many small businesses to meet the demand for their products and services.“

Putting it all together 🤔

While inflation appears to be cooling, it continues to be very hot. So we should expect the Federal Reserve to continue to tighten monetary policy, which means tighter financial conditions (e.g. higher interest rates and tighter lending standards). All of this means the market beatings will continue and the risk the economy sinks into a recession will intensify.

On the matter of recession risks, consumers are increasingly stretching their finances to maintain their spending. They’re accumulating more debt and a growing number of these folks are entering bankruptcy.

But it’s important to remember that while consumer finances may be deteriorating, they are coming from a very strong position. Many still have excess savings to tap into and the labor market continues to be very favorable for workers. So it’s too early to sound the alarm on the consumer.

Overall, any downturn won’t turn into economic calamity given that the financial health of consumers and businesses remains very strong.

And as always, long-term investors should remember that recessions and bear markets are just part of the deal when you enter the stock market with the aim of generating long-term returns. While markets have had a terrible year so far, the long-run outlook for stocks remains positive.

This post was originally published on TKer.co

Sam Ro is the founder of TKer.co. Follow him on Twitter at @SamRo

Click here for the latest stock market news and in-depth analysis, including events that move stocks

Read the latest financial and business news from Yahoo Finance

Download the Yahoo Finance app for Apple or Android

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, and YouTube