The Fed is rethinking how it plans on handling the next crisis

With the Federal Reserve on pause with interest rates at the low level of 2.25% to 2.5%, Fed officials are starting to wonder: Is the central bank ill-equipped to deal with the next crisis? And would negative interest rates be an effective tool?

When the financial crisis began in 2007, the Federal Reserve had a 5.25% target interest rate to work with. By the end of 2008, the Fed had lowered interest rates as much as it could lower them — to zero — and turned to large-scale asset purchases through quantitative easing in an attempt to further stimulate the economy.

With many policymakers estimating that rates are currently at the neutral level that the economy can handle, it looks unlikely that the Fed will have as large a buffer as it did in 2007 if it confronts another crisis. And with lingering questions about the effectiveness of quantitative easing, Fed watchers are calling on the central bank to seriously rethink its strategy before the next downturn arises.

“I would lose sleep at night worrying that this fragile strategy is the one the economy is depending on,” Dartmouth professor Andrew Levin said at a monetary policy conference at Stanford University on Friday.

For its part, the Fed has acknowledged the concern and has launched a review of its monetary policy framework and communication practices. In focus: how it publicly explains and achieves its dual mandate of maximum employment and stable prices (through its 2% inflation target).

New York Fed President John Williams said Friday that now is the time to rethink the Fed’s monetary policy strategy while the economy is in a “relatively benign place.”

“Markets are very sensitive to this issue,” Williams said.

Inflation: Not a big deal after all?

Inflation has been the main point of concern among Fed speakers. Since the financial crisis, the Fed has had difficulty stimulating consumption to its target, raising questions about how effective the Fed could be at spurring economic activity in the next downturn.

In 2012, the Fed adopted an inflation target of 2%, which policymakers felt was healthy enough for the economy without risking runaway prices. But since announcing its target, core personal consumption expenditures — the central bank’s preferred reading of inflation — have averaged only about 1.6%.

Fed officials are worried that persistently undershooting its target is undermining its credibility to stimulate consumption.

With rates closer to the zero bound than they were in the crisis, the Fed is wondering if it is time to adjust its approach to inflation to repair that credibility. The problem: Fed officials have different ideas for what would be the best fix.

For example, St. Louis Fed President James Bullard has advocated for nominal GDP targeting, which would prioritize the level of spending instead of the price level itself. In short, nominal GDP targeting suggests that the Fed could let inflation run above target if it meant supporting higher spending levels.

Williams, meanwhile, has pushed research showing that price-level targeting would be best in a low-rate environment. A close cousin to nominal GDP targeting, price-level targeting would similarly allow inflation to “make up” for falling short of inflation by running above 2%. But as the name suggests, the strategy prioritizes price levels (as measured through a price index) instead of nominal spending.

Cleveland Fed President Loretta Mester, however, said Friday that those alternative frameworks present “implementation challenges” and said the current strategy of inflation-targeting has “served the FOMC well.”

Her comments suggest that there is the possibility that the Fed makes no changes to its inflation targeting after the whole review is set and done.

Interestingly, Williams and Bullard have said there is nothing wrong with keeping the current regime.

Bullard told reporters on April 17 that there are communications challenges to a strategy like nominal GDP targeting, which could be more difficult for market participants to understand than straight inflation targeting.

“You’re basically getting 90% of what you can get by just having inflation targeting so there’s no sense in getting that other 10% and then risk miscommunication and risk misinforming or misinterpretation by financial markets,” Bullard told reporters April 17.

Williams said Friday that the current framework only misses inflation by a few tenths of a percent.

“That gives you an idea that even the miss on inflation isn’t that huge,” Williams said.

Need a ‘bazooka’

Outside of the Fed, some worry that the obsession over inflation may be missing the larger point.

Some argue the Fed needs new tools to pull itself out of the next crisis, one that would be more potent than an alternative inflation targeting scheme.

“The central bank needs a ‘bazooka’ at the zero bound that makes credible its commitment to achieving its policy rule, and raising inflation if required,” Harvard economics professor Kenneth Rogoff said.

Rogoff’s recommendation: negative interest rate policy. The thesis: allowing interest rates to go negative, in which customers would be charged to keep money parked at their bank, would be a quicker way of spurring consumption and recovering jobs in a downturn.

The push for negative interest rate policy is closely tied to skepticism that quantitative easing was an effective measure. Post-crisis, the Fed took on trillions of dollars in agency mortgage-backed securities and longer-term Treasurys, but with 10 years of hindsight some argue that the strategy may not have been all that impactful.

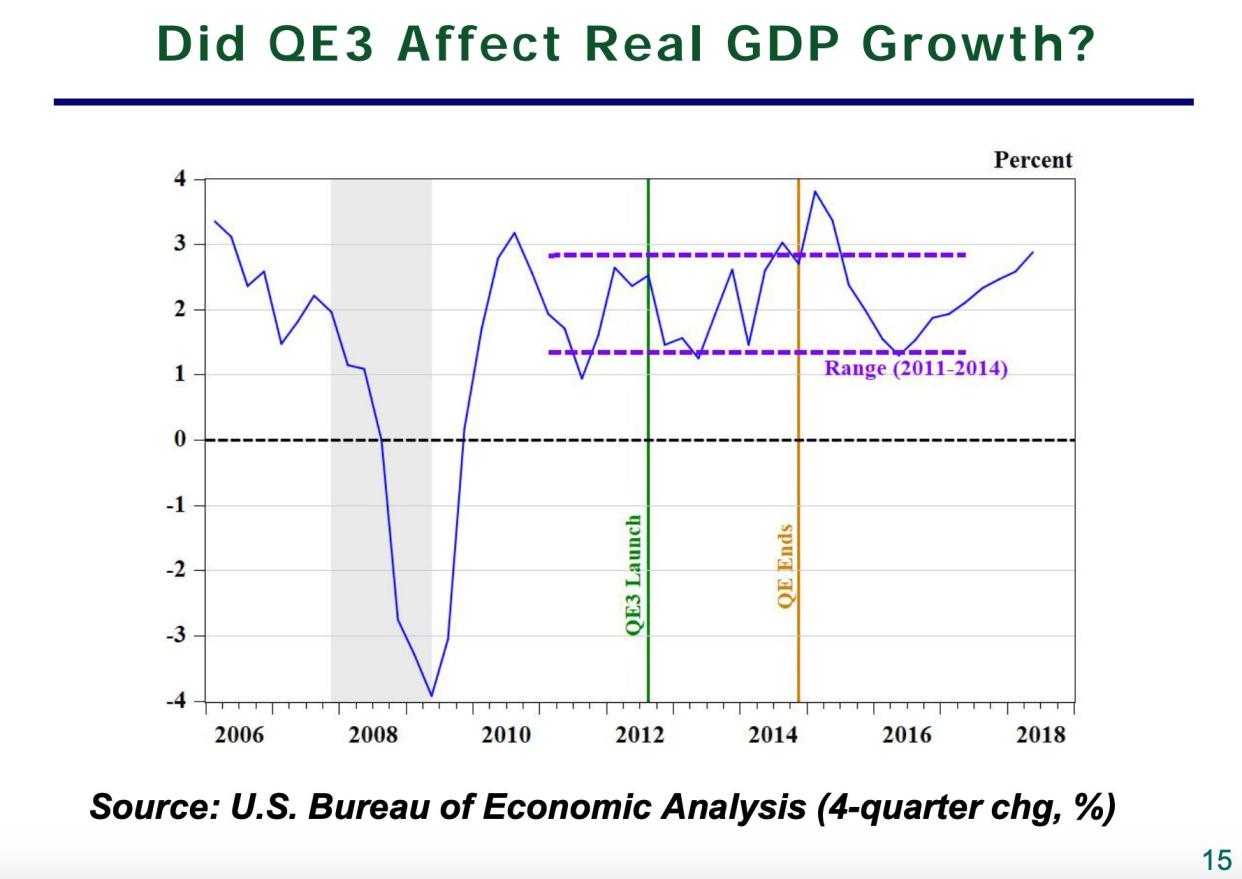

On Friday, Levin said the first round of quantitative easing was effective, but argued that when financial strains subside, further balance sheet actions have “little or no impact on the macroeconomy.” Levin argued that the Fed’s quantitative easing efforts between 2012 and 2014 — referred to as QE3 — had “negligible” effects on the growth of U.S. GDP and employment, further arguing that it had no effect on inflation.

Stanford economist John Taylor, whose work is focused on a rules-based monetary policy, told Yahoo Finance on Friday that quantitative easing is not nearly as potent as policymakers may have originally hoped for.

“It’s just an announcement effect,” Taylor said. “It just happens and then it disappears.”

Fed officials have not spoken extensively of the possibility of using negative interest rate policy, but Williams said in May that negative rates, in addition to more quantitative easing, would be on the table.

—

Brian Cheung is a reporter covering the banking industry and the intersection of finance and policy for Yahoo Finance. You can follow him on Twitter @bcheungz.

Powell on the economy: 'We don't see any evidence at all of overheating'

Bank CEOs quiet on M&A ambitions as expectations for consolidation build

Bank investors face a 'conundrum' in an inverting yield curve

St. Louis Fed President on December rate hike: 'It didn't come off very well'

Congress may have accidentally freed nearly all banks from the Volcker Rule