Here's the math to figure out how much it could cost to take over Papa John's

Papa John's is seeking buyers and putting itself up for auction, Reuters reports.

CNBC said Wednesday that Papa John's founder and former CEO, John Schnatter, was considering teaming up with a private-equity firm to buy back the company, but Schnatter denied the report.

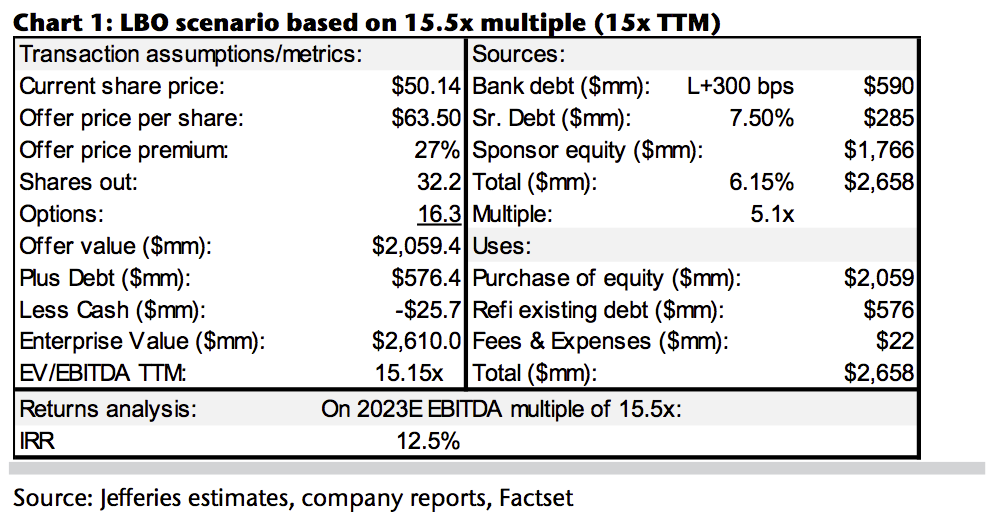

No matter who will be the buyer, Papa John’s is likely to be evaluated at $63.50 per share if it is acquired at similar valuation to Sonic, according to Jefferies.

Papa John's shares continue to climb after a report Wednesday said that the company is seeking buyers and putting itself up for auction. Shares spiked 8.5% following the news, and are up another 2.7% in early Thursday trade.

The pizza chain asked potential acquirers to submit offers and expects to receive its first round of bids by the end of October, according to Reuters, citing sources familiar with the matter.

Meanwhile, CNBC reported Wednesday that Papa John's founder and former CEO, John Schnatter, has been talking with private equity firms about buying back the company. Schnatter, through a spokesperson, denied CNBC's report.

"John Schnatter has not reached out to or had any discussions with any private equity firm or any other entity about buying Papa John’s," the representative said in an email. "Any such report about a potential transaction involving Mr. Schnatter is totally and completely false.

RELATED: Take a look at a few food chains that may take over the U.S.:

No matter who buys Papa John's, investors care mostly about what the pizza chain might be worth in the event of an acquisition. To figure that out, Jefferies analyst Alexander Slagle compared a potential deal with a recently announced deal in fast-food industry — Inspire Brands purchase of Sonic.

On Tuesday, Inspire Brands — the parent company of Arby's — said that it had reached a deal to acquire Sonic for $43.50 per share, or $1.57 billion. That total jumps to $2.3 billion, when including debt.

"If Papa John’s is acquired at similar valuation to Sonic, implies Papa John’s $63.50 potential acquisition price," Slagle said.

By Slagle's calculation, the $2.3 billion Sonic deal indicates that Sonic's enterprise value is 15.5 times the company's earnings before some items in the trailing twelve months. By applying the same 15.5 times multiple, Papa John's enterprise value totals $2.6 billion. After adjusting debt and cash, the pizza chain is likely to be valued at $63.50 per share.

Slagle said the comparison makes sense because Papa John's and Sonic have similar businesses and face similar struggles.

"We think the Sonic transaction is the most relevant, as it is a highly franchised quick service restaurants peer (95% franchised vs Papa John’s at 87%) that has been struggling until lately (8 consecutive quarters of negative same-store sales), although Sonic is fully domestic and has very modest unit growth," Slagle added.

Jefferies

More from Business Insider:

Short seller Andrew Left is creating a cannabis fund. He explains why the market's not in a bubble, but does need to 'chill out'

The boss of Santander's digital bank says it will be 'the same direction but faster' under new CEO Andrea Orcel

SurveyMonkey popped up 50% in its IPO — now its CFO explains the path ahead as it works toward profitability and faster growth

NOW WATCH: An aerospace company reintroduced its precision helicopter with two crossing motors