Sears CEO's master plan to profit off the demise of his stores is taking a turn for the worse

A bustling San Diego mall that's home to high-end stores like Nordstrom, Tiffany, and Restoration Hardware is defying the decline of shopping centers across the US and undergoing a massive $700 million expansion.

One store in the mall — Sears — won't survive long enough to reap the benefits of the redevelopment.

Desperate for cash, Sears Holdings sold the property in 2015, along with dozens of other prime locations, signing deals to rent the space from its new owner.

Now the company that bought those outlets is pulling the plug on San Diego store, which has been an anchor of the Westfield UTC shopping center for more than 40 years. Seritage Growth Properties, the real-estate investor, has already siphoned off a chunk of the store and leased it out to Williams-Sonoma and Pottery Barn Kids. This summer, it will take over the rest.

It's a lucrative move for Seritage. As Sears retreats from one of its most promising locations and fires dozens of employees, Seritage says it can triple the rent by turning the space over to the new high-end tenants.

This same scenario is playing out across the country, as Seritage picks up the pace of its takeovers of Sears stores. Seritage also reached new agreements in April to take over the entire Sears store at Aventura Mall in Miami, Florida — one of the most profitable malls in the country — and at malls in Dallas, Texas; Carson, California; and Charleston, South Carolina. It has already leased partial space in 123 Sears stores to other tenants, and it has completely taken over 24 stores.

'Widely anticipated demise'

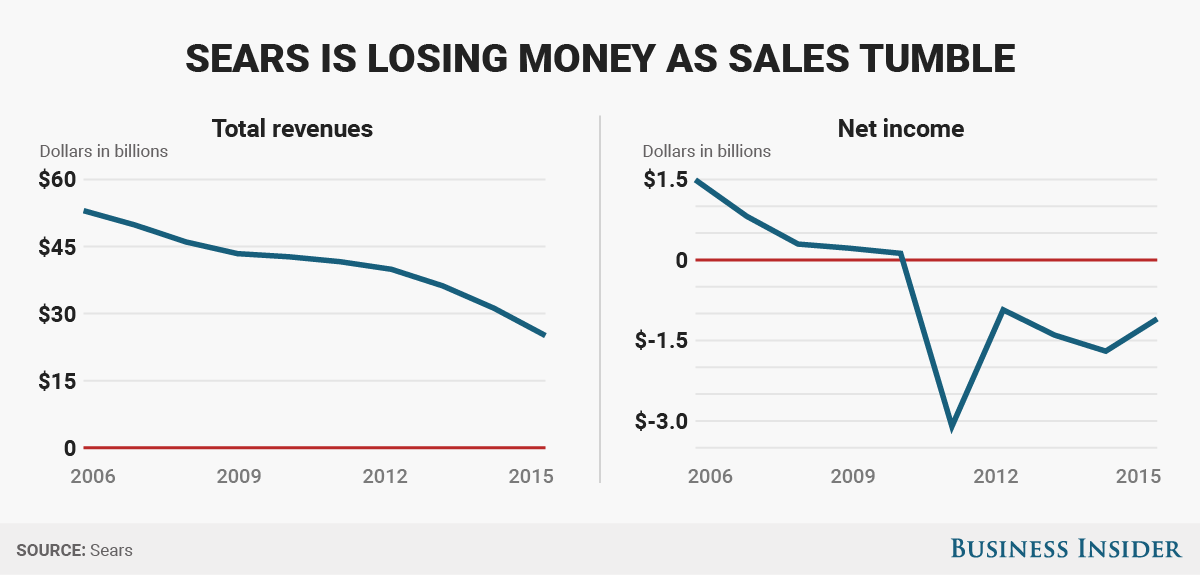

It is no secret that Sears is in crisis. Under the control of Chief Executive Eddie Lampert, the stores have suffered from years of underinvestment and sales have collapsed — falling by half since 2007. Lampert has at various points, either directed billions of dollars to share buybacks that only benefit investors — draining the business of vital resources — or focused on a loyalty membership strategy that has yet to prove its value even after several years.

Lampert and his hedge fund own 58% of Sears — the value of a stake that has dwindled as the share price has fallen over the years. Sears, once America's largest retailer, now has a market value of about $1 billion. Seritage is worth more, closer to $1.4 billion.

If Seritage can profit from Sears' retreat from brick-and-mortar retail, that's good for Lampert. In addition to being Sears CEO and largest shareholder, he is Seritage's chairman and his hedge fund owns about 40% of the real estate investor's limited partnership, as well as 8.5% of the voting power in its common stock. He has also recently extended credit to Seritage that it will use to redevelop the Sears stores. Seritage and Sears declined to comment for this story.

The fact that Lampert stood on both sides of the real estate sale as CEO of Sears and chairman of Seritage has already prompted a lawsuit. The suit said that the Sears stores were worth far more than $2.7 billion and that Lampert stood to benefit regardless thanks to his dual roles at the companies. Lampert, Sears' board of directors, and Seritage settled the lawsuit for $40 million this year.

But lately, analysts and investors have started to worry about Seritage too. Analysts say the speed at which Sears is unraveling could actually imperil Seritage, because it would lose a key tenant — which is responsible for about 60% of Seritage's rental income — much faster than it anticipated and may not have the resources to redevelop stores fast enough. Bets against the stock are also rising.

Seritage is "in a race to hasten redevelopment of former Sears-leased space in order to prepare for its lead tenant's widely anticipated demise," Floris van Dijkum, managing director at Boenning and Scattergood wrote in a recent note. "While management continues to deliver strong releasing spreads and attractive returns, we see a looming cash shortfall without a major capital raise."

Lampert's brainchild

After creating Seritage, Lampert orchestrated a massive real-estate deal in 2015, in which Sears sold 235 stores and interest in an additional 31 stores to Seritage Sears raised $2.7 billion from the sale and rented back the store space from Seritage.

The transaction, known as a sale-and-leaseback agreement, is relatively common, especially among traditional retailers looking to raise money from valuable real estate that they have owned for decades.

Sears needed the deal. The retailer was at the end of its rope with net losses ballooning to more than $8 billion in the five years leading up to the transaction so the $2.7 billion payment gave Sears a new lifeline.

Under its lease terms with Sears, Seritage has the right to recapture half or all of the space in the Sears and Kmart stores it owns, and then turn that space over to a new tenant. It has rented space to new tenants — like Whole Foods, Dick's Sporting Goods, and AMC— in more than 140 of these already.

Seritage can also get paid when Sears exits a lease early. If base rent outweighs earnings over a 12-month period, Sears can break the lease — but has to pay Seritage a full year of rent to do so.

Sears, which is closing more than 150 stores this year, exercised this right on 17 stores last September, filings show.

The bet that Seritage can profit from Sears real estate has drawn some deep-pocketed backers. Bruce Berkowitz's Fairholme Capital, a longtime Sears investor, owns 12% of the company's shares and billionaire investor Warren Buffett holds a 7% personal stake.

"A very important fact is that Seritage clearly proves the point about the value of the real estate remaining at Sears," Berkowitz told Fairholme investors on a conference call last November.

Over the edge

Skye Gould

The agreement with Seritage, while bailing out Sears, also pushed many stores into loss-making territory once they began paying rent and as sales failed to rebound, according to a former Sears executive who asked to remain anonymous for fear of legal retribution for speaking about the company.

"Sears is paying hundreds of thousands of dollars in rent per store, when before, Sears owned these properties," the executive said. "A lot of the stores are now unprofitable because of that."

On top of paying rent to Seritage, Sears reimburses the company for taxes and maintenance on the stores it owns.

These payments totaled $194 million in 2016 and $133 million in 2015. Meanwhile, Sears has been burning through cash at a rate of more than $1 billion per year and selling off real estate and other assets to stay afloat.

Stores have been laying off employees, cutting bonuses, and slashing work hours to stanch the losses.

"The team has been beaten down," the executive said. "They haven't gotten raises or bonuses in God knows when."

Seritage struggles

With this backdrop, what might've been seen as an opportunity for Seritage, is now being flagged as a risk. The company's shares have fallen more than 24% in the last year amid expectations of a possible bankruptcy filing by Sears.

Short interest in the stock — that is trades placed by investors who are betting it will decline further — have reached the highest level in its history, according to Matthew Unterman, Director at S3 Partners, a financial analytics firm.

"Even including all signed not open leases, [Seritage] would have a $12 million shortfall if Sears stopped paying rent," writes Dijkum, the Boenning and Scattergood director. "Thus, an imminent bankruptcy could leave the company owned by bondholders with equity holders potentially wiped out."

So Seritage has a huge incentive to recapture as many Sears stores as possible as quickly as possible — especially in high-traffic malls like Westfield UTC — and turn them over to new, higher-paying tenants. Sears pays Seritage about $4.45 per square foot in rent, whereas Seritage's non-Sears tenants are paying about $15.23 per square foot, according to Seritage.

SeritageIf Seritage can keep turning over Sears stores to new tenants — therefore reducing its reliance on Sears for rental income — before a possible Sears bankruptcy, then the company could turn out to be a good long-term bet.

But some investors are giving up on that idea, worried that Seritage's timeline to capitalize on Sears' assets is shrinking.

Mohnish Pabrai, managing partner of Pabrai Investment Funds purchased Seritage shares for his funds about a year ago and recently sold them all, according to Barron's.

"If Sears doesn't file until 2020, Seritage is fine," he told Barron's. "It is possible they are fine if there is a late-2019 filing. Any filing before that means taking extraordinary measures."

NOW WATCH: We tried Starbucks' new color-changing Unicorn Frappuccino that's taking over Instagram

See Also: