There's been a 'stunning' shift in the US economy since Trump's election

There is a chasm opening up in the US economy in the post-Trump landscape between enthusiasm and actual results.

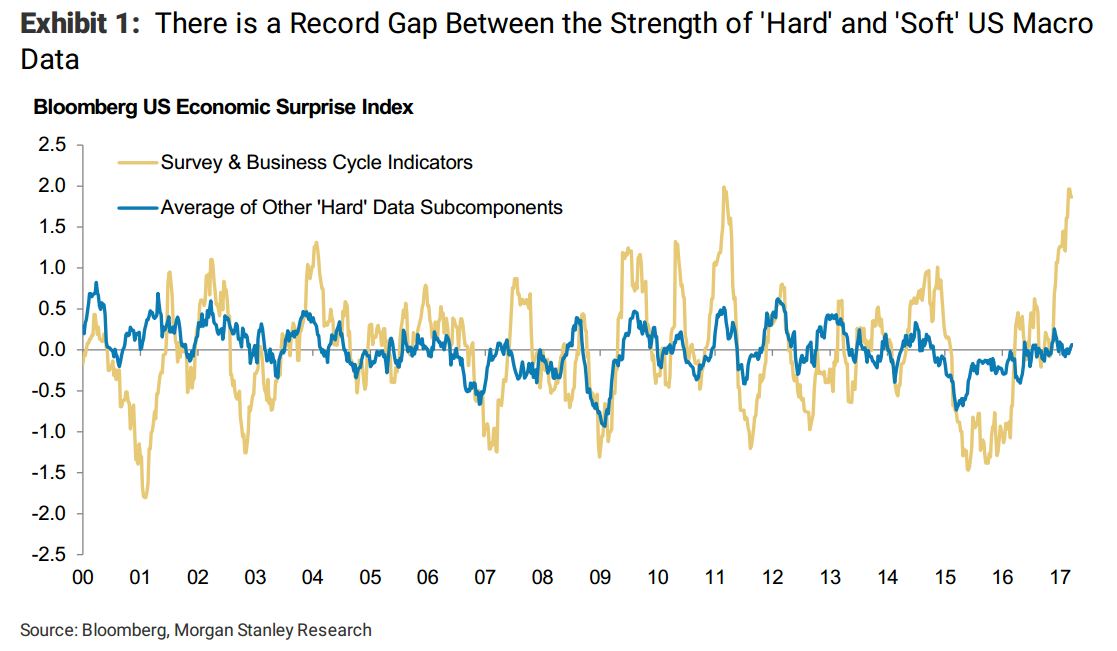

Morgan Stanley economists Ellen Zentner and Robert Rosener laid out the difference between sentiment following the election of Donald Trump — defined by "soft data" like surveys and confidence indexes — and actual activity — defined as "hard data" like industrial production and retail sales.

We've noted the divergence in soft and hard data before, but it appears the gap between the two types of data is only growing.

"The divergence is stunning," wrote Zentner and Rosener in a note to clients on Monday. "Upside surprises appear to be completely driven by the soft data while hard data are simply coming in about as expected."

The difference was once again reinforced on Tuesday, as the Conference Board's consumer confidence index surged to 125.6, its highest level since 2000.

Morgan Stanley

To underscore this point, Zetner and Rosener looked at a few different measures of expected GDP growth for the first quarter of 2017 — the New York Fed's GDP tracker and the Atlanta Fed's GDP Now. From the note:

"Compare the New York Federal Reserve Bank's current 1Q GDP tracking vs ours—FRBNY is currently tracking 1Q GDP at 3.0% versus us around 1%. The difference is larger than usual and is being driven by the fact that the New York Fed incorporates soft data into its tracking (attempting to tie it econometrically to GDP, a very hard thing to do especially in real-time). Our method translates the incoming hard data into its GDP equivalent. Note that the Atlanta Fed's GDPNow tracking also focuses on hard data and is currently tracking 1% for 1Q GDP."

Put another way, the GDP trackers that measure actual economic activity are much weaker than the NY Fed's which incorporates soft data.

Morgan Stanley

To be fair, this doesn't mean that the two types of data couldn't converge. Improved sentiment could in turn lead to more spending and thus greater economic activity. Conversely, the strong soft data could be a temporary bounce and eventually fall back to Earth.

In Zetner and Rosener's opinion, a mix of the two is most likely, with a small boost to the hard data but not enough to justify the massive leap in soft data.

"Moreover, we do expect that the breadth of the 2Q rebound in hard data will be fairly limited, with a swing in consumption as the main driver of the expected 2Q upside, followed by a slightly better net trade and inventory profile," said the note.

"As a consequence, we would not necessarily expect 'hard data' surprise indices to start racing higher if the factors behind the 2Q growth rebound remain narrowly confined to a few sectors as we expect."

NOW WATCH: 7 mega-billionaires who made a fortune last year

See Also:

SEE ALSO: Trump is making huge changes to his economic plans after the 'Trumpcare' defeat