How much will I get from Social Security if I make $75,000?

Social Security is an important part of your financial planning for retirement, and even if you're fortunate enough to earn more than the typical American, you'll still find that your Social Security benefits play a key role in helping you finance your golden years. If you earn $75,000 a year, you're well above the median income for entire American households, let alone individual workers.

But you still need to have an idea of what Social Security will give you. Below, we'll take a look at how much someone earning $75,000 per year can expect from Social Security.

Social Security payroll taxes: What to expect

If you earn $75,000 per year, then you'll have payroll taxes taken out of your pay throughout the year, because the wage base limit on Social Security is well into six figures. The current payroll tax on Social Security is 6.2% of your salary, so your employer will withhold $4,650 to go toward Social Security. Your employer will also pay $4,650 to cover the employer contribution toward Social Security payroll taxes.

The full $75,000 you earn will become part of your work history for purposes of determining your benefits. That's because you paid payroll taxes on your entire salary. As long as you weren't working for an employer that's exempt from Social Security -- most commonly state and local governments that choose to offer their own pensions instead -- then you'll earn the maximum of four credits every year to go toward your career goal of 40 credits to be entitled to Social Security in retirement.

Also see the average retirement age in every state:

Understanding the big picture

Keep in mind that simply earning $75,000 for a single year won't automatically determine what your Social Security benefit looks like. It takes a 35-year career to max out your Social Security benefits, with the Social Security Administration taking the average monthly earnings from your top-paid years after accounting for inflation.

Therefore, the question you have to answer is what path you followed to get to a $75,000 salary. If you got small but steady raises throughout your career, then your average earnings will be higher than someone who earned little until getting a big pay bump recently. Don't fall into the trap of thinking that Social Security works like some government or private pensions, where benefits are often based on just a few years at the end of your career.

What Social Security will pay you

We'll have to make some assumptions to provide an exact benefit number. Let's say that you'll turn 62 next year, have already worked for 35 years, and have gotten raises over the course of your career that are exactly equal to the rate of inflation. Those assumptions won't match up perfectly with your actual situation, but it can give you a starting point that you can then use to make adjustments to reflect your earnings history more precisely.

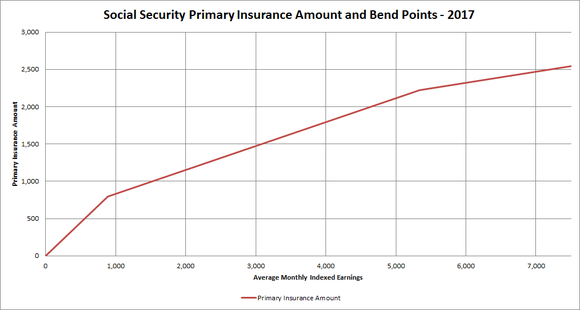

In this hypothetical scenario, your average indexed monthly earnings would be $6,250 per month. To calculate your benefits since you'll be age 62 in 2017, you'll need to use what Social Security calls bend points. Start with 90% of the first $885 in monthly earnings, and then add in 32% of earnings between $885 and $5,336, along with 15% of earnings above $5,336. Doing the math, 90% of $885 is $796.50, 32% of the next $4,451 is $1,424.32, and 15% of the remaining $914 is $137.10. Add all those up, and you get a total full retirement age benefit of $2,357.92, which is what you'd get if you wait until you are 66 years and two months old to claim.

Image by author. Data source: Social Security Administration.

In terms of income replacement, someone making $75,000 a year can expect Social Security to replace about 38% of your annual pay. If you want to maintain your pre-retirement standard of living, then you'll need to find other sources of cash.

Those who retire at ages other than full retirement age will see adjustments to their benefits. If you claim at the earliest age of 62, the haircut of nearly 26% will lead to benefits of about $1,749 per month. Wait until age 70, and you'll get almost 31% more, with monthly benefits of roughly $3,081.

Last, say you took breaks during your career and only managed to earn that $75,000 salary for half of a 35-year period. Most people assume that working half as much will produce a half-sized Social Security check, but the way the progressive benefits formula works, you'll get more. On average monthly earnings of $3,125, your benefit will be $1,513.30, or 64% of your full-career benefits. That's not bad, especially when you consider that you only paid half the payroll taxes that a full-time worker would have paid.

Make the most of Social Security

Social Security will make a big contribution toward retirement income even for those who make $75,000 a year. You'll want to have savings of your own to supplement Social Security, but the challenge of finding ways to save won't be quite as large as it would be without retirement benefits to help you.

The $15,834 Social Security bonus most retirees completely overlook

If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies..

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

RELATED: Check out the best states for retirement in 2016: