What are exemptions, deductions and credits?

It is easy to lump exemptions, deductions and credits into the same basket of tax-saving mechanisms, but they are distinctly different. Here are the simplified differences:

What They Reduce – Deductions and exemptions both reduce your taxable income, and credits reduce your overall tax bill. With reference to Form 1040, exemptions and deductions all take effect before line 43 (your taxable income), and credits are applied after line 44 (the tax you pay on that taxable income).

Exemptions and deductions reduce your taxes proportionally to your tax bracket, but credits reduce your taxes dollar-for-dollar regardless of your tax bracket. In other words, if you are in the 25% tax bracket, a $1,000 deduction saves you $250 on your taxes, but a $1,000 tax credit saves you $1,000 on your taxes.

Their Basis – Exemptions are only concerned with people and the relationship you have with them; aside from determining whether or not someone is a dependent, they have no financial basis. Deductions are related directly to expenses you incurred over the course of the tax year. Credits are generally incentives aimed at influencing behavior.

View important tax dates to know:

Let's look at the three categories in more detail:

1. Exemptions – A higher number of exemptions reduces your taxable income – essentially this says to the IRS, "these are the number of people I am responsible for." You, your spouse, and all your dependents receive exemptions.

Generally, dependents must be age 18 or younger (except for full-time students), a member of your family or a qualified relative, and must provide less than half of their own economic support. Unfortunately, your pets, while dependent on you, do not qualify as legal dependents in the eyes of the IRS. See IRS Publication 501 for details on who qualifies as a dependent.

You can reduce your taxable income by a set amount of money multiplied by the number of dependents. Exemption amounts are scaled back above certain income levels. For 2015 taxes, the threshold is $154,950 in Adjusted Gross Income (AGI) if married filing separately.

You cannot claim a personal exemption for yourself if someone else claims you as a dependent. Use the I.R.S. Interactive Tax Assistant to determine if you can claim someone as a dependent.

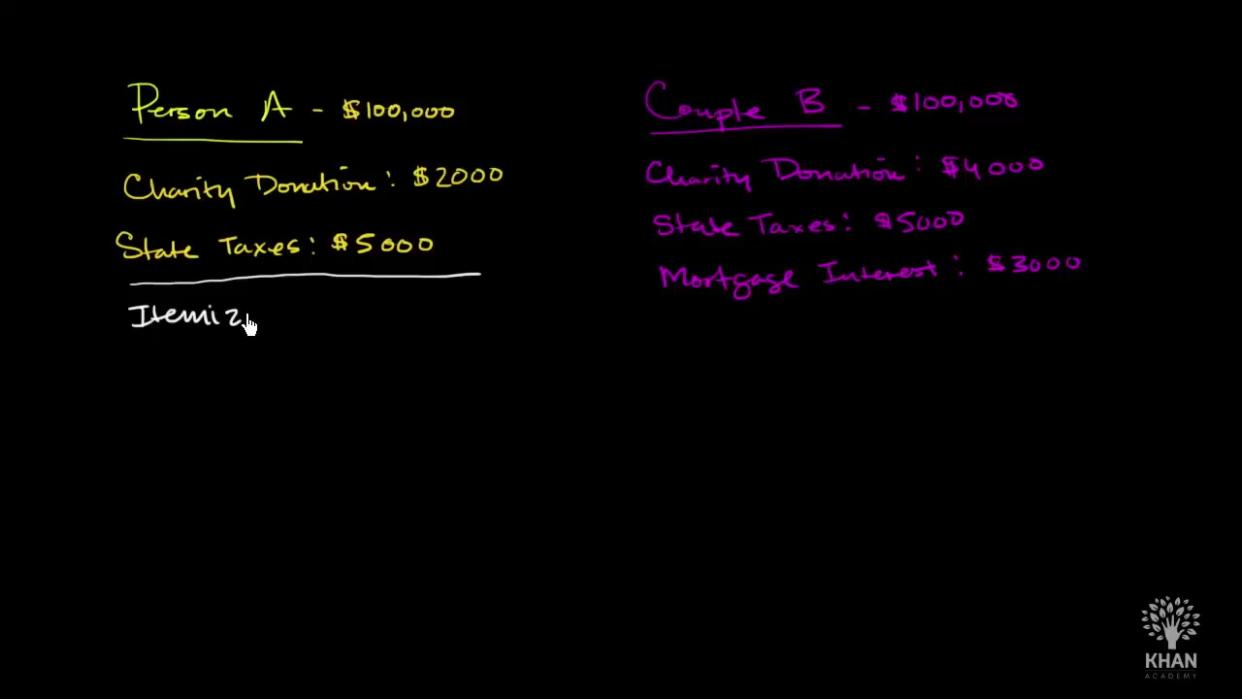

2. Deductions – Deductions are related to your expenses, but their impact varies based on two criteria – whether they are "above-the-line" or "below-the-line" expenses, and whether they are scaled relative to your income.

The other distinction in deductions is whether they are itemized – a list of individual deductions you can take – or a standard deduction that you can apply. The standard deduction is based on your filing status and has nothing to do with your actual expenses.

"Above-the-line" deductions mean they are used in figuring your AGI, before you have to decide whether to itemize or take a standard deduction. This means you can take these deductions whether you itemize or not. "Below-the line" deductions are itemized, and some can only be taken once the expenses exceed a certain percentage of your AGI. This makes above-the-line deductions doubly useful.

3. Credits – Credits are generally incentives aimed at one of two goals: to influence behavior, such as education credits and residential energy credits; or to address a societal concern, such as the child tax credit or adoption credits. Major credits have a separate line on Form 1040. Rooting out miscellaneous credits and the requisite IRS forms can be time-consuming but could prove to be time well-spent.

Some savings, like education costs, can be redeemed as either a credit or a deduction, depending on qualifications for each. Therefore, when trying to decide which is best, remember this hierarchy from generally most effective to least – credit, above-the-line deductions, exemptions, and below-the-line deductions. However, all of these are tax savings – so take all to which you are entitled, regardless of their size. If you need help in determining how to best utilize the exemptions, deductions and credits that may be available to you, seek out a qualified tax professional.

RELATED: 10 of the strangest ways states tax you

More from MoneyTips:

How To Maximize Your Tax Refund

Premium Tax Credit 101

Do You Qualify For An Earned Income Tax Credit?