2023 consumer debt levels grew, but not as severely as in 2022, according to Experian data

In 2023, good credit collided with higher interest rates, and everyone—consumers, policymakers and bankers—held their collective breaths. While some economists were watching for an economic downturn, consumers largely kept their eyes on their own finances as interest rates on loans and credit cards climbed significantly.

By year's end, it became clear the economic reality of 2023 was that of resiliency and not recession. As part of its ongoing review of consumer debt and credit in the United States, Experian examined representative and anonymized credit data from the third quarter (Q3) of 2023 to reveal some of the major trends in consumer credit. A few findings to consider as we begin:

Consumer spending continued at a healthy pace. Average credit card balances increased by 10% in 2023, and retail spending remained strong. Talk of an economic slowdown yielded to a "soft landing" narrative in the business press, a story that had the Federal Reserve getting praise for beating back inflation without unduly slowing economic activity.

Lenders became more discerning when deciding to extend additional credit. And for their part, some would-be homebuyers and home sellers decided to sit out the housing market entirely amid rising home prices and mortgage rates. Spending on some bigger-ticket items such as new cars also slowed as consumers balked at rising sticker prices and car loan rates that have plagued potential borrowers since 2022.

Consumers are still willing to pay more to borrow in 2023. They indicated they have their limits, however, if the mortgage and auto loan markets are anything to go by. In addition, delinquency rates, while increasing, are still lower than in previous years. Consumers largely still have the wherewithal to repay their existing obligations, much of which were borrowed with low fixed-rate terms.

In this analysis, note that while rising interest rates adversely impacted nearly all borrowers, not every consumer credit market was affected in the same way.

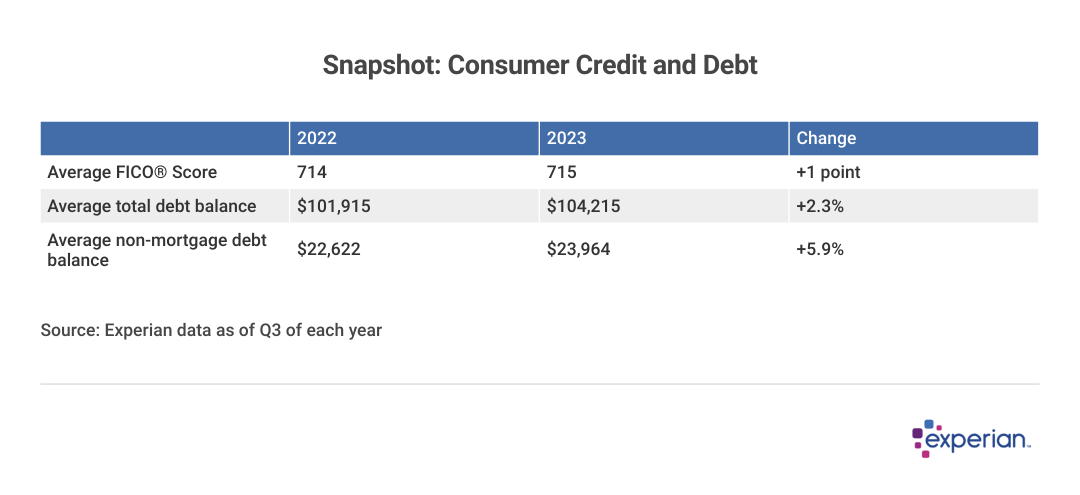

Average credit score in the U.S. increases to 715

As reflected in credit scores, creditworthiness remained broadly stable for most consumers in 2023. As of Q3, the average FICO Score in the U.S. was 715, a one-point increase from the same period in 2022.

Total debt rose, but increase is more apparent when mortgages are taken out of the equation

Meanwhile, average total debt balances increased by $2,300 to $104,215 in 2023. This 2.3% increase in total debt balance was modest relative to inflation, which grew by 3.7% over the same period.

Despite higher prices and rates, consumers seem both willing and able to service their existing debt, as well as assume additional debt without overextending themselves.

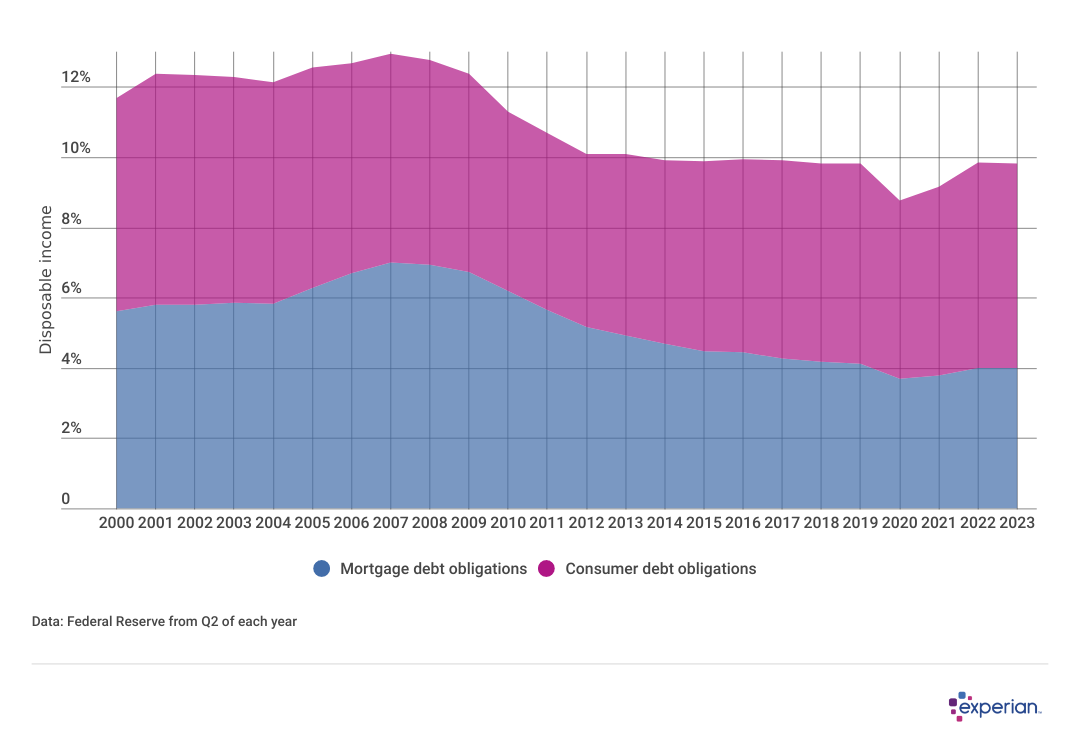

Debt service obligations remained steady

One measure of restraint shows that total debt service obligations—the percentage of disposable income that households devote to mortgage and consumer credit—are still significantly lower than they were in the mid-2000s, when rapidly falling house prices and job losses led to the Great Recession and a huge number of defaulted loans. Lenders, for their part, also showed restraint by tightening underwriting standards for mortgage loans over the same period.

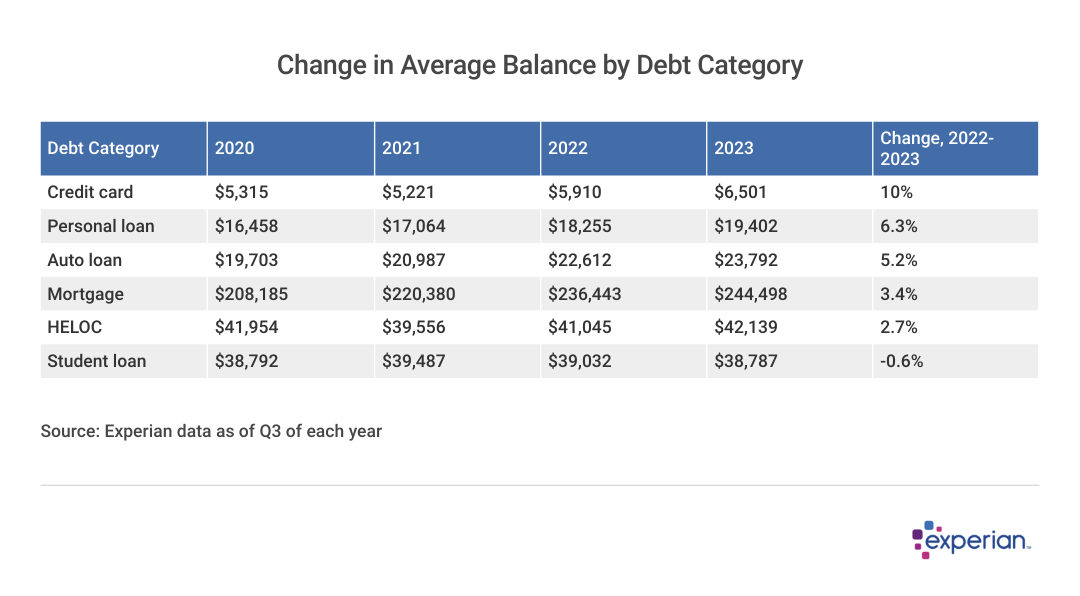

U.S. consumer debt snapshot

Average loan balances grew for most types of consumer debt in 2023. Credit cards—the debt products with the highest average interest rates for consumers—grew the most. The only category that bucked the trend was student loans, most of which benefited from an interest and repayment pause that ended in late 2023 after three years.

The loans that comprise the bulk of consumer balances—mortgages and student loans—typically have much lower APRs than those of credit cards. In the coming weeks, Experian will publish more detailed reports on each of these types of loans, but to quickly summarize each, here are the changes to average loan and credit card balances in 2023:

Credit card balances grew 10% to $6,501 in the 12 months from Q3 2022 to Q3 2023, as higher interest rates sharply increased in 2023. Consumers were by and large still able to service those balances, thanks to a tighter labor market leading to both higher employment and higher incomes.

Personal loan balances grew 6.3% to $19,402 in 2023 as more consumers made the decision to consolidate higher variable-rate debt into lower fixed-rate loans.

Auto loan balances grew 5.2% in 2023, to $23,792, as more consumers began to climb into more expensive vehicles, while paying more in interest for the privilege.

Mortgage balances climbed only modestly in 2023, up 3.4% in 2023 to $244,498. Despite average monthly payments for new mortgages skyrocketing, most mortgages currently being repaid are subject to much lower fixed rates than the 6% and higher mortgage rates prevailing for much of 2023.

Home equity line of credit (HELOC) balances increased modestly in 2023, to $42,139. For years, HELOC balances were in decline, as consumers (and lenders) preferred using cash-out refinances to extract equity from their homes. With mortgage rates significantly higher now, however, cash-out refinances will be a non-starter for most consumers. HELOCs remain an appealing alternative way for consumers to tap their home equity.

Student loans never went away, but many borrowers saw their payment requirements and interest accrual paused for more than three years. Meanwhile, various loan forgiveness programs have reduced overall student loan debt by more than $120 billion since the pandemic, and some diligent borrowers decided to repay their student loans throughout the payment pause.

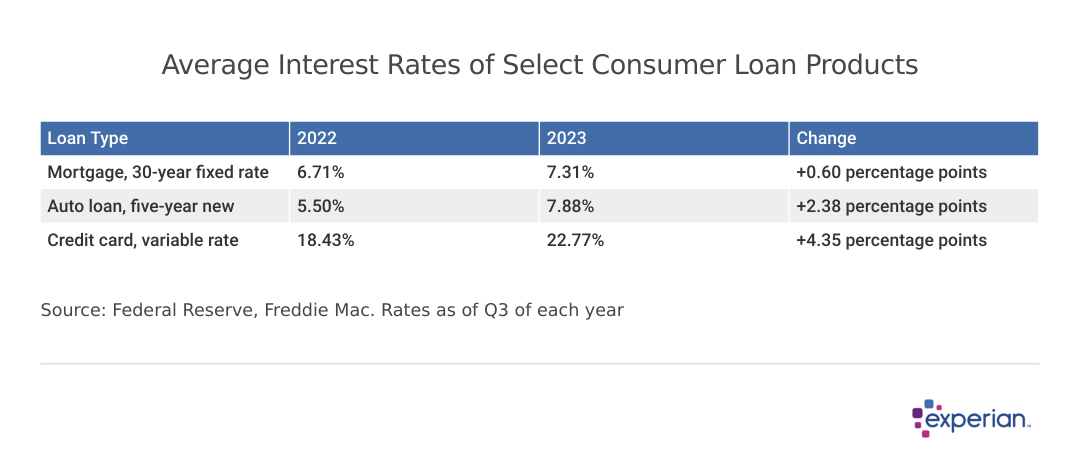

Loan interest rates jumped in 2023

The seeming relentless ratcheting up of interest rates impacted all consumers who needed to borrow. Not only did rising rates significantly increase borrowing costs, they soured many consumers on borrowing to purchase cars and homes. These purchases were rapidly increasing in price even before additional borrowing costs were taken into account.

To see how rising rates are impacting borrowers differently, consider two common types of consumer credit: mortgages and credit cards.

For fixed-rate mortgage borrowers, the rates they see today don't affect them directly. They'll continue to pay what is almost certainly a lower rate on their fixed mortgage, as long as they don't sell or refinance. And that's still most mortgage borrowers today: The majority of the $17 trillion in total outstanding consumer debt is owed on fixed-rate mortgages with APRs of 4% or less, compared with the current average mortgage rate of 7.31% available in late 2023. Most mortgages were made in 2021 or earlier.

But credit card users—at least those who carry balances from month to month—feel current interest rate hikes almost immediately. And that's with interest rates more than double those of mortgages.

The upshot? Consumers are walking away from one loan market (mortgages) while gravitating toward another with much higher interest rates (credit cards).

As rates climbed, some consumers exited the housing market as they were no longer able to afford a mortgage, while others still waiting on the sidelines further delayed the start of their home search. Consequently, the number of mortgages originated declined in 2023, resulting in the slowest mortgage market since 2008.

Many of these consumers are also now paying an average of 23% APR on revolving accounts, according to Federal Reserve data, with average balances around $6,500 as 2024 begins. That means borrowers carrying an average-size balance month to month would accrue around $112 in interest charges every month.

Despite mortgage rates being much lower than those of variable-rate credit cards, the markets for these loans behaved very differently from one another once rate increases began to take effect. Credit card usage for consumer goods remained strong, while mortgage usage for home purchases lessened. With higher interest rates affecting nearly everyone, the average credit card balance increased 10% in 2023 alongside a 4 percentage point increase in average annual percentage rates (APRs) over the same period.

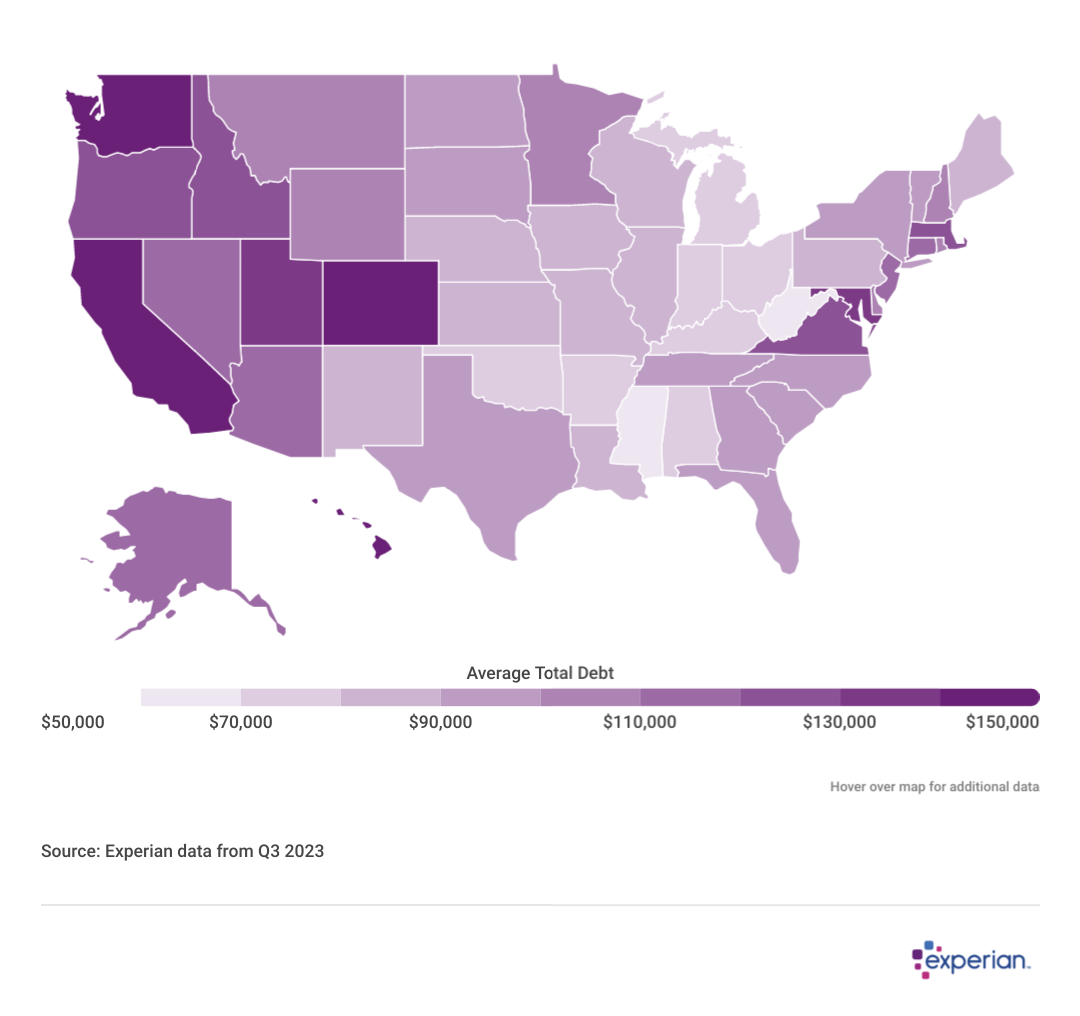

Average total debt levels up in most states

The 2.3% increase in average total debt in 2023 was more modest than was seen in 2022, when inflation was still roiling at 8% annual rates. Now that inflation has cooled, the increase in average total consumer debt has also slowed. Nonetheless, consumers are still enduring higher balances despite the slowing pace of inflation.

States with higher residential real estate prices, including California and Washington in the West and highly urbanized states in the Northeast, typically have larger total debt loads. Mortgages comprise at least 70% of all consumer-owed debt, and the cost of housing in these areas can have a significant impact on total debt levels.

Credit utilization and delinquency rates continue to increase (but slowly)

Average credit card debt increased significantly in 2023. At the same time, lenders became pickier about how much credit they're willing to extend, and which consumers they'll approve.

There are multiple factors that go into those approval decisions. Often, they're based on a consensus that considers where the health of the economy is currently, and where it may be headed over the next few months. A robust economy generally means fewer delinquent loans for lenders.

These lender decisions collectively influence the credit utilization rate of consumers, at least by way of determining credit limits. And while consumers overall still have a healthy appetite for credit card spending—balances increased by 10% over the past 12 months—card issuers seemingly aren't as willing to extend their credit line by an equal 10% in turn. As a consequence, average credit utilization increased from 28% to 30%.

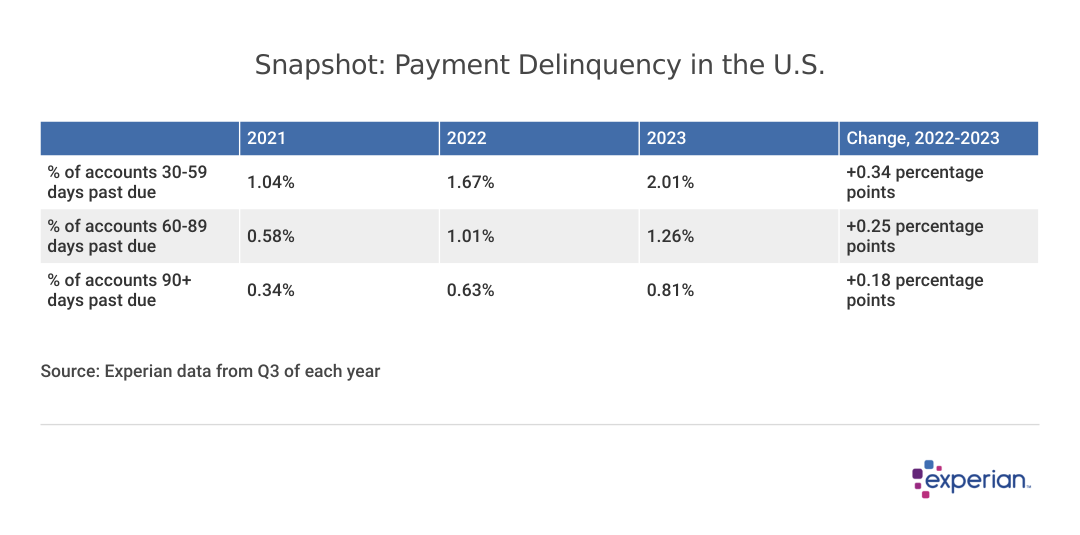

Delinquency rates increased in 2023 as well

Despite the increases, rates are still well below those observed prior to the pandemic. As of Q3 2023, 2.01% of accounts were 30 to 59 days past due; the number of accounts that were 60 to 89 days past due increased to 1.26%, and 0.81% of accounts were 90 days or more past due.

What borrowers can expect in 2024

Interest rates for consumer loans will decline

The Federal Reserve is expected to begin lowering interest rates sometime in 2024, but no one knows exactly when those decreases will begin. Much will depend on what the Fed sees in economic activity and price increases over the first months of 2024.

A sharp slowing of economic activity and low inflation may mean interest rate cuts will begin sooner rather than later in the year. But any federal funds rate decreases made by the Fed will take some time before reaching consumers in the form of meaningfully lower interest rates for mortgages and auto loans. As for credit card borrowers, a slight reduction in credit card interest rates, even if passed on within one or two months after the Fed lowers rates, will barely be noticed by some consumers when the average APR for credit cards is already above 20%.

Tighter budgets

Average monthly payments are growing, which will impinge future discretionary spending. The most obvious category where this is apparent is automobiles, where the average monthly payment on auto loans has grown from $588 in Q3 2022 to $630 in Q3 2023—a whopping 7.1% increase, according to Experian data.

Meanwhile, student loan borrowers began resuming their repayments in September, which adds an additional monthly payment averaging more than $200 for most borrowers.

Even fixed-rate mortgage borrowers face additional headwinds: Although their monthly payments haven't increased, for many, higher home insurance premiums can crimp those homeowners' budgets.

Continued wariness from lenders

Loan officers will continue to be particular about the credit histories of potential borrowers this year. They may limit the amount they're willing to lend and charge higher interest rates to consumers with lower FICO Scores.

The bottom line

Despite some headwinds, experts anticipate lower interest rates and tamed inflation in 2024. This could benefit borrowers, perhaps more than they may currently believe: As consumer confidence declined in 2023 largely due to unaffordable higher-rate loans, the reversal of at least some of those rate increases in 2024 may improve consumer sentiment in the months ahead.

Methodology: The analysis results provided are based on an Experian-created statistically relevant aggregate sampling of our consumer credit database that may include use of the FICO Score 8 version. Different sampling parameters may generate different findings compared with other similar analysis. Analyzed credit data did not contain personal identification information. Metro areas group counties and cities into specific geographic areas for population censuses and compilations of related statistical data.

This story was produced by Experian and reviewed and distributed by Stacker Media.