Buy, Sell, Hold: JA Solar

Source: JA Solar

As the sun sets on another earnings season, it's time to take a look back and reevaluate the solar industry and the major players. JA Solar has been on my watchlist for some time. With shares currently trading down more than 52% from its 52-week highs, is now the time to buy, or are shares still overvalued? Let's take a look.

Hanging up the cell

JA Solar has made a concerted effort of late to move away from supplying cells and concentrate more on supplying higher-margin PV modules. It has worked out well for the company so far. In 2012, JA Solar delivered 1,702 MW, of which modules comprised 55% and cells comprised 45%. In 2013, the company increased its module shipments, which rose to 57% of total megawatts shipped.

Because of the increased demand of its modules, JA Solar is planning to increase module capacity to 2.8 GW and to increase cell capacity to 2.8 GW. The approximate $130 million in capital expenditures is necessary, according to the company, as it is guiding for 2 GW in module shipments for 2014. If successful, this would improve upon the 1.2 GW of module shipments the company had in 2013.

Although the company's interested in transforming into a company which is primarily concerned with module shipments, JA Solar is still committed to delivering industry leading, high-quality cells. The company's multi-crystalline silicon cells average 18.3% efficiency, while the mono-crystalline cells have achieved over 20% efficiency. These cells are clearly in high demand. JA Solar ranked No.2 among the top 10 solar PV cell producers in 2013. Despite taking first place, Yingli Green Energy's mono-crystalline cells, at 17%, lag in efficiency -- multi-crystalline cells are also inferior, representing 15.6% efficiency.

Working toward profitability

The company's efforts at transformation have been fruitful. Gross margins improved throughout 2013, rising from 6% in the first quarter to 15.5% in the fourth quarter; likewise, operating margin showed improvement, rising from -5.1% in the first quarter to 2.7% in the fourth quarter. The increase in margins led to increased diluted earnings per ADS throughout the year, rising from a loss of $0.85 in the first quarter to earnings of $0.32 for the fourth quarter. Although unprofitable for 2013, JA Solar demonstrated a remarkable improvement over 2012 -- fiscal year 2013 yielded a net loss per diluted ADS of $1.94, while fiscal year 2012 yielded a net loss per diluted ADS of $7.05.

Profitability among Tier-One Chinese PV manufacturers is not common, and even though JA Solar was in the black for the fourth quarter, it still trails the profitability of two of its peers, Jinko Solar and Canadian Solar -- two companies that have proven to be profitable over the past twelve months. Among competitors who are also unprofitable for the trailing twelve months, the company offers a better value than Hanwha SolarOne , but JA Solar doesn't look as valuable as Trina Solar , which offers a better return on equity.

JASO Return on Equity (TTM) data by YCharts

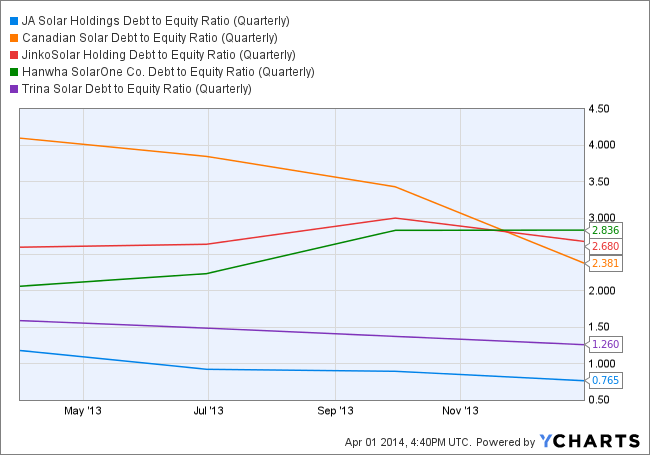

Handling debt

Always a concern when considering Chinese PV manufacturers is the management of debt. In this regard, JA Solar is a clear leader.

JASO Debt to Equity (TTM) data by YCharts

Considering JA Solar's plans to spend $130 million in capex in order to expand cell and module capacity, it will be important to see if the company manages to keep its expenditures under control so that it can maintain its impressive debt-to-equity ratio.

A Foolish conclusion...

For JA Solar in 2013, there are many positive takeaways, and I'll be interested to see if it can continue its recently impressive performance in 2014; however, in the meantime, I'll be keeping this one on hold.

Are you ready to profit from this $14.4 trillion revolution?

Let's face it, every investor wants to get in on revolutionary ideas before they hit it big. Like buying PC-maker Dell in the late 1980s, before the consumer computing boom. Or purchasing stock in e-commerce pioneer Amazon.com in the late 1990s, when it was nothing more than an upstart online bookstore. The problem is, most investors don't understand the key to investing in hyper-growth markets. The real trick is to find a small-cap "pure-play" and then watch as it grows in EXPLOSIVE lockstep with its industry. Our expert team of equity analysts has identified one stock that's poised to produce rocket-ship returns with the next $14.4 TRILLION industry. Click here to get the full story in this eye-opening report.

The article Buy, Sell, Hold: JA Solar originally appeared on Fool.com.

Scott Levine has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2014 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.