Is CarMax, Inc. Destined for Greatness?

Investors love stocks that consistently beat the Street without getting ahead of their fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with robust and improving financial metrics that support strong price growth. Does CarMax fit the bill? Let's take a look at what its recent results tell us about its potential for future gains.

What we're looking for

The graphs you're about to see tell CarMax's story, and we'll be grading the quality of that story in several ways:

Growth: Are profits, margins, and free cash flow all increasing?

Valuation: Is share price growing in line with earnings per share?

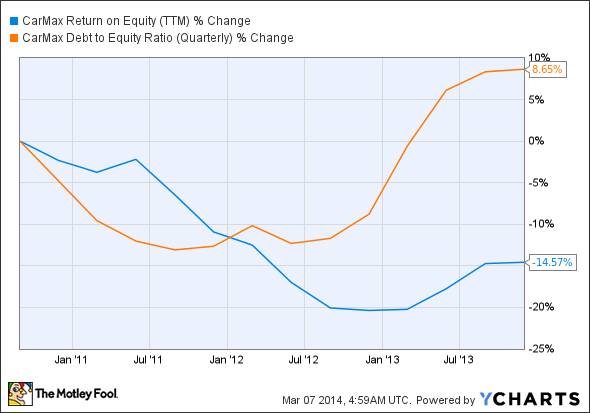

Opportunities: Is return on equity increasing while debt to equity declines?

Dividends: Are dividends consistently growing in a sustainable way?

What the numbers tell you

Now, let's take a look at CarMax's key statistics:

KMX Total Return Price data by YCharts.

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue growth > 30% | 51% | Pass |

Improving profit margin | (7.6%) | Fail |

Free cash flow growth >Net income growth | (1,610%) vs. 39.5% | Fail |

Improving EPS | 38.4% | Pass |

Stock growth (+ 15%) < EPS growth | 145.6% vs. 38.4% | Fail |

Source: YCharts. *Period begins at end of Q3 2010.

KMX Return on Equity (TTM) data by YCharts.

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Improving return on equity | (14.6%) | Fail |

Declining debt to equity | 8.7% | Fail |

Source: YCharts. *Period begins at end of Q3 2010.

How we got here and where we're going

Things don't look good at all for CarMax today, as the used-car superstore only mustered two out of seven possible passing grades. One big source of that weakness is its falling free cash flow, which has diverged markedly from its net income over the past three years and at latest tally was more than $1 billion in the red for the trailing 12 months. However, CarMax's stockholders have enjoyed solid growth during our three-year tracking period -- which could actually be worrying, as it's so far in advance of the company's fundamental earnings growth. Is CarMax's stock growing sustainably, or will this used-car retailer fall to its fundamental weaknesses in the end? Let's dig a little deeper to find out.

CarMax recently reported lower-than-expected third-quarter earnings results, largely due to fluctuating credit conditions in the auto industry. Fool contributor Andres Cardenal points out that third-party subprime lenders have recently tightened the credit terms for auto loans, as third-party subprime credit volume has been growing rapidly (perhaps too rapidly) over the past few years. CarMax has plans to become a direct subprime auto loan originator through its financing arm, which could help reverse its misfortunes.

While CarMax might seem differentiated from rivals AutoNation and Copart the three used-car companies have provided remarkably similar growth for investors over the past three years:

KMX Total Return Price data by YCharts.

This might seem surprising, as the growth in CarMax's earnings per share has actually been far weaker than that enjoyed by AutoNation or Copart investors. Over the past three years, AutoNation has put together three times the EPS growth enjoyed by its larger peer:

KMX EPS Diluted (TTM) data by YCharts.

Over the past few years, CarMax has delivered strong unit sales and same-store sales growth while continuing its geographical expansion in the domestic auto-loans market. Fool contributor Brendan Mathews notes that CarMax launched three new superstores in the third quarter of fiscal 2013, and it has plans to open another 14 stores in 2014, including new markets in Portland, Reno, Rochester, and Spokane. CarMax also boasts ambitious plans to open up between 10 and 15 new stores annually over the next few years. In a recent survey conducted by AutoTrader.com, 55% of new-car buyers are open to considering used cars if they are certified, which bodes well for CarMax due to its brand recognition, inventory variety, and geographical footprints.

Fool contributor Matthew Frankel notes that CarMax's earnings per share are expected to grow by 10% per year over the next few years. Since the company accounts for roughly 2% of the overall U.S. used-vehicle market, there are plenty of opportunities to further capitalize. CarMax's pilot program for subprime lending could become a major revenue driver, as subprime loans currently account for about 18% of CarMax's revenue.

Putting the pieces together

Today, CarMax has few of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy -- or to stay away from a stock that's going nowhere.

New cars are still popular -- in China! Find out how you can profit.

U.S. automakers boomed after WWII, but the coming boom in the Chinese auto market will put that surge to shame! As Chinese consumers grow richer, savvy investors can take advantage of this once-in-a-lifetime opportunity with the help from this Motley Fool report that identifies two automakers to buy for a surging Chinese market. It's completely free -- just click here to gain access.

The article Is CarMax, Inc. Destined for Greatness? originally appeared on Fool.com.

Alex Planes has no position in any stocks mentioned. The Motley Fool recommends and owns shares of CarMax. It recommends Copart. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2014 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.