Better Buy: Biogen Or Amgen?

Both Biogen and Amgen are succeeding thanks to fast growing therapies.

At Biogen, Tecfidera continues its blistering pace forward in winning U.S. multiple sclerosis market share from Novartis and Sanofi , which market oral competitors Gilenya and Aubagio, respectively. Meanwhile, Amgen's bone boosting drugs Prolia and Xgeva continue to win converts away from Novartis legacy drug Zometa. Sales of Prolia and Xgeva jumped 45% to $1.8 billion in 2013.

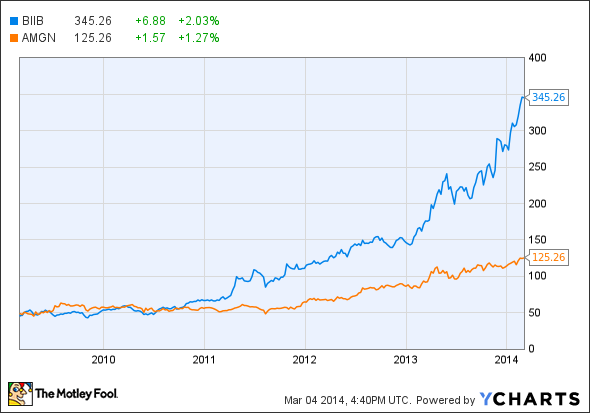

As a result, shares in both Biogen and Amgen are hitting new highs, but is one a better buy than the other?

Debating earnings

Biogen and Amgen have done a great job at under-promising and over-delivering this past year. Both companies have leveraged sales growth to outpace analyst earnings expectations in each of the past four quarters.

However, the rate of out performance by Biogen is shrinking as analysts adjust models to reflect the better-than-hoped launch of Tecfidera. After winning the FDA's go-ahead in March, Tecfidera has already racked up over $875 million in sales, helping Biogen's revenue jump 26% last year to nearly $7 billion.

Quarterly EPS Versus Analysts Estimates | ||||

|---|---|---|---|---|

Surprise % | March 2013 | June 2013 | September 2013 | December 2013 |

BIIB | 22.40% | 19.20% | 11.90% | 2.60% |

AMGN | 6.50% | 8.60% | 9.60% | 8.30% |

Source: Yahoo!Finance

Optimism that Biogen's Tecfidera roll-out will remain a success this year has analysts increasing their outlook for earnings. Projections for 2015 earnings have increased from $13.72 to $13.96 per share over the past 90 days.

Meanwhile, analysts are less convinced that Amgen will be able to offset greater competition for Amgen's blockbuster Enbrel with Prolia and Xgeva. As a result, estimates have dropped from $8.80 90 days ago to $8.70 for 2015.

2015 Analyst Earnings Projections | ||

|---|---|---|

Current | 90 Days Ago | |

BIIB | $13.96 | $13.72 |

AMGN | $8.70 | $8.80 |

Source: Yahoo!Finance

While the higher earnings expectations for Biogen reflect the growing opportunity for Tecfidera to protect Biogen's multiple sclerosis franchise (also including Avonex and Tysabri), the drop-off in expectations for Amgen may not adequately reflect the opportunity to leverage drugs obtained in last summer's acquisition of Onyx.

One of those acquired drugs is multiple myeloma treatment Kyprolis. Sales of Kyprolis grew from $65 million in the third quarter to $73 million in the fourth quarter. That $280 million a year run rate is even more intriguing when we consider Amgen hasn't filed for Kyprolis' approval in Europe yet, and that ongoing trials for Kyprolis as a first and second line treatment could offer significant sales and earnings growth over time, especially given Kyprolis' $40,000 price tag.

Debating valuation

Most Investors wouldn't consider either of these biotech companies as value picks. Each has a price to sales ratio that is well above where buy-low investors would feel comfortable, but Amgen's 5 times sales is better than Biogen's 11.5 times.

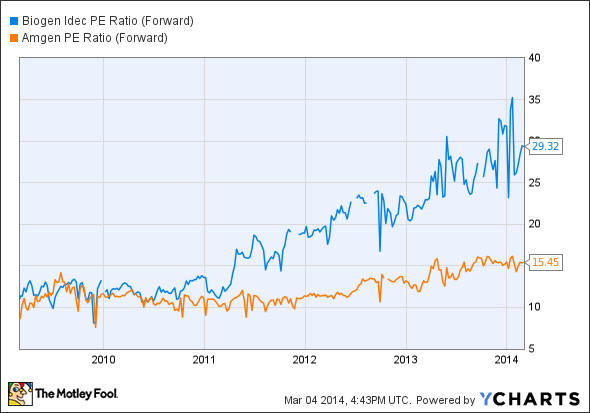

Amgen is also less pricey when considering how much investors are paying for earnings. Using trailing 12 month figures, Amgen's P/E ratio is 18.8 versus Biogen's 44.2. Looking ahead, Amgen investors are paying 15.4 times forward earnings per share, while Biogen's are paying 29 times earnings.

BIIB P/E Ratio (Forward) data by YCharts

Amgen also bests Biogen in terms of how much investors are paying for earnings and future growth. The company's forward PEG ratio is just 1.01, versus Biogen's 1.47.

Fool-worthy final thoughts

It appears Amgen remains the better buy based on valuation, but questions remain whether drugs like Prolia, Xgeva, and Kyprolis can offset patent risk. That suggests Foolss should watch analysts expectations carefully as the year progresses to see whether expectations find their footing and start heading higher.

In Biogen's case, it's hard to make an argument for value investors to want to own shares. However, an argument could be made for growth investors, especially if Tecfidera can keep winning business from Novartis' and Sanofi's competing therapies. If so, that strengthens an already rock-solid earnings outlook. That suggests Amgen may be the better buy for value investors, and Biogen may be the better option for growth pickers.

Here's 1 more important stock to watch this year

There's a huge difference between a good stock and a stock that can make you rich. The Motley Fool's chief investment officer has selected his No. 1 stock for 2014, and it's one of those stocks that could make you rich. You can find out which stock it is in the special free report "The Motley Fool's Top Stock for 2014." Just click here to access the report and find out the name of this under-the-radar company.

The article Better Buy: Biogen Or Amgen? originally appeared on Fool.com.

Todd Campbell has no position in any stocks mentioned. Todd owns E.B. Capital Markets, LLC. E.B. Capital's clients may or may not have positions in the companies mentioned. Todd owns Gundalow Advisors, LLC. Gundalow's clients do not own shares in the companies mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2014 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.