Is AT&T Worth its Weight In Dividends?

It's common knowledge that AT&T offers the richest dividend yield on the Dow Jones Industrial Average nowadays. At 5.7%, AT&T's yield is 1.1% ahead of second-richest income yielder Verizon , and light years in front of the Dow's 2.7% average yield.

But that's doesn't automatically make AT&T a great dividend stock. One hallmark of an awesome dividend payer is a willingness -- nay, a solid commitment -- to increase those golden payouts on a regular basis. And that's where AT&T doesn't measure up.

Let's apply the time-honored Gordon Growth Model of dividend-based valuation to AT&T. The model makes a few important assumptions: the underlying business has matured and should grow both earnings and dividends at a steady state for the foreseeable future, and the company pays as much as it can in dividends.

Image source: AT&T.

Does AT&T qualify under these criteria? I'd say so.

Analysts see AT&T growing earnings by 6.3% this year and by 6.1% over the next five years. These estimates are below estimates for the S&P 500 market barometer, and roughly in line with the 6.9% annual growth of the Dow over the turbulent last decade. So the expected growth looks stable enough to move ahead.

As for dividend payout ratios, AT&T has funneled 101% of its adjusted earnings into dividend payments over the last five years. Real traditionalists might prefer to look at dividend payouts versus so-called free cash flow to equity, or FCFE, which is a cash-based metric that accounts for net debt changes.

By that metric, AT&T fares a bit better. The five-year dividends-to-FCFE ratio stands at 74% today. Even so, there isn't much headroom for dividend growth here.

And that shows in AT&T's slug-like dividend boosts. Sure, Ma Bell increases her dividends every year -- but the increases have landed at or below 2.5% in each of the last five years.

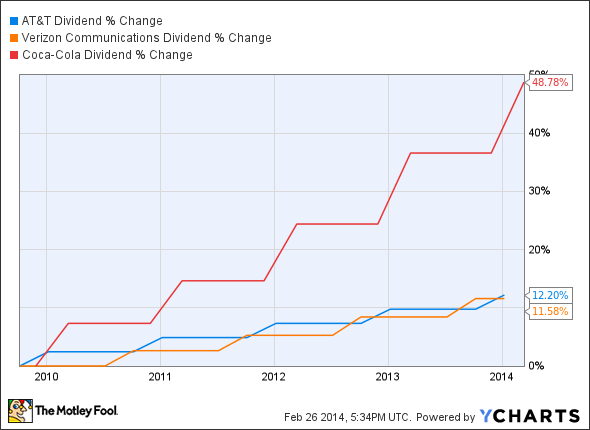

Verizon isn't doing much better, and both telecoms rank among the slowest dividend growers on the Dow. To put this disadvantage into perspective, let me compare their dividend trends with a stock that is growing payouts more in line with Dow averages:

T Dividend data by YCharts.

It's time to plug AT&T's profile into a Gordon Model spreadsheet, like the ones provided by New York University professor and occasional Fool writer Aswath Damodaran. I'm using the stable growth dividend discount model, because the exercises above make me satisfied that it suits AT&T.

This is the result:

If AT&T keeps dividends growing at the current 2.4% rate, the stock would be worth about $30 per share. The stock currently trades for $32 per share, so buying it for dividend value today would mean overpaying by 7%.

If AT&T decides to step up its dividend increases, the Gordon Model value skyrockets quickly. But I don't see much evidence that this value-creating future is in the cards.

Consider this: dividends per share may have increased 12.4% over the last five years, but that includes a massive share buyback program that reduced the number of shares by 9.4% in the last two years. AT&T's dividend expenses have actually only grown 0.4% since 2008. The company is bending over backward to keep dividend costs low without totally destroying its payout yield.

In the end, there's a fair chance that my $30 Gordon Model price actually overvalues AT&T shares, since the company's payout policies are only growing weaker.

AT&T can always surprise me with a brand new direction, but the low headroom means Ma Bell needs a fundamental business improvement first. Too many ifs and buts for me, and I'm sticking to my $30 fair value for AT&T shares from an income investor's perspective.

Want to learn more about dividend investing? Start here!

One of the dirty secrets that few finance professionals will openly admit is the fact that dividend stocks as a group handily outperform their non-dividend paying brethren. The reasons for this are too numerous to list here, but you can rest assured that it's true. However, knowing this is only half the battle. The other half is identifying which dividend stocks in particular are the best. With this in mind, our top analysts put together a free list of nine high-yielding stocks that should be in every income investor's portfolio. To learn the identity of these stocks instantly and for free, all you have to do is click here now.

The article Is AT&T Worth its Weight In Dividends? originally appeared on Fool.com.

Anders Bylund has no position in any stocks mentioned. The Motley Fool recommends Coca-Cola. The Motley Fool owns shares of Coca-Cola. Try any of our Foolish newsletter services free for 30 days.We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2014 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.