Dividend Derby: Bristol-Myers Squibb Vs. AstraZeneca

Dividend darlings Bristol-Myers and AstraZeneca are core holdings for income investors looking to offset anemic bond yields. However, rising market volatility and stubbornly low fixed income yields have pushed dividend yields at both companies to nearly five year lows.

In the wake of Bristol-Myers selling its half of the two companies' diabetes joint venture to AstraZeneca in December, now is the perfect time to see if one may be a better buy than the other.

BMY Dividend Yield (TTM) data by YCharts

Dividend busting headwinds?

The ability to grow revenue and profit is vital to growing dividend payouts. That means that drug makers are at a disadvantage to other dividend-paying companies because they're continuously battling patent expiration on their best-selling products.

In 2012, Bristol lost exclusivity on its top selling cardiovascular drug Plavix. This cratered its operating margin and net income, forcing a major restructuring that ultimately resulted in Bristol's unloading its half of the diabetes joint venture to Astra. Sales of Plavix totaled just $258 million last year, down from $2.5 billion in 2012.

At Astra, the loss of exclusivity on its blockbuster drug Nexium this coming May and Crestor in 2016 pose a significant threat to the company's profitability as well. Nexium generated $991 million in sales last quarter, while Crestor produced $1.5 billion in fourth quarter revenue (both numbers assume constant exchange rates). Those key future patent losses make the 6% decline in Astra's global sales last year even more worrisome. Unfortunately, the resulting drop in earnings will limit the ability of both companies to return more money to shareholders.

Turning the freighter

To overcome patent headwinds, Bristol and Astra will need sales for current products to quicken.

At Bristol, a lot of heavy lifting is being done by cancer drug Yervoy. Yervoy's sales grew 23% year-over-year to $260 million in the fourth quarter, bringing full-year sales to $960 million, up 36% from 2012. Bristol's 2013 sales of Sprycel and Orencia are helping too. Sprycel sales of $1.3 billion were up 26% and Orencia's sales of $1.4 billion were up 23% in 2013.

Over at Astra, the blockbuster Symbicort is negating some risk. Symbicort generated $3.5 billion in revenue in 2013, up 10% from 2012. Brilinta is also helping Astra given sales grew 216% to $283 million last year. Astra is also relying on growth in the newly unified diabetes lineup, which includes Byetta, Bydureon, Onglyza, and the newly approved Farxiga.

Advancing new products to market

If both companies hope to exceed pre-expiration peak annual sales, those existing products will need help from new drugs in their pipelines.

Fortunately, there are a couple of key compounds at Bristol that could start contributing to sales in the next year or two. One of them is daclatasvir, a hepatitis C drug that the company has already filed for approval in both Japan and the EU -- regions with a significant unmet need.

While daclatasvir probably won't be as successful as Gilead's Sovaldi, it has a good shot at becoming the number two player in the space, particularly given combining it with Sovaldi cleared the disease in a very high percentage (>90%) of patients during a Phase 2 trial.

Bristol also has nivolumab, a PD-1 targeting cancer compound being studied in melanoma, lung cancer, and kidney cancer. The potential has analysts pegging annual peak sales of as much as $4 billion. Bristol is also working with AbbVie on elotuzumab for multiple myeloma. Last summer, the two companies presented intriguing data from a mid stage trial showing the drug improved progression free survival.

Meanwhile, Astra has a robust drug pipeline, with more than ten drugs in phase 3 trials and 27 in phase 2. One of the most intriguing drugs in development is olaparib, a gastric and ovarian cancer compound that was repurposed following a failed mid-stage trial. Another interesting compound is brodalumab, which is being co-developed with Amgen . The two companies think that the drug could have potential as an alternative to Amgen's blockbuster drug Enbrel in psoriasis. If all goes well, Astra thinks it could file for FDA approval in 2015.

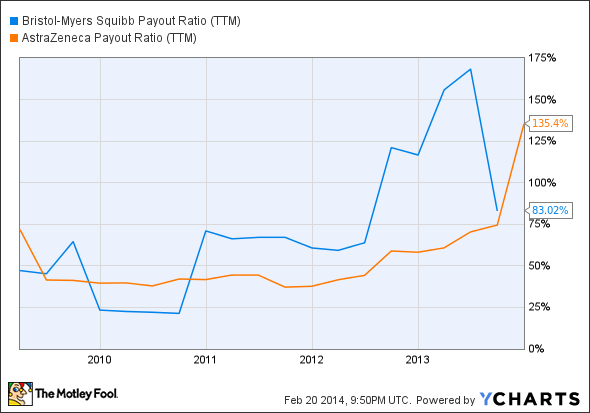

For dividend investors, the filings and potential approvals won't come quickly enough. Dividends are eating up a big share of earnings at both companies. With payout levels near or above 100% of earnings in the past year, dividend investors should stay vigilant.

BMY Payout Ratio (TTM) data by YCharts

Fool-worthy final thoughts

Both Bristol and Astra are paying out a big chunk of their earnings as dividends, which means product growth and new products will be necessary for future dividend increases.

Of the two, Bristol may be better positioned to up its payout quicker thanks to improving profitability. Bristol's 2013 operating margin improved to 18% from 13% in 2012, while Astra's declined to under 15%. So, while Astra's dividend yield is higher than Bristol's, it may also come with greater risk. That suggests dividend investors should keep a close eye on the two company's pipelines and financial ratios this year to see if conditions improve or worsen.

These 9 companies dividends are on less-shaky ground

One of the dirty secrets that few finance professionals will openly admit is the fact that dividend stocks as a group handily outperform their non-dividend paying brethren. The reasons for this are too numerous to list here, but you can rest assured that it's true. However, knowing this is only half the battle. The other half is identifying which dividend stocks in particular are the best. With this in mind, our top analysts put together a free list of nine high-yielding stocks that should be in every income investor's portfolio. To learn the identity of these stocks instantly and for free, all you have to do is click here now.

The article Dividend Derby: Bristol-Myers Squibb Vs. AstraZeneca originally appeared on Fool.com.

Todd Campbell has no position in any stocks mentioned. Todd owns E.B. Capital Markets, LLC. E.B. Capital's clients may or may not have positions in the companies mentioned. Todd also owns Gundalow Advisor's, LLC. Gundalow's clients do not have positions in the companies mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2014 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.