You Should Sell Vera Bradley and Coach, and Buy Kors Instead

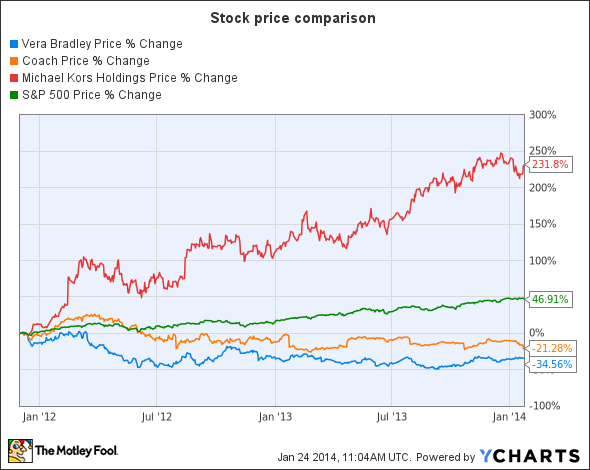

The fashion-apparel and accessories retail market has been notoriously treacherous because of macroeconomic headwinds, as a result of which consumers are spending less on the nice-to-have items. Hence, despite luxury handbags being the second-most-desirable accessories after shoes, Vera Bradley , known for its colorful luxury handbags, has been underperforming the market, much like Coach . However, rival Michael Kors Holdings is on a solid run, as seen below.

Vera Bradley data by YCharts

But the question is, will Vera turn around? Can it be a good buy for investors going forward compared to Coach and Kors? Let's find out.

A closer look at Vera Bradley

Vera posted estimate-beating third-quarter fiscal 2014 results, beating on both top and bottom lines. Net revenue decreased 6% to $130.1 million from $138.3 million in the prior year. The top-line decline was due to weak mall traffic, which resulted in comparable-store sales declining by 6.5%. As revenue took a hit and inventory levels increased, earnings were also affected. Net income decreased 14% to $15.2 million, or $0.37 per diluted share, compared to net income of $17.7 million, or $0.44 per diluted share, in the prior year.

Vera seems to be in the midst of an identity crisis as it is trying to focus more toward a multichannel sales platform, and it has not been able to achieve success on all sales channels at the same time. For example, in the direct segment comprised of company-owned retail and outlet stores, sales increased 7% to $68.9 million. The direct segment accounted for 53% of total net revenue in the third quarter versus 46% in the prior year. However, e-commerce sales declined 8%, and indirect net revenue declined 17%. If only Vera could achieve growth on all three fronts, a turnaround would be in sight.

Vera appointed Robert Wallstrom as its chief executive officer with the objective of turning around the fortunes of the company. Wallstrom has more than three decades of experience in the retail industry, and under him, Vera will focus more on retail expansion to push the performance of the direct segment. In the indirect segment, it is focusing on key accounts like Dillard's and Disney instead of trying too many things at once.

In addition, Vera has already revamped its website to a responsive design so that consumers can access the site and place orders from any device. This change alone resulted in a traffic surge from mobile devices, and user activity buying Vera products from their smart devices was up 10% from last year and took up close to half of the quarter's overall traffic.

However, turning around a business is a long process, and Vera is aware of this. The new launches were unable to generate much enthusiasm. As a result, Vera revised its fourth-quarter guidance and expects net revenue to be in the range of $145 million to $150 million compared to $163 million in the prior-year quarter. Diluted EPS is expected to be in the range of $0.44 to $0.47. This is keeping in mind that there will be higher promotional activity in a challenging retail environment.

Coach and Kors: looking for the better pick

Coach performed better than Vera, as its sales declined just 1% to $1.1 billion and operating income declined 3% to $322 million. Earnings per share, however, remained flat at $0.77, helped by share buybacks during the past 12 months. This decline in performance, from double-digit growth last year, was due to a challenging retail environment resulting in a 6.8% decline in comps, the first such decline since the company's September 2009 quarter.

According to analysts, the reason behind this significant drop is pretty clear. Target customers are switching over to competitors -- Michael Kors being one of them.

Michael Kors has been gaining at the expense of others in the global luxury market. During the second quarter of fiscal 2014, Kors was able to sustain its strong momentum across all segments and geographies. Its revenue rose 38.9% to $740.3 million while comps jumped 22.9%, making it the 30th consecutive quarter of growth for the company.

However, Coach has a strong international footprint, especially in China, where it registered double-digit sales growth of 35% due to distribution and double-digit comps growth. Coach's international sales jumped 9% year over year. In fiscal 2014, Coach expects to grow its square footage by about 25% to 30 net dual-gender stores. It is expecting total sales of around $530 million in China.

Bottom line

Vera Bradley is struggling to turn around its business, and Coach is losing customers to Kors. Hence, it will be best for investors to stay away from both Vera Bradley and Coach for the time being. Both are seeing revenue declines, and this is not good news. On the other hand, Kors is aggressively looking to grow its store area and is in a good position in the Chinese market, making it a stock worth owning.

Start investing right this very second

Millions of Americans have waited on the sidelines since the market meltdown in 2008 and 2009, too scared to invest and put their money at further risk. Yet those who've stayed out of the market have missed out on huge gains and put their financial futures in jeopardy. In our brand-new special report, "Your Essential Guide to Start Investing Today," The Motley Fool's personal finance experts show you why investing is so important and what you need to do to get started. Click here to get your copy today -- it's absolutely free.

The article You Should Sell Vera Bradley and Coach, and Buy Kors Instead originally appeared on Fool.com.

Meetu Anand has no position in any stocks mentioned. The Motley Fool recommends Coach and Michael Kors Holdings. The Motley Fool owns shares of Coach. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2014 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.