Why Size Will Matter for These Stocks in 2014

Let's face it, when it comes to real estate investment trusts (REITs), size does matter.

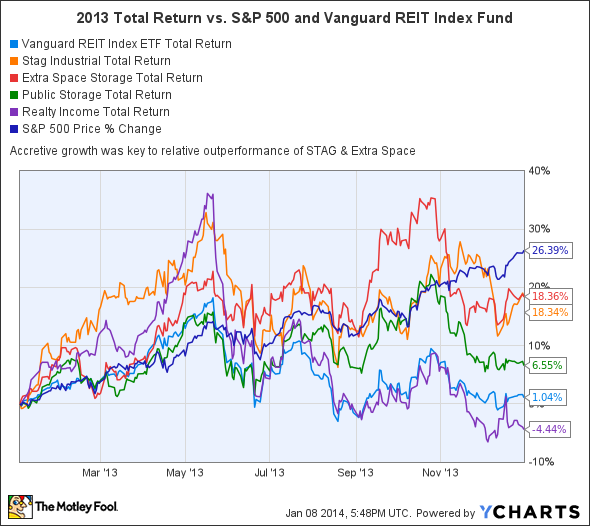

I find it hard to conclude otherwise when looking at the disparate results from last year. The growth component of a REIT -- as opposed to the dividend piece -- can substantially impact its total return and lead to outperformance.

The chart below clearly shows the smaller STAG Industrial , and Extra Space Storage holding up better than larger peers with strong balance sheets like Realty Income and Public Storage .

These stocks each outperformed the Vanguard REIT Index Fund by a whopping 17%, as well.

Do dividends explain it?

The relatively narrow range in the dividends above compared to the 17% outperformance of STAG and Extra Space clearly shows that dividends alone are not the answer. REITs that can significantly grow earnings while paying competitive dividends are better positioned to offset the headwinds of rising interest rate concerns.

Why growth matters to REIT investors

The ability to raise rents helps REITs keep pace with inflation and hopefully give shareholders slightly better returns. This organic or "same store" earnings growth is one way for investors to evaluate how well management is performing for shareholders.

However, the secret sauce for high total returns is a REIT management team that's able to steadily grow through acquisitions that are accretive to earnings.

Why size matters

Public Storage has a market cap of $25.7 billion. It is one of the largest publically traded REITs and has a fortress balance sheet with a very high, investment-grade rating. Last year, Public Storage announced the acquisition of 76 storage facilities for $716 million, with another 44 pending under contract, for a total of $1.15 billion. That sounds impressive, but it actually represents only a 4.47% increase for Public Storage.

Competitor Extra Space Storage, on the other hand, is the second largest self-storage REIT with a market cap of $4.69 billion. During 2013, Extra Space announced the acquisition of 30 properties for $294 million, plus another 57 properties pending under contract, for a total of $735 million. The projected growth from those deals is nearly 16%.

Extra Space is also the largest third-party manager with 253 self-storage facilities under management. In addition to fee income, this gives Extra Space a built-in acquisition pipeline moving forward.

A similar comparison can be made between single-tenant, triple-net-lease stalwart Realty Income -- sporting a $7.46 billion market cap -- and the much smaller $900 million STAG Industrial.

Realty Income generates its income from over 3,800 commercial properties located in 49 states and Puerto Rico. Although Realty Income grew significantly by acquisitions during 2013, investors may realize that it's unlikely to be able to duplicate that performance in 2014. There just aren't that many multibillion-dollar acquisition targets remaining in the single-tenant, triple-net-lease universe.

Meanwhile, for the calendar year ended 2013, STAG acquired 39 industrial facilities consisting of approximately nine million square feet for approximately $346 million. This annual acquisition activity increased the square footage of the portfolio by 31%. As this underscores, it is much easier to move the needle on a small- to mid-cap REIT by accretive acquisitions than it is to impact the growth rate of a larger-cap, more mature competitor.

STAG acquires single-tenant, class B industrial facilities in secondary markets. This investment strategy has few competitors with access to capital markets, which should bode well for its continued growth in 2014.

Investor takeaway

There certainly is a place in many portfolios for industry leaders, with strong balance sheets, that can consistently pay a dividend in good times or bad, like Public Storage and Realty Income. However, in a rising interest rate environment, I think investors should also consider smaller equity REITs that are well positioned for growth.

It's time to look beyond just comparing yields and focus on potential total returns. That means turning your sights to well-managed companies that are in that "sweet spot" of being large enough to have economies of scale, yet small enough for accretive growth to impact the bottom line.

Will this be your 2014 investing homerun?

There's a huge difference between a good stock and a stock that can make you rich. The Motley Fool's chief investment officer has selected his No. 1 stock for 2014, and it's one of those stocks that could make you rich. You can find out which stock it is in the special free report "The Motley Fool's Top Stock for 2014." Just click here to access the report and find out the name of this under-the-radar company.

The article Why Size Will Matter for These Stocks in 2014 originally appeared on Fool.com.

Bill Stoller has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2014 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.