Is It Time to Buy Industrial Supply Companies?

Last year was a difficult one for investors in industrial supply company Fastenal . The stock ended the year flat, and managed to underperform sector peers such as Grainger and MSC Industrial . Furthermore, the Institute for Supply Management, or ISM, manufacturing data got a lot stronger in the second half, but Fastenal's performance did not. What's going on? Can the market expect more from the company this year?

Fastenal disappoints, again

Having warned investors that it would miss quarterly earnings per share estimates of $0.36 in its update in December, Fastenal then managed to miss its upgraded estimate of "growth in net earnings per share" by reporting flat earnings growth of $0.33 for its fourth quarter.

Superficially, this is surprising given the strength of the ISM manufacturing data:

Source: Institute for Supply Management

In addition, MSC Industrial's management reported on its January conference call that feedback from its manufacturing customers "confirms the current theme of stabilization and gives us some cause for greater optimism about 2014."

So why did Fastenal miss esimates?

Fastenal adjusts its sales operations, gets heavy too

In the December update, Fastenal outlined the three reasons for the earnings miss.

First, despite the strong ISM numbers, Fastenal is having some issues with its particular end markets. The company generates 50% of its sales from manufacturing, 25% from non-residential construction and the rest from a diverse set of business. Within its manufacturing sales, heavy manufacturing makes up 80% of sales with heavy equipment making up half in turn. Be sure to distinguish between Fastenal's heavy manufacturing and its heavy equipment sales, the latter is a subset of the former.

All told, heavy equipment makes up 20% of total company sales and this segment was weak in 2013. In fact, Fastenal disclosed that heavy equipment sales (agriculture, mining, construction, defense, etc.) grew less than 2% in the third quarter, and only 1.5% in the fourth, even as heavy manufacturing sales were up "between 6% and 7%". The good news is that heavy manufacturing sales appear to be recovering (in line with the ISM) with a 7.2% in the fourth quarter following a 5% gain in the third.

Indeed, the theme was confirmed by MSC Industrial's management on its recent conference call: "Overall, we continue to see that our core customer segments in heavy metalworking are still lagging the broader industrial economy." Grainger also reported that its light manufacturing sales grew in "the high-single digits" in the third quarter, but its heavy, commercial and natural resources sales were only up "mid-single digits".

In addition, Fastenal's sales to non-residential customers have been weaker in 2013, as poor weather plus sequestration issues hit the commercial and industrial construction markets.

Source: company presentations.

Second, gross margins ran below expectations. According to Fastenal's December update, this was due to "lower utilization of our trucking network and lower supplier incentives", and "the final components relate to product mix (fasteners carry our highest gross margin and have had a weak 2013) and a very competitive marketplace".

In fact, fastener sales started 2013 by comprising 42.9% of total sales, but only made up 40.6% at the end of it. However, on the recent conference call, Fastenal's management outlined that gross margin is expected to get back to its historical 51%-52% range in the first quarter, recovering from a disappointing 50.6% in the fourth quarter of 2013.

The third factor was due to the expansion in store headcount made in the second half. Earlier in the year, Fastenal had outlined a plan to hire 600-900 more in-store staff in order to enable existing managers to increase their sales visits. In addition, there was a change of approach whereby the company went for quality over quantity with the expansion of its vending machines; a policy set to be reversed in 2014. It appears that the sales changes caused some initial problems, and Fastenal's management was quite upfront on the failure to execute in the second half.

Where next for Fastenal?

It's a mixed outlook for Fastenal.

On the positive side, 2014 it could be a better year for commercial construction, and the new orders component of the ISM manufacturing index (see above) indicates that manufacturing growth will be strong in the coming months. Furthermore, its gross margin looks set to bounce back, while its sales execution has the potential to improve.

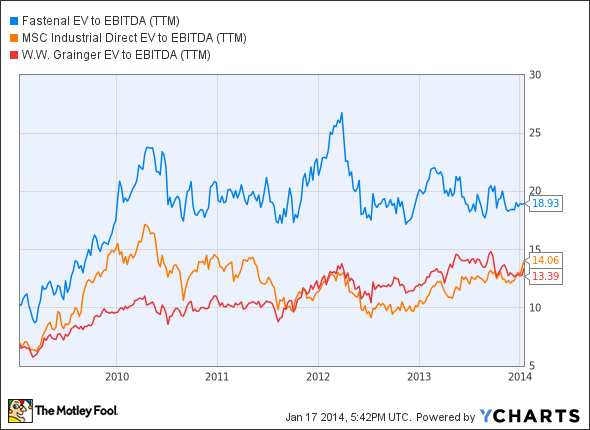

On the downside, the stock remain expensive related to its peers:

FAST EV to EBITDA (TTM) data by YCharts

Moreover, Grainger and MSC Industrial have the potential to grow their e-commerce revenues and vending machine sales, while sales to customers with vending machines already make up 36.6% of Fastenal's net sales.

In conclusion, the U.S. industrial sector looks like it will be healthy in 2014, and Fastenal is likely to bounce back, but there are cheaper ways to buy into the sector than this. The valuation is still not compelling.

Opportunities to get wealthy from a single investment don't come around often...

...but they do exist, and our chief technology officer believes he's found one. In this free report, Jeremy Phillips shares the single company that he believes could transform not only your portfolio, but your entire life. To learn the identity of this stock for free and see why Jeremy is putting more than $100,000 of his own money into it, all you have to do is click here now.

The article Is It Time to Buy Industrial Supply Companies? originally appeared on Fool.com.

Lee Samaha has no position in any stocks mentioned. The Motley Fool recommends MSC Industrial Direct. The Motley Fool owns shares of MSC Industrial Direct. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2014 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.