General Electric Company: Poised for Another Solid Year After Strong Earnings Report

General Electric's share price has risen to heights not seen since the stock market plunge in 2008. It's done this despite the company being in what analysts call a transitional period, shifting focus away from its finance division, GE Capital, and returning to its industrial roots. It's a move that's paying off quicker than expected, by the looks of its fourth-quarter earnings. Here are the details.

By the numbers

Starting from the top line, revenue was up 3% from fourth-quarter 2012 to $40.4 billion -- totaling $146 billion for the year. Fourth-quarter orders in the U.S. and Europe were up 13% and 3%, respectively, while margins increased 100 basis points. Improving margins helped General Electric post operating earnings of $5.4 billion, or earnings per share of $0.53 -- a 20% increase from last year's fourth quarter. GE's full-year operating earnings per share were up 9% to $1.64.

The numbers were in line with expectations, but the best takeaway for investors is that General Electric made the right move in returning focus to its industrial operations.

Industrial segment profits rose 12% to $5.5 billion, with six of seven segments reporting positive earnings growth. Infrastructure orders were up 8% to $30.7 billion in the fourth quarter, and General Electric's backlog of equipment and services hit a record high at $244 billion -- a $15 billion increase from the previous quarter.

GE Chairman and CEO Jeff Immelt said in a press release:

GE ended the year with strong fourth-quarter earnings and margin growth in an improving but mixed environment. We saw good conditions in growth markets, strength in the U.S., and a mixed environment in Europe. We had strong operating performance for the year and are pleased with our execution in 2013, taking $1.6 billion of cost out, growing margins, reducing the size of GE Capital, and returning more than $18 billion to shareholders.

Returning value

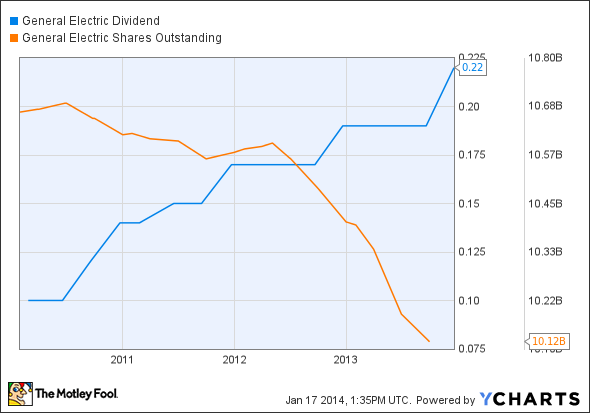

General Electric also kept to its theme of returning value to shareholders through multiple avenues. GE returned $18.2 billion to shareholders by paying $7.8 billion in dividends and repurchasing $10.4 billion of its stock. When shares outstanding and dividends are graphed it should form an "X" if the company is diligent in returning value to shareholders; dividends should consistently rise while shares outstanding should decline.

GE Dividend data by YCharts.

During the quarter, GE announced a 16% increase in its quarterly dividend -- its fifth increase in just more than three years.

General Electric generated $17.4 billion in cash from operating activities last year, with industrial operating activities accounting for $11.5 billion of that amount. With the company ending the quarter with $89 billion of consolidated cash and cash equivalents, shareholders can expect GE to keep returning value in 2014; it looks like it is going to be another strong year for GE.

Dividend stocks like GE can make you rich

One of the dirty secrets that few finance professionals will openly admit is the fact that dividend stocks as a group handily outperform their non-dividend paying brethren. The reasons for this are too numerous to list here, but you can rest assured that it's true. However, knowing this is only half the battle. The other half is identifying which dividend stocks in particular are the best. With this in mind, our top analysts put together a free list of nine high-yielding stocks that should be in every income investor's portfolio. To learn the identity of these stocks instantly and for free, all you have to do is click here now.

The article General Electric Company: Poised for Another Solid Year After Strong Earnings Report originally appeared on Fool.com.

Fool contributor Daniel Miller has no position in any stocks mentioned. The Motley Fool owns shares of General Electric Company. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2014 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.