Earnings Week: Bank of America and JPMorgan Still Look Cheap

Although we don't believe in timing the market or panicking over daily movements, we do like to keep an eye on market changes -- just in case they're material to our investing thesis.

On the back of a week in which stocks managed a nominal gain, the market opened mixed on Monday, with the S&P 500 down 0.01% and the narrower Dow Jones Industrial Average up 0.01% at 10:15 a.m. EST. This week arguably marks the "proper" start to 2014 as far as the stock market is concerned, with some key economic data and fourth-quarter earnings reports from no fewer than six Dow components:

Tuesday: JPMorgan Chase

Wednesday: American Express, Goldman Sachs, Intel, UnitedHealth

Friday: General Electric

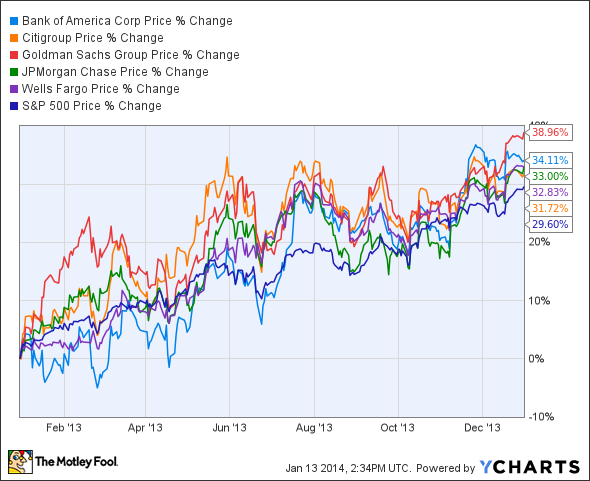

Outside of the Dow, Wells Fargo, Bank of America , and Citigroup will also announce results on Tuesday, Wednesday and Thursday, respectively. That will round out the reporting season as far as the top five U.S. banks are concerned. This group had a terrific year in 2013, with all five beating a roaring S&P 500 index on the basis of price return:

However, don't let that performance obscure the notion that there may yet be value left in this group. Robert Ewing, manager of the $5.5 billion Putnam Fund for Growth and Income, made the case for JPMorgan Chase and Bank of America [subscription required] in last weekend's edition of Barron's, and I'm inclined to agree with him. His thesis is that the costs and regulatory headaches these banks have faced as a result of the financial crisis are now subsiding, yet their valuations -- even after a big run-up in their stocks -- remain depressed:

[W]ithin [financials], there are still some opportunities, including JPMorgan. It is the cheapest big bank by any metric. It has a single-digit forward-earnings multiple, and it trades at 1.5 times tangible book value... There is no debating that there is more of that [settlements with regulators] to come. But the probabilities are quite high that the negatives have peaked and will slowly recede, and the franchise is performing better than all of the other big banks. JPMorgan reports results from seven segments, but we break it into 16 segments. And they are either maintaining or gaining share in 14 of those 16 segments. So, fundamentally, they are performing really well."

On a price-to-book value basis, Bank of America's stock is even cheaper, which sets a low hurdle for growth and profitability:

I'm not positive that they have to grow at very compelling rates. Bank of America, for instance, is trading at 1.2 times tangible book value, which would imply almost no growth. But these banks still have an engine to generate 12% to 13% returns on equity, long-term. And if they don't grow and they don't need that capital, then it can come back to shareholders in share buybacks and dividends, and that still is a pretty compelling value proposition.

Note that analysts typically use 10% as a benchmark for big banks' cost of equity, so a 12% or 13% return on equity would imply the organization is economically profitable and deserves to trade at a premium over its book value. What sort of premium? Ewing has an idea:

If they are capable of generating 12% to 13% returns over time, then they should trade at book-value multiples notably higher than where they are today. They deserve to trade at closer to two times book value. And in both cases, they are trading at single-digit forward [P/E] multiples, based on our estimates, and they should probably have low double-digit multiples.

Neither of these banks are the screaming buys they represented 12 or 24 months ago, but, in a market that is beginning to look a bit "toppy," they certainly look like compelling large-capitalization names.

The time to act is now: Here's the one stock you must own for 2014

There's a huge difference between a good stock, and a stock that can make you rich. The Motley Fool's chief investment officer has selected his No. 1 stock for 2014, and it's one of those stocks that could make you rich. You can find out which stock it is in the special free report: "The Motley Fool's Top Stock for 2014." Just click here to access the report and find out the name of this under-the-radar company.

The article Earnings Week: Bank of America and JPMorgan Still Look Cheap originally appeared on Fool.com.

Fool contributor Alex Dumortier, CFA has no position in any stocks mentioned; you can follow him on Twitter @longrunreturns. The Motley Fool recommends Bank of America. The Motley Fool owns shares of Bank of America and JPMorgan Chase. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2014 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.