1 Year After the Spin-Off, Abbott Laboratories Looks Like a Winner

In a bid to boost shareholder value Abbott Laboratories split itself in half a year ago. The company packaged its U.S. drug portfolio and pipeline into AbbVie , leaving it with its medical device and equipment products and responsibility for overseas drug sales.

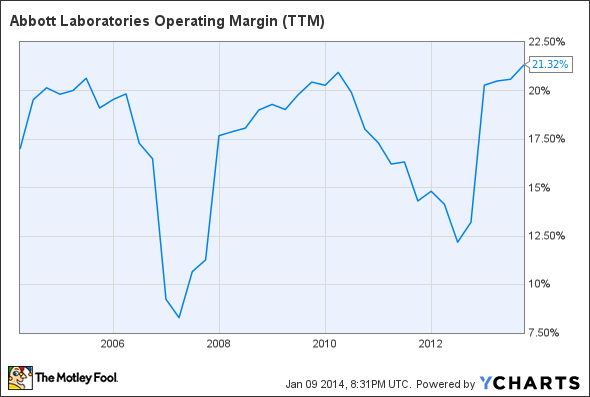

Addition by division

The split insulates the more stable growth business of selling infant formula, lab tools, and stents from the more volatile, hit-and-miss business of drug development. It allows less risk adverse investors to own Abbott for its steady growth in established markets and more risk tolerant investors to take a chance on emerging drugs in AbbVie's pipeline including treatments for hepatitis C and cancer.

It also helps Abbott capture more money from every dollar of sales thanks to freeing it from expensive drug R&D. That's helped Abbott's operating margin climb to more than 21% -- a ten year high.

ABT Operating Margin (TTM) data by YCharts

Abbott leveraged that higher operating margin against $5.3 billion in third quarter sales to produce earnings per share of $0.55, up from $0.42 last year.

The bulk of Abbott's business comes from its nutrition segment, which sells Similac infant formula and represents a little less than a third of the company's sales. That business saw sales grow 1.9% last quarter. However, growth would have been better if not for the overhang of a recall in China.

That recall gave competitor Mead Johnson a bit of a lift. Mead Johnson cited competitor recalls as one of the reasons its sales grew 21% year-over-year in its Asia/Latin America segment during the third quarter.

But Abbott's formula business should return to normal and sales should return to growth as wealthier emerging markets help lift the overall market for baby food and pediatric nutrition from $41 billion in 2012 to $64 billion in 2017.

The baby business may provide a steady revenue stream, but diagnostics is the fastest growing business at Abbott. Strong emerging market demand for infectious disease products drove molecular diagnostic products sales up 15% and domestic hospital sales helped point of care diagnostic sales expand 16.5%. That pushed combined sales of Abbott's diagnostics products up 8% from last year in the third quarter

Strength in diagnostics should continue as the market for molecular diagnostics is expected to nearly double by 2017.

That offers plenty of opportunity for Abbott, which is 4th in market share in the industry, to win business against Roche, which owns 32% market share, Myriad Genetics , and Qiagen.

Roche has built its leadership in diagnostics around blood testing products used by laboratories, hospitals, private physicians, and diabetics. 50% of Roche's diagnostics sales came from their professional diagnostics tools, while 25% came from diabetes blood glucose products in 2012. Roche also competes with Abbott in molecular diagnostics, which represents 11% of Roche's diagnostic sales.

Myriad has focused its portfolio on developing gene testing tools for cancer. Those tools can be used by doctors to evaluate patients for next generation therapies that specifically target genetic mutations like the BRCA gene. Myriad's BracAnalysis tool generates three quarters of its $166 million in third quarter sales.

In addition to growing its diagnostics business, Abbott is also deploying some of its cash to advance its medical devices segment and expand its presence in fast growing markets like peripheral artery disease, or PAD. Abbott acquired Idev for over $300 million earlier this year to gain Idev's flexible stents for use in leg angioplasty. Retiring baby boomers should make that a fast growing market given the chance of being diagnosed with PAD increases with age.

The deal positions Abbott up against Johnson & Johnson's Cordis and Medtronic. Johnson bought Flexible Stenting Solutions in March, 2013 to expand its S.M.A.R.T. product line that's gotten the FDA nod for use both above and at the knee.

Abbott and Johnson's deals reflect industry advances in creating flexible stents that bend with the body, expanding the opportunity to treat as many as 27 million patients who suffer from PAD in North America and Europe.

Outside of PAD, Abbott spent another $250 million acquiring OptiMedica and its automated equipment for cataract surgery. An aging population is expected to increase demand for femtosecond laser equipment, like those made by OptiMedica, from $572 million to $2.4 billion by 2019.

Fool-worthy final thoughts

So far, the split up gets high marks for increasing shareholder value. Both AbbVie and Abbott have seen their share prices march higher in the past year. That trend could continue for Abbott given the company's stable growth and improving cash flow should support dividend hikes. The company increased its dividend payout 57% to $0.22 per share for the first quarter of 2014, marking its 42nd year of dividend increases.

Interested in dividends? Here are 3 important dividend paying companies for 2014

If you're looking for some long-term investing ideas, you're invited to check out The Motley Fool's brand-new special report, "The 3 Dow Stocks Dividend Investors Need." It's absolutely free, so simply click here now and get your copy today.

The article 1 Year After the Spin-Off, Abbott Laboratories Looks Like a Winner originally appeared on Fool.com.

Todd Campbell has no position in any stocks mentioned. Todd owns E.B. Capital Markets, LLC. E.B. Capital's clients may or may not have positions in the companies mentioned. Todd also owns Gundalow Advisor's, LLC. Gundalow's clients do not own positions in the companies mentioned. The Motley Fool recommends Johnson & Johnson and Qiagen. The Motley Fool owns shares of Johnson & Johnson and Medtronic. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2014 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.