Should You Stay Away From Solar Stocks in 2014?

2011 and 2012 were absolutely horrible for solar investors. China's policy of heavy subsidization of its domestic solar manufacturers nearly crippled many American companies, pushing prices so low that every panel sold was a money loser for some makers. Over those two years, SunPower (NASDAQ: SPWR), First Solar (NASDAQ: FSLR), and GT Advanced Technologies (NASDAQ: GTAT) shareholders lost between 57% and 77%:

SPWR Total Return Price data by YCharts

The backlash included the U.S. instituting tariffs on panels made by Chinese firms, and for Chinese panel maker Trina Solar (NYSE: TSL), its stock was punished to the tune of 82% of its market value as these tariffs weighed heavily on an already narrow profit margin, pushing the company well into the red.

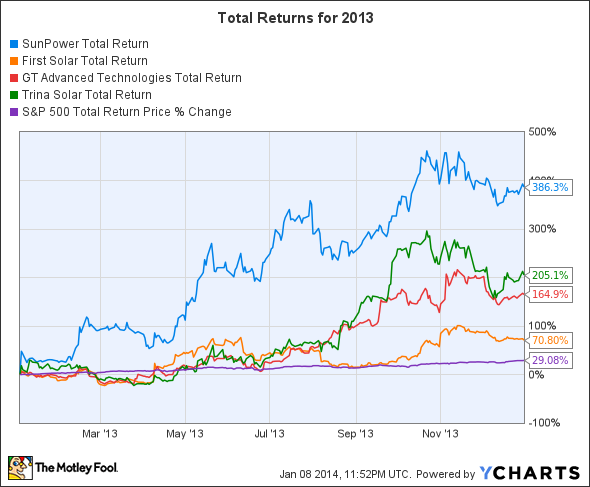

However, 2013 painted a different picture, with shares of all four companies skyrocketing:

SPWR Total Return Price data by YCharts

After a strong bounce-back year, what should investors do in 2014? Is the solar bubble going to burst again? Let's take a closer look.

Merci beaucoup

SunPower was in serious trouble in early 2011, when French energy giant Total S.A. stepped in with a massive $1.46 billion equity stake (it owns 66% of SunPower) that provided both much-needed liquidity, and a gorilla fighting in its corner. The partnership with Total -- besides saving the business -- has led to a number of large deals, including a recent 86Mwp solar plant it will build in South Africa.

Today, SunPower has reached the point where it is actually having to add additional production capacity. In the Q3 earnings call, CEO Thomas Werner made it clear that fabrication was at a point where the company had no choice but to add capacity, having run at full capacity in the second and third quarters, and anticipating the same for Q4. The plan is to build an additional 25% in capacity at a cost of $160 million-$230 million, while simultaneously adding 10% more capacity to existing fabrication lines.

Finding its competitive side

First Solar also saw some real positives over the first nine months of 2013, particularly in its ability to drive down costs while also increasing utilization at its manufacturing facilities. CFO Mark Widman highlighted this on the earnings call:

In the third quarter, we ran our factories at approximately 80% capacity utilization, up five percentage points from the prior quarter ... We have reduced our module manufacturing cost per watt to $0.59 from $0.67 last quarter, an $0.08 per watt or 12% reduction quarter-on-quarter. This is the best quarter-over-quarter cost improvement in six years on a per watt basis and highest percentage reduction since our IPO.

Revenue for the fourth quarter was revised down slightly; it's the company's ability to make money that's really the key.

It's not really about solar for GT Advanced Technologies anymore

GT Advanced Technologies' big year isn't really about solar at all. Management has been promising great things from its Sapphire business for the past couple of years, and patient investors (or speculators buying at $5) learned that sometimes, management can be trusted when it announced a big deal with Apple to make Sapphire components in the new manufacturing plant being built in the U.S., shooting the stock up 20% the day of the announcement. While the market has given back some of those gains, the real value of this deal won't be apparent for as long as a year from now.

If GT Advanced can land a few more big deals like this one, it could be transformative for the company once called GT Solar.

Metrics that matter: Did the lost value go away for good?

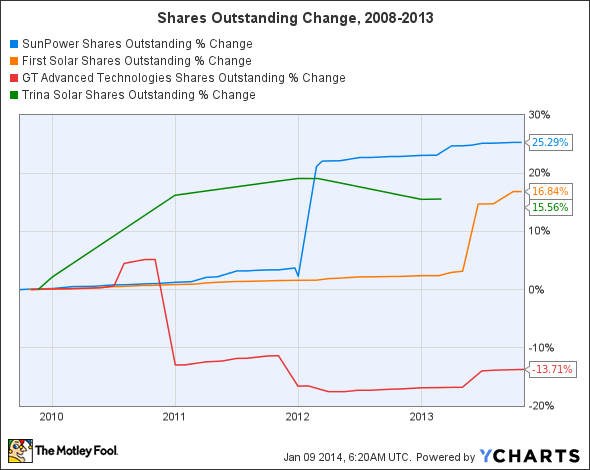

Let's finish by taking a little longer view, and adding some context to properly evaluate what's happened with the share price as compared to the change in shares outstanding:

SPWR Total Return Price data by YCharts

These stocks all have a long way to go to fully recover from 2008. However, it's important to understand that share price movement can be a product of more than just the company losing value:

SPWR Shares Outstanding data by YCharts

As you can see, shares outstanding has increased for all of these companies, due to public offerings to raise cash and stock-based employee compensation. While to some extent this is an ordinary course of business -- especially for businesses that need to use stock as currency to fund growth -- it dilutes current investors, making it that much harder to recoup losses when things go bad, and watering down gains when things go well.

The point? All things created equal, these companies have to generate at least the percentage in dilution in additional earnings to get investors back to even -- and that's assuming that the companies are all valued the same by the market, which isn't a given.

Where from here?

While expecting another 2013 is unreasonable, and expecting shares to get back to 2008 levels in 2014 is probably a stretch, the solar industry and the global economy are much healthier than before the recession. That bodes well for -- if not 2013 again -- a good chance at market-beating returns.

SunPower and First Solar seem to be in the best positions to grow and be profitable, while Trina's thin (but expanding) margins point to one or two profitable quarters, so it's a coin-toss how the market responds.

GT Advanced Technologies is definitely the speculative play, with its value today sustained almost exclusively on the Apple deal. Caveat emptor: a small bite isn't unreasonable, but expect a bumpy ride.

What will drive the U.S. economy for the next century? It's bigger than solar by far...

U.S. News & World Report says this "Will drive the U.S. economy." And Business Insider calls it "The growth force of our time." In a special report entitled "America's $2.89 Trillion Super Weapon Revealed" you'll learn specific steps you can take to capitalize on this massive growth opportunity. But act now, because this is your shot to cash in before the fat cats on Wall Street beat you to the potentially life-changing profits. Click here now for instant access to this free report.

The article Should You Stay Away From Solar Stocks in 2014? originally appeared on Fool.com.

Jason Hall owns shares of, GT Advanced Technologies, and January 2015 calls of GT Advanced Technologies.. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2014 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.