Can Visa Justify its New Place on the Dow in 2014?

It's been just more than four and a half years since the Dow Jones Industrial Averagebottomed out in the spring of 2009. Since the index's lowest ebb, its overseers have replaced six components and the Dow has surged from below 7,000 points to more than 16,000 points for the first time in its history.

Due to the index's price-weighting structure, some stocks have had a far greater impact on that rise than others. Going forward, none are likely to have more effect on the Dow's movements as Visa , one of three new additions this year. Visa's current $220 share price gives it the Dow's largest weighting, which is currently calculated at 8.6% of the index's value. This means that, despite enjoying less growth than fellow Dow credit card issuer American Express both this year and since the Dow's rebound began in 2009, Visa is all but certain to exert a greater influence on the index in 2014:

V Total Return Price data by YCharts.

Being the Dow's second-best-performing financial stock this year is no small feat in a year (and a rebound) full of financial outperformance, but Visa's stock performance in the year ahead will be the most important of its relatively brief public life. Another strong showing may well push the Dow out of a decade-plus secular bear market for good -- the index finally broke through an inflation-adjusted high, set at the end of the dot-com boom, shortly before Christmas, but it's a little too early to declare that bullish times are here to stay. If Visa's stock grows even half as much in 2014 as it did this year, the Dow could very well move toward (or beyond) 17,000 points by next Christmas.

But how likely is it that Visa will continue to thrive in 2014? One way to find out is to consider what Wall Street expects going forward and how that stacks up to Visa's previous growth.

The year ahead: by the numbers

Visa has seen its bottom line grow substantially coming out of the recession; thanks to the end of the one-time impact of a multibillion-dollar legal settlement, its latest full-year results look even more impressive. However, analysts now expect the weakest growth on Visa's bottom line in years for 2014:

Fiscal Year | Earnings Per Share | Year-over-Year Growth Rate |

|---|---|---|

2010 | $4.01 | 96.6% |

2011 | $5.16 | 28.7% |

2012 | $3.16 | (38.8%) |

2013 | $7.59 | 140.2% |

2014 * | $8.89 | 17.1% |

Sources: Morningstar and company press releases.

* 2014 EPS and growth rate are based on analyst estimates for the upcoming year.

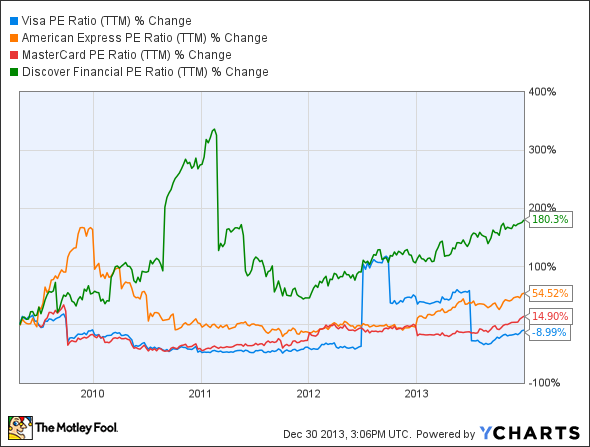

It's quite possible that Visa will beat the Street's expectations next year, as it has a long history of surpassing estimates. However, the company met estimates on the nose in its latest quarter, for the first time since the rebound began, so more dour investors could take that one disappointment as evidence of a change in the trend. Long-term investors know better than to panic over one underwhelming quarter -- but does Visa have the chops to justify a year of 20% share-price growth in 2014? The answer seems more likely to be yes than no, as Visa is the only one of the four major credit card issuers to have experienced a valuation decline since the official start of the Dow's post-crisis rebound:

V P/E Ratio (TTM) data by YCharts.

That doesn't necessarily mean that Visa is necessarily cheap, though -- its actual P/E ratio (29) is within striking distance of MasterCard's 33 P/E. and it's roughly three times Discover Financial's P/E of 11. Price to free cash flow is an uglier metric for Visa as compared to its peers, as the Dow's latest addition still boasts a P/FCF of nearly 57, compared to MasterCard's 29 and Discover's puny P/FCF of 8. However, it's important to remember that this metric is still elevated by the impact of its swipe-fee settlement; when we adjust for that write-off, Visa's P/FCF would be closer to 20, which would be lower than either MasterCard's or American Express' results. When we take these new facts into account, Visa begins to look like a much better value, and its story for the upcoming year again appears to support outsized growth -- at least 17%, if investors (and the company) simply follow expectations through the coming year.

Beat the market by thinking small in 2014

There's a huge difference between a good stock, and a stock that can make you rich. The Motley Fool's chief investment officer has selected his No. 1 stock for 2014, and it's one of those stocks that could make you rich. You can find out which stock it is in the special free report: "The Motley Fool's Top Stock for 2014." Just click here to access the report and find out the name of this under-the-radar company.

The article Can Visa Justify its New Place on the Dow in 2014? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more insight into markets, history, and technology.The Motley Fool recommends American Express, MasterCard, and Visa. The Motley Fool owns shares of MasterCard and Visa. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.