Why Micron Technology Stock Skyrocketed 240% In 2013, and What's Next

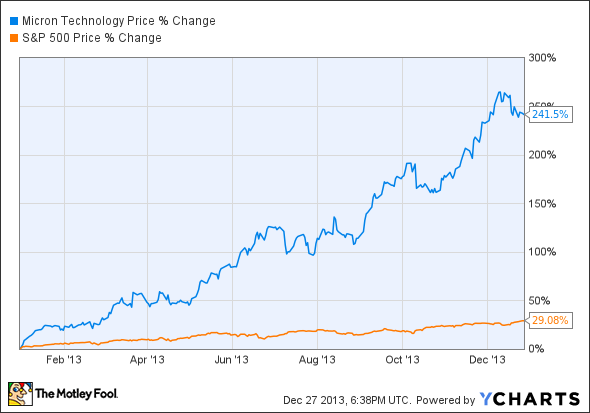

Shares of computer memory maker Micron Technology are up 240% in 2013. The stock not only beat the S&P 500 index, but was the third strongest performer among its 500 tickers.

How did Micron reach this lofty pinnacle in 2013?

Micron finally closed the game-changing acquisition of bankrupt rival Elpida this summer, after more than a year of painful regulatory wrangling in Japanese courts and government bureaus. The $2.5 billion deal could have fallen apart at several points along the way, which explains why Micron investors didn't bid the stock up in 2012. Too much uncertainty, and the Elpida thing really needed to happen.

It's not exactly fair to say that the entire 240% surge rested on Elpida. The company is already a proven winner in the rapidly consolidating memory industry, after all. But there's no way the shares would have soared 240% without this buyout. I did call it "game changing" already, and I mean it.

Here's how the buyout changed the game in DRAM manufacturing and sales:

DRAM Market Shares Before and After the Elpida BuyoutCreate infographics

Separately, Micron and Elpida were minnows next to the giant Samsung and Hynix sharks. Together, they wield a much larger market share with all the efficiencies and clout that entails.

So, here's what's happening now. In a market known for its brutal and lengthy price wars, the reformed Micron now wields substantial control over the supply side of the supply-and-demand equation. Samsung doesn't mind driving prices down, since memory chips are just a hobby for the Korean electronics giant. Micron and Hynix, on the other hand, would love to put the brakes on the manufacturing lines to keep unit prices healthy.

Elpida never had that luxury, given that it was fighting a losing battle of survival, and needed every available penny of top-line sales. But with Micron's solid balance sheet at its back, Elpida's portion of the global DRAM market is indeed taking a breather. In fact, Micron is converting some of Elpida's old DRAM operations to make more lucrative NAND flash chips instead.

Micron is finally allowed to take the lessons learned in the lean years, and apply them to a stronger market that's more in Micron's own control.

On that note, expect Micron's compressed profit margins to spring back to life. Analysts already predict $2.09 of net earnings per share in the 2014 fiscal year, up from a $0.18 loss per share in 2013.

MU Gross Profit Margin (TTM) data by YCharts

I'm a Micron shareholder myself, with no plans of selling my shares in 2014. I can't wait to see this well-managed company deliver on the promises of the Elpida-fueled makeover.

So, 240% isn't enough for you? Check out these six picks for ultimate growth in 2014

They said it couldn't be done. But David Gardner has proved them wrong, time, and time, and time again, with stock returns like 926%, 2,239%, and 4,371%. In fact, just recently, one of his favorite stocks became a 100-bagger. And he's ready to do it again. You can uncover his scientific approach to crushing the market and his carefully chosen 6 picks for ultimate growth instantly, because he's making this premium report free for you today. Click here now for access.

The article Why Micron Technology Stock Skyrocketed 240% In 2013, and What's Next originally appeared on Fool.com.

Fool contributor Anders Bylund owns shares of Micron Technology. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.