What Will Cisco Do in 2014?

Cisco Systemsis having a rough year. Shares of the networking equipment builder are up just 6% in 2013, while its Dow Jones peers as a whole have risen 23%. The company beat earnings estimates in each of the four quarterly reports this year, but often followed up with weak guidance.

Can Cisco bounce back from this disappointing performance next year, or will 2014 be another 12 months of frustration for Cisco shareholders?

Cisco by the numbers

Analysts expect Cisco to report adjusted earnings close to $2 per share in calendar year 2014, which is no change from late-stage 2013 estimates. Revenue is seen shrinking 2% to roughly $47 billion.

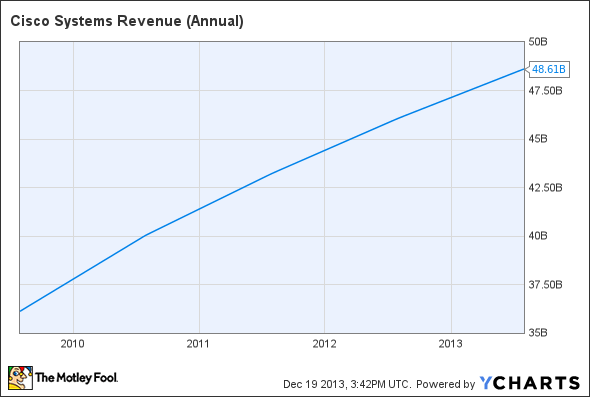

Last week, Cisco CFO Frank Calderoni reduced his long-term revenue growth targets from approximately 6% a year to something more like 4.5%. His earnings targets remain close to Wall Street's estimates, but the current streak of 15 quarters with year-over-year revenue growth is going to end this month.

That's a scary prospect when your recent revenue history looks like this:

CSCO Revenue (Annual) data by YCharts.

The Cisco story, in English

Let's hear it straight from CEO John Chambers. Speaking at last week's annual investor confab, Chambers spelled out exactly how he's looking at 2014:

This next year will be the year of architectures. What's going to be the key turning point this year is, it won't be about architectures by business entity group. It's about how you work horizontally across all the business entities to solve your customers' problems.

Chambers has seen smaller rivals unexpectedly steal a few juicy contracts. Recently, Alcatel-Lucent has come back from death's door to land several large-scale equipment contracts in key growth markets like China and Latin America. Cisco won't fight back against these incursions by dropping prices and sacrificing margins. Instead, Chambers wants to impress potential customers with the integrated depth of his company's product portfolio. Cisco wants to be the one-stop shop for all your information-technology needs, and not just networking.

If that model sounds familiar, you've been following IBM over the last couple decades. The new Cisco looks a lot like the old IBM, even as Big Blue is working its way into a more focused business model.

So that's the plan for 2014. Big strategy shifts often include temporary roadblocks, as Cisco's revenue forecasts are showing. Fellow Fool Tim Green says that this is the perfect time to buy Cisco shares, as investors worry far too much about Cisco's ability to execute.

If you agree that Cisco is likely to work its way back from today's challenges, the stock certainly looks tempting. But I can't blame you for taking a "wait and see" approach, either. Cisco has a lot to prove right now and a track record of fumbles in the last five years.

Is Cisco building a business for the next 100 years?

It's no secret that investors tend to be impatient with the market, but the best investment strategy is to buy shares in solid businesses and keep them for the long term. In the special free report, "3 Stocks That Will Help You Retire Rich," The Motley Fool shares investment ideas and strategies that could help you build wealth for years to come. Click here to grab your free copy today.

The article What Will Cisco Do in 2014? originally appeared on Fool.com.

Fool contributor Anders Bylund has no position in any stocks mentioned. The Motley Fool recommends Cisco Systems. The Motley Fool owns shares of International Business Machines. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.