Goldman Sachs in 2014: Don't Expect the Same Returns

Although we don't believe in timing the market or panicking over daily movements, we do like to keep an eye on market changes -- just in case they're material to our investing thesis.

Historically, investment bank Goldman Sachs cultivated discretion and shunned media attention, but the aftermath of the financial crisis has blown that strategy wide open -- the company has gone from operating behind closed doors to becoming a household name. S&P Dow Jones Indices' Index Committee capped that transformation in September by adding Goldman to the venerable Dow Jones Industrial Average . As the bank achieves a new level of exposure, more investors are asking: What's in store for Goldman Sachs in 2014? Here are x things on the bank's radar for next year:

The business: Operating in a "taper" world

On Wednesday, the Fed announced that it will begin to scale back its monetary accommodation by reducing its monthly securities purchases from $85 billion to $75 billion, starting in January. Since the securities in question are a roughly equal mix of mortgage and Treasury securities, the largest effect of the Fed's "taper" ought to be in bond markets, an area in which Goldman Sachs is a dominant actor.

It's difficult to try to gauge the "all-in" impact of the "taper" as there are countervailing effects. On the one hand, the Fed's decision acknowledges that overall economic and financial uncertainty has decreased, along with the risk of financial calamity. The economic recovery appears to be gaining some traction and politicians are behaving more sensibly. That ought to be good for M&A volumes if executives' and boards' animal spirits begin to return. In mid-October, Goldman CFO Harvey Schwartz told investors and analysts that the firm's investment banking backlog "improved to its highest level in five years" during the third quarter.

However, while uncertainty may have fallen, it's quite possible that volatility will increase next year from current levels, which is low by historical standards (just take a look at a long-term chart of the VIX Index). The Fed has managed to suppress volatility to an impressive degree, but as it begins to unwind its extraordinary policies, it's reasonable to assume that will not last.

Increased volatility could take a toll on equity and bond underwriting. Furthermore, the Fed's bond-buying program may well have brought corporate bond issuance forward into 2012 as companies seized their window of opportunity to lock in low rates. In a Financial Times article published on Monday, Jonny Fine, Goldman's head of investment grade syndicate in the Americas called 2013 "the voracious year." Indeed corporate bond sales hit a record mark this year, at $1.1 trillion.

That said, while bond issuance may fall, Goldman could reap market share gains to make up the difference. Morgan Stanley and UBS, judging the profits too meager in the context of higher capital requirements, are scaling back their activity in this area.

And speaking of record highs, many investors believe that this year's stock market rally owes much to the Fed; whether or not that is true, it's hard to imagine that we'll see the same type of performance repeated in 2014, which brings me to Goldman Sachs' stock.

The stock: Lower your expectations for 2014

Before I speak about the stock, I want to remind readers that one year is far too short a time frame for a prediction per se -- the degree of randomness is simply too high. However, it is possible to say something about valuation and speak in terms of reasonable expectations, even as one acknowledges that actual outcomes may end up differing widely.

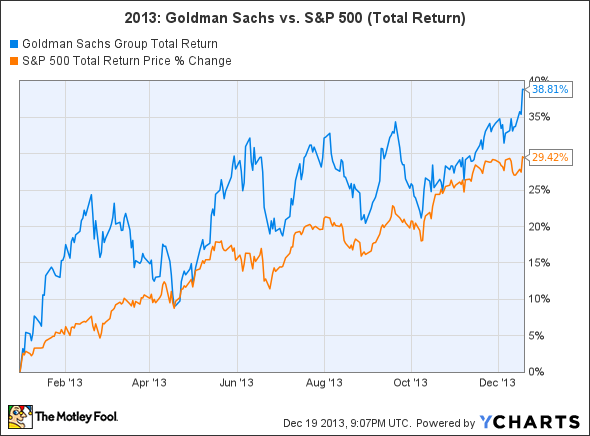

For context, shares of Goldman Sachs solidly outperformed those of their large-capitalization peers this year (see graph below), notching up a very respectable 39% total return through Wednesday. Interestingly, however, over the past five- and 10-year periods, Goldman's total returns have roughly tracked those of the S&P 500 -- 133% vs. 128% over five years and 104% vs. 100% over 10) -- albeit with significantly higher volatility.

GS Total Return Price data by YCharts.

If the shares are to deliver strong returns next year, it will likely be on the back of multiple expansion rather than earnings growth, as analysts expect low- to mid-single-digit earnings-per-share growth next year and in 2015, respectively. As of Wednesday's close, Goldman shares trade at 12.1 times next 12 months' earnings-per-share estimate -- a healthy discount to the S&P 500's 15.3 multiple. Let's assume the S&P 500 is fairly valued, is that discount warranted or ought we to expect Goldman's multiple to rise? I think it is warranted, for several reasons.

First, as mentioned above, Goldman shares have historically been more volatile than the broad market. Second, by its nature, the business is inherently riskier than the average large-cap enterprise -- 2008 was a powerful demonstration of that. Third, although Goldman is highly profitable, an extraordinary share of its profits are siphoned off by its employees. Once you get down to earnings attributable to outside shareholders, the profitability/ returns are relatively pedestrian. Fourth, the full impact of the new banking regulations (including the newly released Volcker rule, which bans proprietary trading) is not fully understood.

Bottom line

Goldman Sachs is an unusual business, which remains the best-of-breed among investment banks. Although the financial environment could be tricky to navigate next year -- both in terms of regulation and the state of the markets themselves -- I think one of Mr. Schwartz's quotes from the most recent earnings call is applicable here:

... we've seen some pullback from some competitors. I think that's a multi-year phenomenon as it relates to the impact of regulation... The real differentiating characteristics firm by firm -- and we all will live with the same rules, we'll have all the same resources -- is which firm can better deliver to their clients and which firm can better adapt.

I believe that Goldman is a bit smarter and more adaptable than its competitors and that ought to keep it ahead of the pack next year (and for the foreseeable future.) However, I don't think investors should expect the same performance from the stock in 2013 that it managed to produce in 2012, and the same could be said for the broad market.

Goldman beat the market in 2013; here's the one stock to own for 2014

There's a huge difference between a good stock, and a stock that can make you rich. The Motley Fool's chief investment officer has selected his No. 1 stock for 2014, and it's one of those stocks that could make you rich. You can find out which stock it is in the special free report: "The Motley Fool's Top Stock for 2014." Just click here to access the report and find out the name of this under-the-radar company.

The article Goldman Sachs in 2014: Don't Expect the Same Returns originally appeared on Fool.com.

Fool contributor Alex Dumortier, CFA has no position in any stocks mentioned. The Motley Fool recommends Goldman Sachs. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.