Are Activist Hedge Fund Shareholders Just Throwing Tantrums?

Activist shareholders are getting restless, but is it really a desire for change that's motivating these moves, or more a need to have their egos stroked?

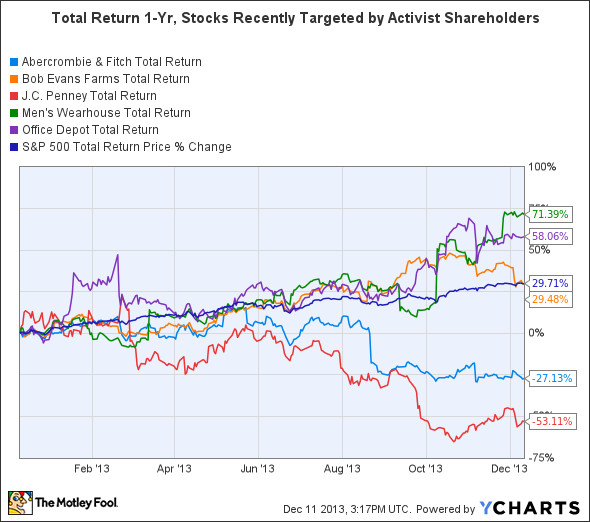

In recent weeks we've seen hedge fund operators that own large stakes in retailers like Men's Wearhouse and Abercrombie & Fitchstomp their feet in indignation when the boards of directors didn't give them what they want, but earlier we saw Bill Ackman pack up his marbles at J.C. Penney and go home after the board refused to dump replacement CEO Myron Ullman fast enough as the two differed over direction.

And when Office Depot delayed its annual shareholder meeting during its merger with OfficeMax, Starboard Value had a hissy fit and said it was taking the call to action directly to shareholders.

Now Sandell Asset Management is threatening to hold its breath and turn blue after Bob Evans Restaurants rejected its demands to spin off its restaurant business, saying it will file a consent solicitation that gives it the right to have all shareholders vote on a proposal without waiting for the next annual meeting. Analysts think it will call for changes in the election of directors.

According to Institutional Shareholder Services, there have been 35 proxy campaigns in 2013 through November, up from the 27 waged last year, though less than the 43 battles that were fought in 2009.

In many cases the hedge fund operators have good cause to throw tantrums. Boards of directors often have a tendency to circle the wagons when agitators lob pointed questions their way or point to their mismanagement that brought about the dismal performance that attracted the activist shareholders in the first place. One of their favorite defenses is the poison pill, which typically triggers massive dilution if someone acquires too large a stake in a company. That it also entrenches the management team is not merely just a side benefit.

Men's Wearhouse had rejected outright a $2.3 billion offer from Jos. A. Bank saying it was a lowball bid, but then it adopted one of those poison pill defenses and refused to enter negotiations even after its rival said it would be willing to up the offer. Hedge fund operator Eminence Capital was livid that the board had seemingly reneged on its promise to engage in a good-faith effort to explore the potential of a tie, particularly after the men's clothier withdrew its offer. Of course, Men's Wearhouse has now gone and turned the tables and made a bid for Jos. A. Bank, but the special shareholders meeting Eminence initiated for February to shake up the board is still on track, and Bank has no intention of responding anytime soon.

Similarly, Engaged Capital was incensed that not only did Abercrombie's board reject its suggestion that it replace CEO Michael Jeffries when his contract expires in February, but that the board apparently thought it necessary to announce its decision within a week of getting the proposal. Because there are still a few months yet before the deadline arrives, the timing was seen as a means of highlighting just how deeply the board was ridiculing the idea. Engaged said it would be considering all of its options.

Yet the interests of hedge funds aren't exactly aligned with those of other common shareholders. They have their own investors they need to massage with returns, and those investment timelines may not have the same long-term horizon others have. The hedge funds typically want to get in and get out in a few years' time.

For J.C. Penney, its saga has been extensively chronicled, but it was Ackman who had been behind the overhaul of the department store chain and it was his hand-picked CEO, Ron Johnson, who has been fingered as the main culprit behind Penney's spectacular decline. After the board decided to bring its once and future CEO Ullman back on board on an interim basis, Ackman clashed with them over how fast he should be replaced, and in a fit of pique, ultimately declared he had lost faith in the board and its chairman and was selling his entire stake at a loss.

At a time when the market has returned almost 30% over the past year, the hedge funds are looking to juice the results of their lagging investments.

ANF Total Return Price data by YCharts.

Activist shareholders definitely have a role in shaking things up at stagnating companies that have grown complacent with their own underachieving status. Yet not every proposal they put forth is worthy of consideration, and sometimes the changes that management unveils need time to work.

Simply stomping their feet and threatening to go directly to shareholders because their pet project was rejected doesn't necessarily mean that what the hedge funds wanted is what outside shareholders need.

Change for change's sake

Warren Buffett has made billions through his investing and he wants you to be able to invest like him. Through the years, Buffett has offered up investing tips to shareholders of Berkshire Hathaway. Now you can tap into the best of Warren Buffett's wisdom in a new special report from The Motley Fool. Click here now for a free copy of this invaluable report.

The article Are Activist Hedge Fund Shareholders Just Throwing Tantrums? originally appeared on Fool.com.

Fool contributor Rich Duprey owns shares of Abercrombie & Fitch Co. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.