Investors Should Reconsider Sysco

Have you ever eaten food at an educational facility, summer camp, or hotel? If by some miracle the answer to that question is "no," then how about a restaurant? If you have eaten at any of these locations in your life, then there's a good chance that you have consumed Sysco products. Most importantly from an investing standpoint, this also means that you have supported the company's top line somewhere along the line.

In fact, despite economic headwinds and unfavorable industry trends, Sysco delivered $44 billion in sales in fiscal year 2013, a record for the company. Between the aforementioned types of locations that buy products from Sysco as well as health care facilities, it has 425,000 customers. That's a lot of business. Now imagine if Sysco grew its annual sales to $65 billion. Thanks to its recent merger with US Foods, this is now a realistic possibility. It's also likely to lead to increased potential for investors. Let's take a closer look.

Deal facts and expectations

US Foods is the 10th largest private company in the United States with $22 billion in annual revenue. Therefore, this deal will unite two of the largest food distributors on the planet. The deal has already been approved by both boards, so no worries there.

Sysco is paying $3.5 billion in stock and cash for equity in US Foods, and it will refinance US Foods' debt of $4.7 billion. The deal is expected to be immediately accretive to earnings for Sysco. It should also lead to $65 billion in annual sales, $2 billion in annual operating cash flow generation, and annual synergies of $600 million within three to four years.

In regards to the annual operating cash flow, this is an increase over Sysco's current annual operating cash flow of $1.47 billion. This will likely mean increased shareholder returns in the form of dividends and/or stock buybacks. Sysco is very reliable in this regard, having paid a dividend in every quarter since 1970. It has also increased its dividend 45 times since going public. The 46th dividend increase should be right around the corner.

Reasons for the deal

Sysco is highly focused on maintaining and growing customer relationships, and this deal gives the company an opportunity to establish more high-quality relationships. This deal will also offer Sysco geographic expansion opportunities, an improved supply chain, a broader product portfolio (including exclusive brands Chef's Lane and Rykoff Sexton), and the opportunity to maximize cost-cutting opportunities due to overlapping general and administrative functions.

Despite the positive expectations, there's no guarantee that Sysco will be the top investment option in food distribution going forward.

Other food distributor opportunities

Even after Sysco's stock price shot up north of 12% based on the merger news, it's still cheaper than United Natural Foods and Chef's Warehouse . Sysco is currently trading at 23 times forward earnings, whereas United Natural Foods and Chef's Warehouse are trading at 25 and 27 times forward earnings, respectively. Furthermore, Sysco's cash flow generates a yield of 3.40%. United Natural Foods and Chef's Warehouse don't offer any yield.

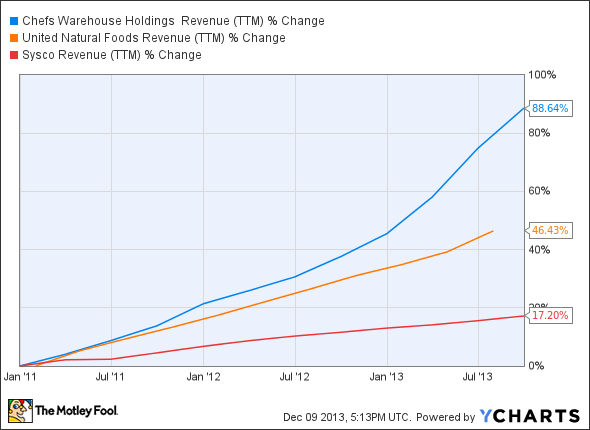

On the other hand, United Natural Foods and Chef's Warehouse have been growing faster over the past three years:

CHEF Revenue (TTM) data by YCharts

However, there are different reasons for growth at these companies. For United Natural Foods, a distributor of natural foods, it's due to the company being on-trend thanks to the rise of the health-conscious consumer. With 65,000 products across six categories, the company is also broadly diversified.

For Chef's Warehouse, the growth has been primarily related to the strength of the high-end consumer. Chef's Warehouse is a specialty food product distributor to fine-dining establishments, country clubs, upscale hotels, and any other public locations where people might consume specialty cheeses, unique oils and vinegars, and the like. While this trend remains intact at the moment, many high-end consumers rely on the performance of financial markets, which makes Chef's Warehouse less resilient than Sysco or United Natural Foods.

The bottom line

If you're looking for moderate growth and a very reliable dividend, then you might want to consider Sysco. The recent merger also proves that Sysco is proactive instead of reactive. If you would prefer a faster-growing company that's on-trend and likely to see sustainable success, then you might want to take a look at United Natural Foods.

Investing for the long haul

As every savvy investor knows, Warren Buffett didn't make billions by betting on half-baked stocks. He isolated his best few ideas, bet big, and rode them to riches, hardly ever selling. You deserve the same. That's why our CEO, legendary investor Tom Gardner, has permitted us to reveal The Motley Fool's 3 Stocks to Own Forever. These picks are free today! Just click here now to uncover the three companies we love.

The article Investors Should Reconsider Sysco originally appeared on Fool.com.

Dan Moskowitz has no position in any stocks mentioned. The Motley Fool recommends Sysco. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.