Abercrombie & Fitch: Status Update

Abercrombie & Fitch hasn't been popular among investors or consumers over the past year. Over this time frame, the stock has lost 24.1% of its value. American Eagle Outfitters and Aeropostale have suffered similar fates, seeing stock declines of 22.9% and 36.3%, respectively. At one time, all three companies sold apparel that was in high demand.

However, today's value-conscious consumer has little interest in spending on expensive, to-be-seen-in attire. This might be cyclical, and it's possible that all three companies will find ways to rebrand themselves to regenerate demand. If that's the case, it might be a long road back. In the case of Abercrombie & Fitch, current headwinds are a little more complicated.

Unfit and uncool on the top line

In Abercrombie & Fitch's third quarter, net sales dropped 12% to $1.0 billion year over year. The "good" news is that there is an area of hope. That area doesn't appear to be in the United States, where younger consumers are looking for thrifty apparel. Domestic sales slid 18% to $674.9 million. International sales weren't as depressing, declining only 2% to $358.4 million.

Abercrombie & Fitch has stated that it expects its weak top-line performance to continue throughout the fourth quarter. Apparently, the company's plan to fix this problem is to rely on the global appeal of its iconic brands. This is far from a concrete strategy, yet it actually makes sense in a way. If international sales declined only 2% on a year-over-year basis, then it's clear that the company's potential lies outside of U.S. borders ... at least for the near future.

Abercrombie & Fitch plans on opening its flagship store in Shanghai next spring, and it recently opened five international Hollister stores and its first store in Japan. It also opened Abercrombie & Fitch/Abercrombie Kids and Hollister outlets in Italy.

The company will open 20 international Hollister stores by the end of this fiscal year, while closing 40-50 stores in the United States. The latter will be done via natural lease expiration.

Closing 40-50 U.S. stores makes sense based on current trends. Many retailers are now only keeping their top 150-200 physical retail locations open while focusing the remainder of their business online, which lowers costs. However, only well-established brands are capable of this. Otherwise, a retailer will find it difficult to improve brand recognition with just online and mobile exposure.

Abercrombie & Fitch is a well-established brand, as is Hollister, which actually has more physical locations than Abercrombie & Fitch (475 vs. 265). The problem for Abercrombie & Fitch is that walking into its stores is part of its appeal.

Fortunately, it's possible for Abercrombie & Fitch to make the online and mobile shopping experience just as exciting. There are no laws against playing high-energy music while showing off half-naked models on a company website. If anything, it would be unique, daring, and attract attention. And the company would have a good head start considering direct-to-consumer sales jumped 10% to $174.6 million in the third quarter.

That said, consolidated comps dropped 14%, with Abercrombie & Fitch comps sliding 13%, Abercrombie Kids declining 4%, and Hollister plunging 16%. Something must be done, and Engaged Capital thought it had the answer.

There's the door ... but it's closed

After sub-par top-line performance, seven consecutive quarters of comps declines, and a public relations nightmare, Engaged Capital (owns less than 1% of the retailer) had demanded that Mike Jeffries be shown the door.

In a nine-page letter, Engaged Capital cited public relations problems, mismanagement, and under-performance as reasons for this move, which could have come in February when Jeffries' contract was set to expire. If the wasn't made, then Engaged Capital wanted the company to be sold.

These weren't surprising requests from a large shareholder, as either event would have likely led to significant upside moves in the stock price. However, the board has resigned Jeffries with details undisclosed. Needless to say, Engaged Capital isn't pleased.

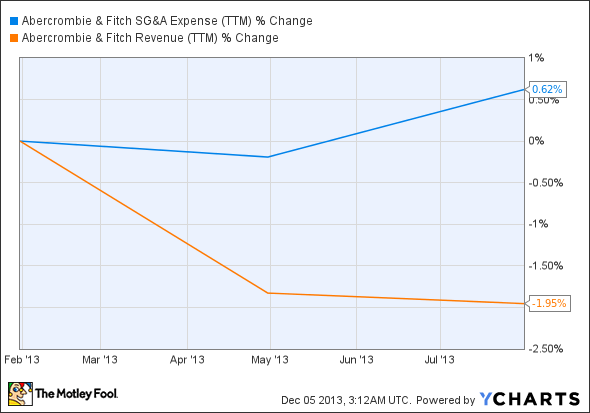

While this would have led to short-term stock appreciation, would it really have fixed the underlying business? Promotions are the name of the game. Consider the following chart, which compares top-line performance and SG&A expense performance over the past year:

Abercrombie SG&A expense (trailing-12 months) data by YCharts

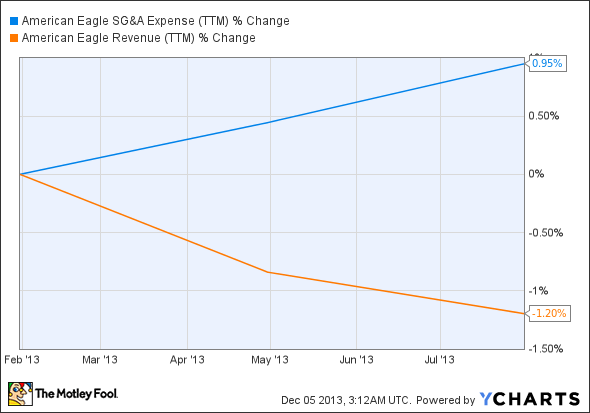

Not good. However, industry trends are more powerful than specific company initiatives. Look at the same chart for American Eagle:

American Eagle SG&A expense (trailing-12 months) data by YCharts

And for Aeropostale:

Aeropostale SG&A expense (trailing-12 months) data by YCharts

While Jeffries has had some missteps, and while I have been bearish on the company for a long time, this seems to be more of an industrywide dilemma.

Identity crisis

Jeffries stays in for now, but there is no established and effective long-term game plan. International growth offers potential, but it's going to take more than that. The bottom line is that teen retailers are in a tailspin right now. If you stand in front of an oncoming train and manage to jump out of the way before it hits you, then you might experience the greatest adrenaline rush of your life, but is it really worth the risk?

Owning these three stocks and throwing away the key may be highly profitable

As every savvy investor knows, Warren Buffett didn't make billions by betting on half-baked stocks. He isolated his best few ideas, bet big, and rode them to riches, hardly ever selling. You deserve the same. That's why our CEO, legendary investor Tom Gardner, has permitted us to reveal The Motley Fool's 3 Stocks to Own Forever. These picks are free today! Just click here now to uncover the three companies we love.

The article Abercrombie & Fitch: Status Update originally appeared on Fool.com.

Dan Moskowitz has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.