Dillard's: A Stable and Fundamentally Strong Pick for Your Portfolio

Share repurchases are a tried and tested way of increasing earnings by reducing the share count. Dillard's has been aggressively and consistently using this method while competing with the likes of Macy's and Kohl's . Along the way, Dillard's has managed to effectively navigate the negativity persisting in the retail sector and this company stands out from the crowd.

Dillard's share price has been going up ever since it started buying back shares as shown below. Through buybacks, Dillard's has returned cash to its shareholders and also increased its earnings which has led to optimism on the Street. Looking forward, it looks like Dillard's shares might continue to rise.

DDS Shares Outstanding data by YCharts

Strong results

Dillard's recently announced estimate-beating third-quarter results. Its comparable store sales, or comps, grew 1% compared to the same quarter a year ago. Dillard's saw similar growth in its construction business and as a result, consolidated revenue increased marginally by 1.4% versus last year to $1.51 billion.

As a result of positive comps combined with cost-cutting measures and increased share buybacks, Dillard's earnings per share grew 17.6% versus the year-ago period to $1.13, which beat the consensus estimate by $0.13 per share. This was the third consecutive quarter with an earnings beat.

Going forward, Dillard's strong performance is expected to sustain and analysts are bullish on the company. They estimate that it will earn more than $8 per share in 2015, up 10% from the 2014 estimate.

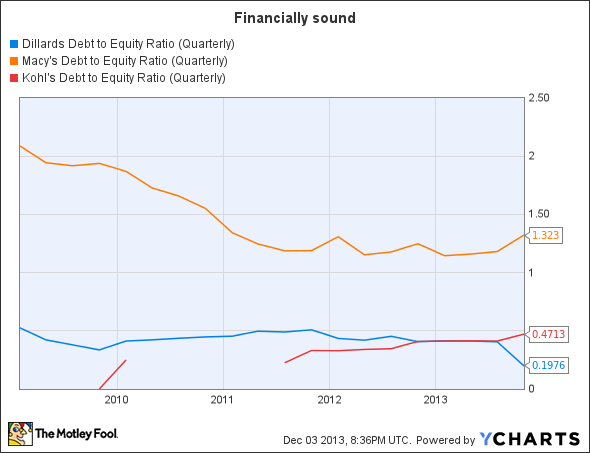

Financially sound

Another thing in Dillard's favor is its debt-to-equity ratio, which is the lowest in the history of the company and also the lowest among the three companies discussed here. This is why Dillard's is less vulnerable to risks such as rising interest rates or a change in its credit rating. This comes despite its aggressive and continued share repurchases that we discussed earlier. In addition, the company anticipates that it will have no short-term borrowings at fiscal year-end 2013.

DDS Debt to Equity Ratio (Quarterly) data by YCharts

In comparison, Macy's debt to equity ratio is almost 7 times that of Dillard's and Kohl's ratio is almost 2.5 times that of Dillard's as shown in the chart above.

Macy's and Kohl's: How the competition is performing

Macy's has performed pretty well. It reported a third-quarter revenue increase of 3.5% to $6.28 billion and a 31% gain in earnings per share versus the same quarter in the prior year. This brought in an element of relief for investors after the tepid second-quarter figures. This growth was on the back of broad-based strengthening across all major categories of business for Macy's and management said there were very few weak areas.

Macy's reiterated its guidance for the fall season, expecting comps growth of 2.5%-4% for the back half of the year and annual earnings per share in the range of $3.80-$3.90. Macy's is confident of a good holiday season ahead.

Kohl's, on the other hand, didn't perform well as it missed consensus estimates. It reported a comps decline of 1.6%, accompanied by a revenue decline of 1% for the third quarter to $4.44 billion.

Kohl's missed the consensus estimate on earnings as well and its adjusted earnings came in at $0.81 per share, declining 11% versus the same quarter a year ago. Earnings were lower due to lower sales and gross margins, which contracted 60 basis points due to lower revenue.

Going forward, Kohl's expects sales to decline in the range of 2%-4% and comparable-store sales to dip in the range of 0%-2% in the fourth quarter, which aren't good signs for investors.

Takeaway

Hence, investors should avoid Kohl's as it is declining. However, both Macy's and Dillard's look like good bets and both have their own attractive points. Macy's is set to perform well in the holiday quarter and the company also has a good dividend yield of 2%.

In comparison, Dillard's looks strong financially when stacked against Macy's and Kohl's. In addition, Dillard's has been aggressively buying back shares and it is the cheapest of the three with a P/E ratio of 11.6. Dillard's earnings have been growing well and more earnings growth is expected. Keeping all of these factors in mind, Dillard's looks like a good pick for conservative investors.

The Fool's top pick for 2014

The market stormed out to huge gains across 2013, leaving investors on the sidelines burned. However, opportunistic investors can still find huge winners. The Motley Fool's chief investment officer has just hand-picked one such opportunity in our new report: "The Motley Fool's Top Stock for 2014." To find out which stock it is and read our in-depth report, simply click here. It's free!

The article Dillard's: A Stable and Fundamentally Strong Pick for Your Portfolio originally appeared on Fool.com.

Fool contributor Prabhat Sandheliya has no position in any stocks mentioned. The Motley Fool owns shares of Dillard's. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.