Does This Solar Stock Have a Silver Lining?

For the average investor, silver is something that jingles in one's pocket or maybe in one's portfolio. It's not something that jingles with the solar industry. It turns out, though, that silver is an essential ingredient in the production of most solar panels.

One company that is especially focused on silver at the moment is Hanwha SolarOne , which recently announced that its innovative "Project EStarII" has now fully been integrated into its production processes. According to the company's press release, the new technology will enable Hanwha to "reduce silver paste consumption and optimize production processes to enhance efficiency and cost saving." Specifically, the new technology will result in average module power gains of 3W to 5W while resulting in an approximate 45% reduction in silver paste consumption.

Hi-ho silver!

Does the solar industry really rely on silver that much? According to The Silver Institute, a nonprofit international association, the most common type of photovoltaic cell (PV) is crystalline silicon. Of these cells, 90% use silver paste and "and over 100 million ounces of silver are projected for use by solar energy in 2015." Over 2,800 tons -- that's a lot of silver.

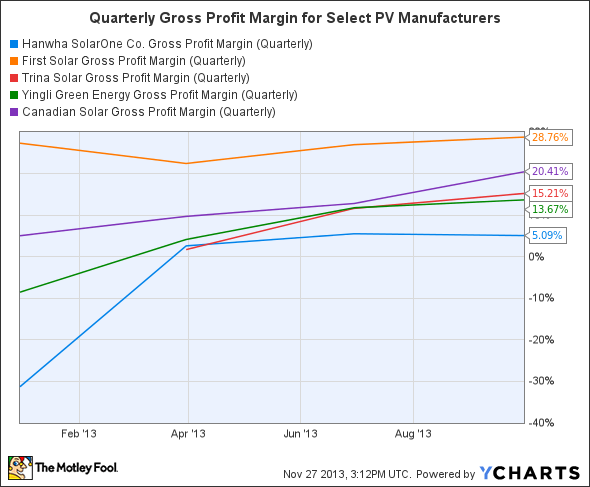

How important to Hanwha SolarOne is the addition of EStarII to its production processes? Well, it seems logical that a reduction in the amount of silver needed to produce the cells will help to improve the company's gross margins. For the third quarter, Hanwha SolarOne's gross profit margins dropped to 5.1% from 5.5% in the previous quarter. During the earnings call, though, management noted that gross margins should expand in the fourth quarter based on "higher shipment volumes, better pricing and reduced costs." This is especially important for the company as it has one of the worst gross profit margins among its peers.

HSOL Gross Profit Margin (Quarterly) data by YCharts.

This copper's a lot more than just some pennies

Some companies are not just looking to reduce the amount of silver in their modules; they're looking to eliminate it altogether. This is the case with TetraSun, a start-up PV manufacturer that uses copper instead of silver in its modules.

Having worked closely with the National Renewable Energy Laboratory (NREL), TetraSun was able to develop a "potentially disruptive technology" according to NREL Principal Scientist Mowafak Al-Jassim. This was undoubtedly the reason behind First Solar's acquisition of TetraSun in April -- an acquisition that affords First Solar the opportunity to enter the rapidly growing residential market. Regarding the acquisition, Jim Hughers, First Solar's CEO, said, ""This breakthrough technology will unlock the half of the PV market that favors high-efficiency solutions, which has been unserved by First Solar to date."

Having been absent from the residential market, First Solar has achieved impressive growth solely by operating in the utility-scale market. On the top line for the most recent quarter, First Solar saw $1.27 billion in net sales. This is a 143% increase quarter over quarter, and it's a 51% rise year over year. On the bottom line, the company saw net income grow to $195 million -- up from $161.4 quarter over quarter and $107.1 million year over year.

Is this the silver bullet?

SunPower is also exploring a silver-free solution. It has made a significant investment in the advanced silicon solar cell company Solexel. Although it's unclear just how much it has invested in the start-up, it's probably fairly substantial. After all, Doug Rose, SunPower's Vice President for Technology and Strategy, sits on the Board of Directors for Solexel.

The company's thin film solar cell dispenses with the need for expensive silver and relies on inexpensive aluminum instead. The high-efficiency cells Solexel produces would be most applicable to the residential market, something which seems to please SunPower's management. During the previous earnings call, management noted that "year-over-year, our residential revenue has more than doubled while bookings have increased by 60%."

Get back

Not all companies may be looking to eliminate silver from their systems altogether, though. At least this is what 3M is hoping. Back in November, it debuted a product which offers a copper alternative to the silver used in the back of PV modules. According to 3M, its Backside Busbar Tape 4706 offers substantial cost savings and protection from the volatility of silver prices. The tape also provides a 0.2% increase in efficiency for the solar cells.

This latest offering is just one of many products 3M offers to the solar industry. Many of its offerings address crystalline silicon and thin film solar panels as well as concentrated solar power solutions. As the solar industry grows, 3M may prove to benefit nicely as it seems to have a good sense of what needs exist.

The Foolish takeaway

The solar industry shows no signs of slowing down. As it grows, however, some companies will fail to keep up and fall by the wayside. I'm on the fence about Hanwha SolarOne's prospects. I find some aspects of the company intriguing, but I have some major reservations as well. Its margins are definitely part of that.

SunPower and First Solar, on the other hand, continues to impress. I also find their commitment to seeking ways to further disrupt the industry compelling. Who knows? In the end, it may be companies like 3M that provide goods and services to the industry that are the ultimate winners.

The Motley Fool's Top Stock for 2014

The market stormed out to huge gains across 2013, leaving investors on the sidelines burned. However, opportunistic investors can still find huge winners. The Motley Fool's chief investment officer has just hand-picked one such opportunity in our new report: "The Motley Fool's Top Stock for 2014." To find out which stock it is and read our in-depth report, simply click here. It's free!

The article Does This Solar Stock Have a Silver Lining? originally appeared on Fool.com.

Scott Levine has no position in any stocks mentioned. The Motley Fool recommends 3M. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.