These Investments Aren't for the Risk Averse

So ... you want to invest in theme parks? With Cedar Fair , Six Flags Entertainment and SeaWorld Entertainment appreciating 7.85%, 7.21%, and 3.70% respectively over the past month, who can blame you?

While momentum might be your friend at the moment, when you invest in companies that rely heavily on discretionary income, momentum can quickly become your enemy. This doesn't mean you should avoid theme park companies as investments. Owning one of them as a small percentage of a diversified portfolio isn't necessarily a bad idea. The trick is figuring out which one of the aforementioned companies offers the most long-term potential.

Cedar Fair: Recent results

Cedar Fair's third quarter net revenue increased 7% to $492.1 million year over year, thanks to strength in attendance, guest spending, and out-of-park revenue. Park attendance on a comps basis improved 2%. This is the most important reading for theme parks because it indicates the company's ability to drive repeat visitation. While this is "just" a 2% increase, that's a healthy number for the industry. Cedar Fair also increased its quarterly cash distribution 12%, indicating that Cedar Fair is confident in its future ability to generate free cash flow.

Looking ahead, Cedar Fair expects full-year net revenue of $1.125 billion-$1.135 billion, and to come in on the high end of its adjusted EBITDA range of $451 million-$425 million. This will represent a 6%-9% increase over last year. This strong outlook is primarily due to strategic capital investments and a successful business model. Cedar Fair also points to its "Best Day of Summer" approach. This pertains to employees being trained to make each guest's experience so memorable that it will represent the best day of their summer. Based on the numbers, this strategy has been effective, as guests are returning to Cedar Fair parks and spending more time in those parks.

If you look at a bigger picture, such as year-to-date through Nov. 3, the numbers are still impressive, with net revenue jumping 6% year over year. For the same time frame, average in-park guest spending increased to $44.33 (a record). Out-of-park revenue grew 7%. Excluding two water parks, sales and attendance increased 2% on a comps basis. Attendance at all parks through Nov. 3 totaled 22.7 million visitors (another record).

More fun ahead

Cedar Fair constantly looks to innovate in order to stay ahead of its competition and drive its top line. It would also like to remain the "Best Amusement Park in the World," an award it has received from Amusement Today.

In 2014, Cedar Fair will add many new attractions to its parks, two of which are listed below:

Banshee: longest inverted coaster in the world (King's Island)

Guardian of Wonder Mountain: coaster track with interactive digital gaming system (Canada's Wonderland)

Cedar Fair will also revitalize Camp Snoopy and the Calico Mine Ride at its popular Knott's Berry Farm, and add cottages, cabins, and in-park TVs at some parks.

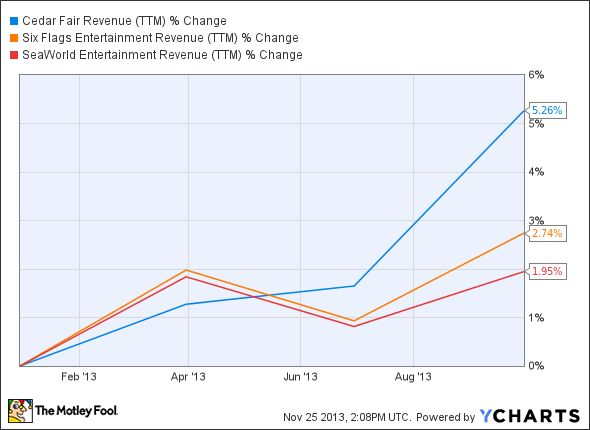

Based on attendance, as well as in-park and out-of-park spending, take a look at how Cedar Fair has performed on the top line compared to its peers over the past year:

FUN Revenue (TTM) data by YCharts

Poor track record

Don't get the wrong idea here--Six Flags has a lot of potential. At the same time, I can't advocate an investment in a company that has recently gone bankrupt and been responsible for an accidental death. As expected, the latter incident led to suppressed attendance, revenue, and profit. The good news is that these numbers are still up overall.

In the third quarter, revenue increased 4% to $505 million year over year. Total guest spending per capita increased 2% to $41.27, admission revenue per capita improved 2% to $23.96, in-park revenue per capita improved 2% to $17.31, and attendance improved 2% to 11.8 million.

Over the first nine months of the year, attendance increased 2% to 22.4 million. Six Flags has managed to upsell guests season passes and membership plans well, leading to a deferred revenue improvement of 28% to $76 million.

However, its growth still hasn't been as impressive as Cedar Fair's. Also consider that Six Flags trades at 28 times forward earnings, whereas Cedar Fair trades at 15 times forward earnings. As if that's not enough to differentiate the two companies from an investment perspective, Cedar Fair yields 5.9% while Six Flags yields 5%.

Both companies are highly leveraged. Cedar Fair carries $1.56 billion in long-term debt. Its cash position is $183.48 million, and it generated $326.14 million in operating cash flow over the past twelve months. Six Flags carries $1.40 billion in long-term debt. Its cash position is $200.96 million, and it generated $345.88 million in operating cash flow over the past year. Therefore, it's going to be difficult for these companies to reinvest in their businesses while maintaining their dividend yields over the long haul, especially when interest rates eventually increase.

To the dry seas

SeaWorld's revenue increased 3% to $538.4 million in the third quarter. Net income blossomed 30% to $120.2 million, and adjusted EBITDA grew at a 10% clip to $254.4 million. These improvements were primarily due to strength at SeaWorld-branded parks, pricing power, and effective cost management.

SeaWorld is currently on pace for a third consecutive record-setting year on its top and bottom lines while also generating a healthy free cash flow. That said, SeaWorld isn't growing as fast as its peers, it's trading at 22 times forward earnings -- a premium compared to fastest-growing Cedar Fair -- and it "only" yields 2.60%. The irony here is that SeaWorld seems to be more responsible with its dividend yield given its highly leveraged position, carrying $1.64 billion in long-term debt. It has $210.52 million in cash, and it generated $277.18 million in operating cash flow over the past months.

The bottom line

Investing in highly leveraged companies that rely on discretionary income isn't the best path to prosperity. You can do better elsewhere. If you choose to add one of these companies to your portfolio, Cedar Fair looks to offer the most long-term potential.

There's great growth potential in these six companies

Tired of watching your stocks creep up year after year at a glacial pace? Motley Fool co-founder David Gardner, founder of the No. 1 growth stock newsletter in the world, has developed a unique strategy for uncovering truly wealth-changing stock picks. And he wants to share it, along with a few of his favorite growth stock superstars, WITH YOU! It's a special 100% FREE report called "6 Picks for Ultimate Growth." So stop settling for index-hugging gains... and click HERE for instant access to a whole new game plan of stock picks to help power your portfolio.

The article These Investments Aren't for the Risk Averse originally appeared on Fool.com.

Dan Moskowitz has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.