Peabody's Coal Is Still Worth Your Time

Coal is not sexy, but the world still needs stable base load electricity generation. On the surface Peabody Energy's latest quarterly earnings look quite poor with a loss of $0.10 per share. The key is to separate the company's continued operations from its discontinued operations. Overall, it's in good position to grow.

Peabody's Q3 earnings

In Q3 2013, Peabody posted earnings from continued operations of $0.06 per share. Its discontinued operations posted losses of $0.16 per share, making for a total loss of $0.10 per share. Losses from discontinued operations should not be taken too seriously, however, as they are only temporary.

Peabody's discontinued operations

The company is selling its Wilkie Creek Mine in Australia. Thanks to the Australian Prime Minister's push to repeal the nation's carbon tax, now Peabody should have an easier time getting this mine off its books. The company also faced some impairment charges related to shutting down its Air Quality Mine in Indiana.

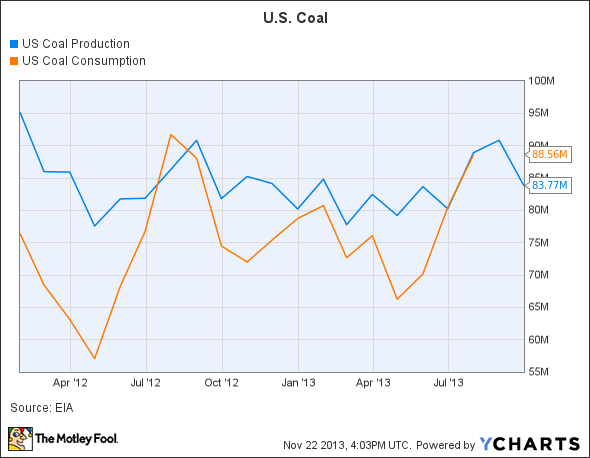

Don't give up on U.S. coal

US Coal Production data by YCharts

The above graph shows how America's coal supply is starting to fall in line with demand. In the first half of 2013 151 U.S. coal mines were idled, helping to limit pricing pressures.

Asian growth

Growth is the lifeblood of capitalism. Together China and India are expected to increase coal demand by 1 billion tonnes from 2012 to 2017, while the rest of the world is expected to raise demand by just 179 million tonnes in the same time period.

Peabody's recent quarter shows how the company is in a good position to serve these new markets. Year over year, it lowered its Q3 2013 Australian operating costs per ton by $6.17. Another positive sign for Peabody is the five-year $1.65 billion revolver and the seven-year $1.2 billion term loan it just acquired. The fact that Peabody is able to roll over its debt shows that its total debt-to-equity ratio of 1.34 is manageable.

Take a deeper look at China's energy policies

China is keen to decrease its greenhouse gas emissions and clean up its economy, but don't expect the country to simply stop using coal. The government's plan is to decrease coal's share of total energy use from 68.4% in 2011 to 65% in 2017. Considering China's high growth rate, the number of tonnes of coal consumed can grow even while it becomes a lower percentage of total energy use.

Still, not all miners are created equally

While Peabody has hope, Arch Coal is a different story. The company is laden with debt, and its total debt-to-equity ratio is already at 1.97. Also, unlike Peabody, Arch Coal has no mines in Australia. Instead, it has many mines in America's expensive Appalachian region. While Peabody's earnings before interest, taxes, deductions and amortization, or EBTIDA, grew from Q1 2013 to Q3 2013, Arch Coal's EBITDA fell in the same time frame.

Arch Coal has expensive American mines and too much debt to be buying assets overseas. With few growth prospects and falling profit, it is best to stay away from this company.

Alpha Natural Resources is a big metallurgical coal producer, but thermal coal still has a big impact on the firm's bottom line. In 2012 metallurgical coal was only 44% of its revenue. Alpha Natural Resources' advantage can be found in its ports on the East Coast, which give it strong export capacity, but its thermal operations in the Eastern U.S. expose it to strong margin pressures and falling customer demand.

Unlike Peabody, Alpha Natural Resources does not have significant resources in Australia. Its profit is constrained and analysts expect the company to post losses in 2013 and 2014. Alpha's low total debt-to-equity ratio of 0.77 means that the company has a low chance of going bankrupt, but still has significant losses ahead.

While Peabody decided to buy Asian assets to deal with the falling U.S. market, CONSOL Energy took a different path. It recently sold all five of its longwall coal mines in West Virginia for $3.5 billion, though it is retaining coal mines in other areas. With an estimated natural gas production growth rate of 30% in 2015 and 2016, CONSOL Energy is turning itself into a natural gas E&P. With its low total debt to equity ratio of 0.83, this firm is one of the best positioned coal and natural gas producers in the Eastern U.S.

The Foolish bottom line

Peabody's latest earnings show how the company is shooting for long-term profitability by selling off low-quality assets. CONSOL Energy has a similar strategy, though it is pushing its capital into natural gas. Alpha Natural Resources' and Arch Coal's recent losses are signs that both companies are stuck with high cost mines and a grim future.

Growth you can count on

This incredible tech stock is growing twice as fast as Google and Facebook, and more than three times as fast as Amazon.com and Apple. Watch our jaw-dropping investor alert video today to find out why The Motley Fool's chief technology officer is putting $117,238 of his own money on the table, and why he's so confident this will be a huge winner in 2013 and beyond. Just click here to watch!

The article Peabody's Coal Is Still Worth Your Time originally appeared on Fool.com.

Joshua Bondy has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.