Still Bullish on This Restaurant

Texas Roadhouse has rewarded its shareholders in a big way so far this year, with the stock appreciating 73.15% year to date. A 1.70% yield doesn't hurt, either. However, it's time to look forward to see if this kind of momentum is sustainable. It's possible that TheCheesecake Factory or Ruth's Chris Hospitality offer more potential. Let's take a look at Texas Roadhouse prior to getting to peer comparisons.

Past results and future potential

Texas Roadhouse saw revenue increase 8% in the third quarter, year over year. Comps, an indication of sales at restaurants open at least one year, improved 2.6% at company-owned restaurants and 4% at franchisee restaurants. Comps are important for restaurants because the reading negates results from new restaurant openings, which could misguide investors. Texas Roadhouse expects positive results for fiscal year 2013 and FY 2014. This indicates that demand remains high for Texas Roadhouse.

Diluted earnings per share declined 4.6%, which is likely to concern you. However, this decline was primarily due to food cost inflation. For FY 2013, Texas Roadhouse expects food cost inflation of 7%, up from the previous estimate of 6.5%-7%. On the other hand, Texas Roadhouse is confident that food costs will decline significantly in FY 2014, leading to food cost inflation in the low-single digits.

Another positive is that Texas Roadhouse has reported seeing strong demand at new restaurants. This indicates that management is good at selecting high-potential locations. Texas Roadhouse looks to expand its restaurant base internationally and domestically. In regards to the latter, it will continue to aim for mid-sized markets, which often see high demand thanks to population size, income levels, nearby shopping and entertainment, as well as a healthy employment base.

In order to drive repeat guest traffic, Texas Roadhouse will encourage repeat visits via top-quality foods and service. In order to drive new guest traffic, Texas Roadhouse will rely on localized marketing programs with a focus on service speed and comfortable seating.

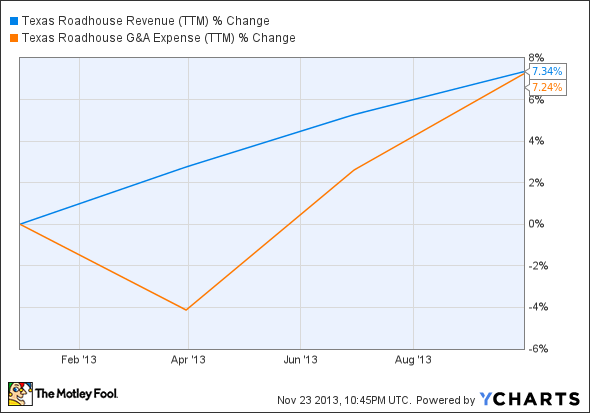

Texas Roadhouse will continue to invest in its infrastructure, with a long-term goal of revenue outpacing G&A expenses. Let's see how the company is doing in that regard over the past year:

TXRH Revenue (TTM) data by YCharts

Texas Roadhouse is reaching its goal, but not by much. More separation between the top line and G&A expenses should be achievable.

That was just the appetizer. Now let's take a look at the main course.

High-end dining

In case you haven't noticed, high-end restaurants have been performing well. The high-end consumer is benefiting from stock and real estate appreciation, which leads to increased discretionary income. Hopefully, these high-end consumers aren't spending as though the market will go up forever. However, that's a story for a later time, perhaps a much later time considering that Janet Yellen plans on keeping interest rates at record lows through 2017. However, as veteran investors have experienced on several occasions, nothing is guaranteed.

The point here is that low interest rates often lead to stock and real estate appreciation, which then leads to increased discretionary income for high-end consumers. This, in turn, leads to companies like Ruth's Hospitality Group performing well. Due to the current economic environment, investing in Ruth's will likely be profitable in the near future.

If you look at Ruth's third-quarter net income of $2.9 million -- much higher than $0.8 million in the year-ago quarter -- then your eyes might bulge at the screen in a way that would make John Doyle proud. You might want to temper that enthusiasm, as $1.3 million of this gain was due to a tax benefit related to insurance settlements. On the other hand, that's still an impressive move when you exclude non-recurring items.

Sales also impressed in the third quarter, increasing 4.3%. If you look at comps, Ruth's saw a 4.2% jump, thanks to strong traffic and an average menu price increase of 1.7%.

We'll get back to Ruth's in a moment. First it's time for dessert.

Similarities and differences

The Cheesecake Factory also saw a revenue improvement in its third quarter - $469.7 million versus $453.8 million in the year-ago quarter. As far as comps go, they grew at a 0.8% clip. If you break that number down, comps at the company's namesake brand increased 1%, and comps at Grand Lux Cafe slid 2.6%. This might seem like a big negative if you just read the numbers, but of the company's 178 full-service restaurants, 166 are The Cheesecake Factory restaurants. Therefore, you might want to disregard comps results for Grand Lux Cafe.

The Cheesecake Factory has now seen 15 consecutive quarters of comps growth, and it has reported seeing high demand at its new restaurants, which is a hint that the top line might perform well in the near future. Like Texas Roadhouse, The Cheesecake Factory is good at selecting high-potential site locations.

The Cheesecake Factory yields 1.20%, as does Ruth's. Texas Roadhouse offers the highest yield at 1.70%. More importantly, for the reasons given above, Texas Roadhouse has outperformed its peers on the top line over the past year:

TXRH Revenue (TTM) data by YCharts

The bottom line

As long as the broader market continues its advance, all three of these companies should see stock appreciation. With Ruth's targeting the high-end consumer, it's high risk/high reward. The same can be said for The Cheesecake Factory, but to a lesser extent. Texas Roadhouse isn't just the most resilient (relatively speaking), but it also offers the most top-line potential, based on its target consumer and highly strategic locations.

Invest in top-notch resilient companies

If you're looking for some long-term investing ideas, you're invited to check out The Motley Fool's brand-new special report, "The 3 Dow Stocks Dividend Investors Need." It's absolutely free, so simply click here now and get your copy today.

The article Still Bullish on This Restaurant originally appeared on Fool.com.

Dan Moskowitz has no position in any stocks mentioned. The Motley Fool recommends Texas Roadhouse. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.