TJX Continues to Impress, as Does Its "Little Brother"

TJX Companies continues to satisfy its investors, as it has seen stock appreciation just north of 51% year to date. We'll take a look at recent results, longer-term top-line and bottom-line performances, key metrics, past and future buybacks, as well as how the stock is likely to perform going forward. And while TJX has been a consistent winner, a company that's sometimes viewed as its little brother might present an even better investment option.

Recent results

Prior to getting to that mysterious "little brother" company, let's first take a look at recent results and future expectations for TJX. In the third quarter, net sales increased 9% to $7 billion year over year, and diluted earnings per share came in at $0.86 versus $0.62 in the year-ago quarter. Comps grew at a 5% clip.

If you look at the past nine months, the numbers are still impressive. On a year-over-year basis, net sales jumped 8% to $19.6 billion, with comps improving 3%. Diluted EPS came in at $2.14 versus $1.73 in the year-ago period.

TJX is confident that its strong momentum will continue. This makes sense since TJX is an off-price retailer offering 40%-60% (and sometimes more) off department store prices. In the current economic environment, the vast majority of consumers are looking for a bargain. If consumers can find fashionable apparel or home goods products at steep discounts, they're going to take advantage of those opportunities.

In essence, TJX is a perfect fit for the current consumer mind-set. Better yet, while most luxury retailers are performing well because many high-end consumers are benefiting from stock and real estate price appreciation, many of those luxury retailers aren't likely to perform as well if markets reverse. T.J. Maxx, Marshalls, and Home Goods, among other TJX brands, will still have their doors open, awaiting customers who desire steep discounts. In other words, stock and real estate market moves are much less likely to affect TJX than many other retailers.

TJX recently stated that it's capable of succeeding in any economic retail environment, and that it's very confident about its top-line and bottom-line growth potential moving forward. The company added that the fourth quarter is off to a good start, and that fresh products will be arriving in its stores for the holidays.

As if that's not enough optimism, TJX announced that it plans to repurchase $1.3 billion-$1.4 billion worth of its stock in fiscal year 2014. Furthermore, TJX raised its FY 2014 EPS outlook to $2.91-$2.94. FY 2013 EPS came in at $2.55.

You might be wondering how it's even remotely possible that another off-price retailer has as much potential as TJX. Believe it or not, that company exists.

Big brother vs. little brother

If you follow the NFL, then you know that Peyton Manning receives much more recognition and accolades than his little brother, Eli Manning. While Peyton might deserve this respect, Eli Manning has quietly led his team to two Super Bowl victories. The comparison below is similar.

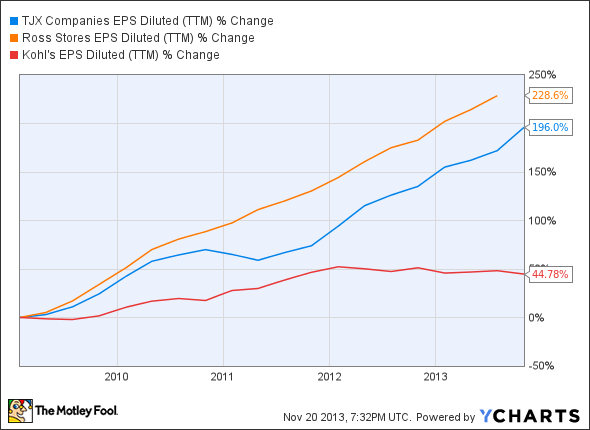

There is no question that TJX has been very impressive on the top line. As a matter of fact, it has greatly outperformed Kohl's on the top line over the past five years. This fact might not blow you away, but Kohl's has managed to deliver on the top line in a very challenging economic environment. Therefore, if TJX has greatly outperformed Kohl's, it's clearly a top-notch retailer. Now consider that Ross Stores has been even more consistent on the top line during the same time frame:

TJX Revenue (TTM) data by YCharts

The same can be said for the bottom line:

TJX EPS Diluted (TTM) data by YCharts

Getting back to the top line performances for TJX and Ross Stores, they took place while both companies managed to maintain positive balance sheets -- very rare in today's economic environment. TJX has $2.09 billion in cash and short-term equivalents versus $1.27 billion in long-term debt. Ross Stores has $550.58 million in cash and short-term equivalents versus $150 million in long-term debt. Kohl's, on the other hand, is slightly leveraged, with $598 million in cash and short-term equivalents versus $4.88 billion in long-term debt.

All three companies are good at generating cash flow. Over the past 12 months, TJX has an operating cash flow of $2.55 billion, and Ross Stores and Kohl's have operating cash flow of $1.01 billion and $1.58 billion, respectively. Kohl's offers the highest yield at 2.60%. TJX yields 0.90%, while Ross Stores yields 0.80%.

If you look at total shareholder return over the past five years, which combines dividend payments and stock appreciation, it couldn't be much closer between TJX and Ross Stores:

ROST Total Return Price data by YCharts

The bottom line

While Kohl's isn't a bad investment option -- I often look at it as the epitome of average -- TJX and Ross Stores are tearing the cover off the ball. These companies are well-positioned for what the consumer desires in today's world. This should lead to continued success for both TJX and Ross Stores.

The Motley Fool's top investment for 2014

The market stormed out to huge gains across 2013, leaving investors on the sidelines burned. However, opportunistic investors can still find huge winners. The Motley Fool's chief investment officer has just hand-picked one such opportunity in our new report: "The Motley Fool's Top Stock for 2014." To find out which stock it is and read our in-depth report, simply click here. It's free!

The article TJX Continues to Impress, as Does Its "Little Brother" originally appeared on Fool.com.

Dan Moskowitz has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.