2 Companies Poised to Profit From Bank of America's Woes

Banks are complex. Really complex.

There are, of course, the derivatives portfolios that approximately zero people in the world truly understand. And there is the systemic interconnectedness between the world's banks that again, more or less zero people truly understand. But both these examples are very high level. The actual day-to-day business of running a modern bank is, believe it or not, nearly as complex.

Source: MoneyBlogNewz.

Banks large are small are turning to software to manage this complexity. Bank of America has been working over the past two years to develop an integrated and streamlined workflow solution to ease the pain of doing business. The bank's goal is to avoid future scandals like the Robo-Signing Foreclosures and accusations of intentionally misleading borrowers who qualified for mortgage modifications.

You can read the full scope of Bank of America's problems here, in a very well-written and comprehensive report by fellow Fools John Maxfield, John Reeves, and Ilan Moscovitz.

Here is the problem

Let's start with a simple example -- originating a mortgage loan. A customer walks into the bank and requests a loan. The banker in the branch must communicate the products available, the current rates, and the general process to get to a loan closing. The banker also must provide the borrower with a litany of disclosures, all required by law. The borrower must submit a personal financial statement and proof of income and must sign a form allowing the bank to pull the individual's credit report.

From there. the bank must assess the creditworthiness of the borrower. It must obtain an appraisal and then review it, approve it, and ensure that the loan-to-value is within bank policy and regulatory guidelines.

Once all this work is done, generally two to three weeks into the process, the bank must roll out a whole other set of disclosures, required by an alphabet soup of regulations, laws, and government agencies -- there's the HUD, RESPA, ECOA, HMDA, Fair Credit Reporting Act Disclosure, and on and on and on.

Eventually, maybe, the loan documents go out to an attorney to close the loan. Loan documents vary by state, creating a new set of complexity for banks that operate across state lines. Only then, if the bank and borrower are lucky, can that mortgage loan finally close.

Fools, my brain hurts just writing out this admittedly abbreviated summary. The requirements and disclosures to open even a simple checking account are only moderately easier. On the deposit side, branch personnel must create "Suspicious Activity Reports," "Currency Transaction Reports," and other government required data collection for only certain transactions. Here is an excerpt from the rules governing Currency Transaction Reports -- it's only one page but will make your head spin.

And lest we forget, there are also reams of rules and regulations for the foreclosure, short sale, and bankruptcy processes, for enterprise risk management practices, for fraud monitoring and reporting, and for essentially every other function of the bank -- loans, deposits, wealth management, trading, and, well, you get the picture.

Have I mentioned that the banks must also document all of their activities just in case the Federal Reserve wants to check for any unfair, deceptive, or abusive acts or practices? (That's UDAAP, for short -- you can enjoy some of the bureaucracy here.)

Fools, these requirements apply to every bank, from the smallest one-office community bank to Bank of America. It's a major challenge for these institutions every single day. For the savvy investor, where there is a challenge there is also an opportunity.

Here is the solution

Simply stated, the only ways banks will be able to manage the overwhelming complexity of opening the doors every morning is through automation. When a customer applies for a loan, the computer, via specially designed software, can automatically print, save, and store all the required disclosures. The customer has the information he or she needs, the bank has a record on file, and the regulators have the checks and balances needed for appropriate regulation.

Jack Henry and Associates and Pegasystems are two of the leading specialty software companies providing this technology to banks. Through an aggressive combination of acquisitions and organic growth, the entire banking software industry, led by these two companies, has performed remarkably well over the past five years.

When crises occur, smart banks focus inward. These banks batten down the hatches and optimize what they are doing. It could mean a managed downsizing of the company, it could mean an increase in employee training, or it could mean re-engineering internal processes. It could also mean upgrading technology.

Driven by this fact, revenue growth for both Jack Henry and Pegasystems has been outstanding since the recession. In the following chart, you'll note the spike in revenue growth immediately following the financial crisis in 2010. And that growth, while somewhat abated, remains strong.

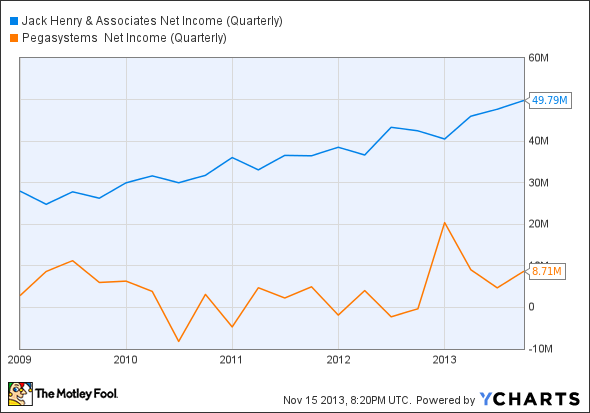

And best of all, that revenue growth is translating into growth on the bottom line. In this final chart, you'll note the trend from the bottom left to the upper right, a trend that should bring a smile to any investor's face (particularly so for Jack Henry).

The next five years

The recession launched this boom for these software businesses, but another dynamic in banking will sustain it: new regulations.

The full extent of the Dodd-Frank regulations remains murky. Banks are beginning to see changes rolling out, perhaps most notably the new "qualified mortgage" rule under the Truth in Lending Act.

Over the next five years, regulations will continue to change and also to expand. The only way for banks to contend with these changes, in terms of both compliance and cost, is through software.

For Jack Henry and Pegasystems, new bank regulations makes their products even more indispensable.

Three more stocks poised for the future

As every savvy investor knows, Warren Buffett didn't make billions by betting on half-baked stocks. He isolated his best few ideas, bet big, and rode them to riches, hardly ever selling. You deserve the same. That's why our CEO, legendary investor Tom Gardner, has permitted us to reveal The Motley Fool's 3 Stocks to Own Forever. These picks are free today! Just click here now to uncover the three companies we love.

The article 2 Companies Poised to Profit From Bank of America's Woes originally appeared on Fool.com.

Fool contributor Jay Jenkins has no position in any stocks mentioned. The Motley Fool recommends Bank of America and Pegasystems and owns shares of Bank of America. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.