Why Did This Genetic Test Maker Outperform Its Industry Peers?

Shares of Affymetrix have jumped nearly 20% since the end of October, after the genetic test maker reported third-quarter earnings, which marked an ongoing return to profitability.

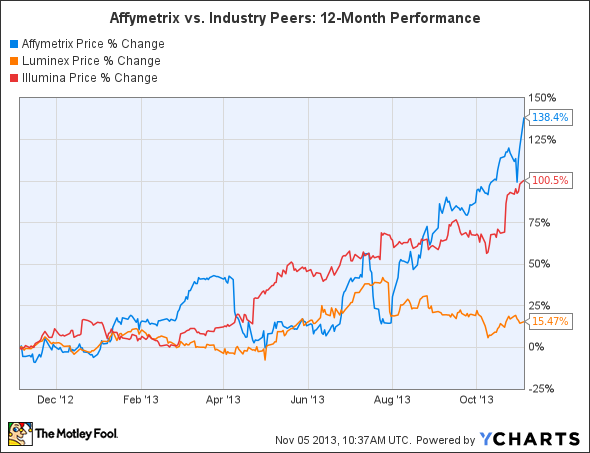

Affymetrix has been one of the top-performing genetic analysis companies over the past year, handily outperforming its industry peers Luminex , and Illumina .

Source: YCharts.

Affymetrix is the smallest of these companies and might have the most room to grow, but was its rally over the past year justified?

Slow and steady third-quarter growth

Affymetrix reported adjusted earnings per share of $0.05, a considerable improvement from the adjusted loss of $0.03 per share it reported in the prior year quarter. Total revenue inched up 0.9% year over year to $80.4 million, while revenue from product sales climbed 2.9% to $74.8 million.

The company's core business is built upon its GeneChip system and associated microarray technology, which is used to acquire, analyze, and manage genetic information. It sells these tools to customers in the life sciences, and clinical health care markets.

Affymetrix's genetic analysis business, which accounts for 68% of its top line, was supported by strong sales of its CytoScan and Axiom genotyping products, which respectively climbed 36% and 80% year over year. Those gains, however, were offset by ongoing losses in its legacy Expression business, which reported a 12% decline.

Revenue growth compared to industry peers

Affymetrix can be compared directly to two larger industry peers, Illumina and Luminex, which both report the majority of their revenue in two of the same categories as Affymetrix -- consumable (one-time use) research items, and genetic testing instruments.

However, when stacked up against these rivals, Affymetrix's growth looks lackluster -- especially in comparison to Illumina, which is posting much stronger revenue growth despite being a much larger company.

Company | Market Cap | Consumable Items | Growth (YOY) | Instruments | Growth (YOY) |

Affymetrix | $565 million | $52.1 million | 3% | $2.8 million | (39%) |

Luminex | $802 million | $12.8 million | (0.5%) | $16.1 million | (2%) |

Illumina | $12.1 billion | $215.4 million | 17% | $94.8 million | 31% |

Sources: Company earnings reports from the most recent quarter.

All three companies can be compared to their larger rival Life Technologies , which has a market cap of $13 billion. Thermo Fisher Scientific agreed to acquire Life Technologies back in April for $13.6 billion, with the deal scheduled to close in early 2014.

Life Technologies reports sales of its consumable items and genetic analysis tools together in its Genetic Analysis business segment, which declined 12.5% year over year to $340.6 million last quarter. The Genetic Analysis segment accounts for 36% of Life Technologies' total revenue.

In addition to its consumable and instrument segments, Affymetrix generates revenue from the eBioscience unit, which it acquired in 2011 for $330 million in cash. Revenue at the unit, which specializes in flow cytometry and immunoassay reagents, climbed 13.1% year over year to $19.9 million.

Wobbly fundamentals

A comparison of these four companies shows that Affymetrix's fundamentals don't compare favorably to its peers.

Company | Forward P/E | 5-Year PEG | Price to Sales (TTM) | Debt to Equity | Profit Margin |

Affymetrix | 52.60 | 2.01 | 1.62 | 65.51 | (11.79%) |

Luminex | 30.28 | 1.68 | 3.73 | 0.67 | 3.34% |

Illumina | 47.00 | 2.98 | 8.94 | 62.53 | 8.68% |

Advantage | Luminex | Luminex | Affymetrix | Luminex | Illumina |

Source: Yahoo! Finance as of Nov. 5. TTM = trailing 12 months.

Affymetrix's high forward P/E and 5-year PEG ratio of 2.01 indicates that the stock could be overvalued at current prices and might face sluggish growth ahead. Its high debt to equity ratio and negative profit margin are also red flags, which point to future problems with bottom line growth.

Reduced expenses and rising cash

It's tough to recommend Affymetrix on the basis of its fundamentals, but the company has made admirable improvements in reducing expenses and boosting its cash position.

During the quarter, it sharply reduced its expenses -- sales, general, and adminstrative expenses fell 7.2% while research & development expenses declined 30.3%. GAAP-adjusted operating expenses declined 14.6%. This reduction of expenses boosted its gross margin from 52% to 55%.

Affymetrix also divested its Anatrace product line of specialty detergent and synthetic lipids to StoneCalibre. As a result, the company finished the third quarter with $50.2 million in cash -- nearly double the $25.7 million that it held in the prior-year quarter.

The Foolish bottom line

Although Affymetrix is showing signs of a turnaround, its slow growth could be a problem, since it relies heavily on increased spending from academic institutions, which could face budget cuts due to macroeconomic problems. In addition, reduced R&D expenses could lead to a stagnation in Affymetrix's product line -- a dangerous vulnerability in a market that constantly demands the latest and most accurate technologies.

For now, conservative investors should stay away from Affymetrix, as its price growth seems to be fueled purely by market momentum rather than real fundamental growth.

More biotech stock ideas

The best way to play the biotech space is to find companies that shun the status quo and instead discover revolutionary, groundbreaking technologies. In the Motley Fool's brand-new FREE report "2 Game-Changing Biotechs Revolutionizing the Way We Treat Cancer," find out about a new technology that big pharma is endorsing through partnerships, and the two companies that are set to profit from this emerging drug class. Click here to get your copy today.

The article Why Did This Genetic Test Maker Outperform Its Industry Peers? originally appeared on Fool.com.

Leo Sun has no position in any stocks mentioned. The Motley Fool recommends Illumina. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.