A Healthy Outlook for Vitamin Shoppe

Within the fragmented nutritional supplement market, Vitamin Shoppe (NYSE: VSI) seeks to gain market share through acquisition and the opening of new stores. While the combination of increasing demand for supplements and a competitive environment full of smaller competitors has generated excitement over the growth opportunity for Vitamin Shoppe, competition from a range of larger companies ranging from Amazon.com (NASDAQ: AMZN), GNC Holdings (NYSE: GNC), and pharmacies such as Walgreens (NYSE: WAG) have forced shares of Vitamin Shoppe downward in recent months. The downward trend changed on Tuesday following Vitamin Shoppe's release of its quarterly earnings. Does this mean that the storm has passed?

Vitamin Shoppe reports solid revenue growth

Shares of Vitamin Shoppe surged as much as 18.5% following the release of its third quarter earnings. This spike in share price is due largely to performance on the top line; management reported a 14% increase in revenue thanks to a balanced mix of new store openings, the integration of the company's Super Supplements acquisition earlier in 2013, and a 2.6% increase in same store sales (SSS).

In addition to third quarter results, management's comments regarding investments in a new distribution center, omni-channel platforms, private label development, and international expansion have investors excited that the growth story for Vitamin Shoppe is far from over. Looking ahead to 2014, Vitamin Shoppe expects to open 60 new stores and generate "mid single digit" SSS growth.

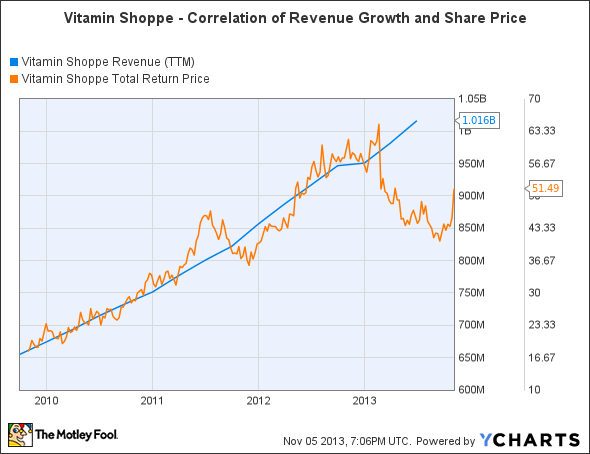

Renewed confidence in long-term revenue growth for Vitamin Shoppe has a powerful effect on the share price; until recently, growth in revenue and share price have been highly correlated as illustrated below:

VSI Revenue (TTM) data by YCharts

Vitamin Shoppe generates strong earnings

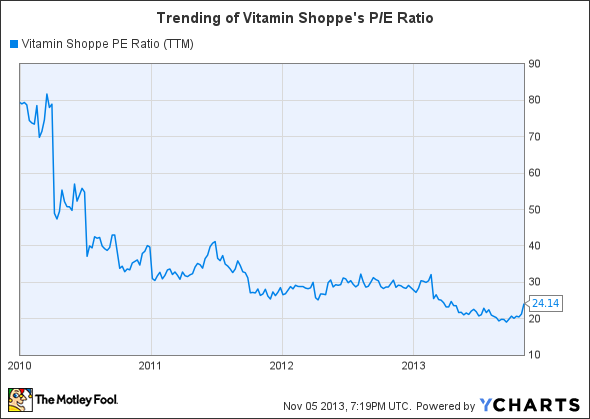

Despite the short-term pressure from acquisition integration costs and the operating expense associated with the opening of new stores and distribution facilities, Vitamin Shoppe remains consistently profitable. The company's third quarter results included EPS of $0.53, and even after the post-earnings spike the company's shares trade at a reasonable trailing price to earnings ratio of 24; while a P/E ratio of 24 may not seem cheap, it is at the very low end of Vitamin Shoppe's historical valuation range as noted below:

VSI P/E Ratio (TTM) data by YCharts

Strong revenue growth, tremendous opportunity for future growth, and a historically low valuation multiple are all reasons that investors are once again excited about Vitamin Shoppe. But as with any investment, there are risks that need consideration.

Strong competition from large competitors

The primary risk to Vitamin Shoppe's long term growth trajectory is the significant competition that it faces from much larger competition. As noted in the table below, even "niche" specialty retailers like GNC Holdings have a significantly larger installed base than Vitamin Shoppe:

VSI | GNC | WAG | AMZN | |

|---|---|---|---|---|

Market capitalization (in billions) | $1.5 | $5.7 | $57.3 | $164.6 |

TTM revenue (in billions) | $1.0 | $2.6 | $72.2 | $70.1 |

Store count | 640 | 8,400* | 8,100 | N/A |

Revenue growth (most recent quarter) | 14% | 8.7% | 5.1% | 23.8% |

SSS growth (most recent quarter) | 2.6% | 8.2% | 4.6% | N/A |

* Includes "store within a store" locations

While Vitamin Shoppe outpaced GNC Holdings' revenue growth of 9% in the most recent quarter, it is interesting to note that GNC Holdings' SSS growth of 8% was dramatically higher than Vitamin Shoppe's 2.6% growth. Likewise, well-established pharmacy operator Walgreens has driven most of its recent growth with SSS increases that are higher than Vitamin Shoppe's most recent results.

While Vitamin Shoppe, GNC Holdings, and Walgreens all compete using an omni-channel strategy that includes both brick-and-mortar stores and e-commerce, it is impossible to ignore competition from Amazon.com, a company on a quest to take over the world. Amazon.com has a dedicated Vitamins & Dietary Supplements section that offers comparable products to Vitamin Shoppe. Each of these companies (and numerous others) are multiple times the size of Vitamin Shoppe and have significantly more resources to devote to the capture of market share in Vitamin Shoppe's niche.

It is important to highlight that Amazon.com is both an ally and competitor to Vitamin Shoppe; Vitamin Shoppe sells almost a thousand different items on Amazon.com and even offers customers points toward Vitamin Shoppe's loyalty program for purchases made on Amazon.com. While these sales can help drive Vitamin Shoppe's growth, they are also at a lower margin given Amazon.com's fees. Additionally, Amazon.com is advertising competing products in such a way that limits the likelihood that a customer's order of multiple items will be entirely Vitamin Shoppe products.

Looking ahead

The opportunity for Vitamin Shoppe to continue on its current growth trajectory remains strong given all of the growth drivers in which the company is investing. Management remains committed to a disciplined growth plan and the maintenance of a net cash position on the balance sheet, which provides the company with both stability and the flexibility to pursue additional acquisitions. Analysts project that Vitamin Shoppe will grow earnings at 15% per year over the next five years; this projection appears to be reasonable and an indicator that Vitamin Shoppe is poised to outperform the market.

However, the number of well-run competitors seeking to grab a piece of Vitamin Shoppe's core and adjacent specialty markets is certainly worth consideration. Going forward it will be important for investors to monitor competitive developments and Vitamin Shoppe's SSS results; the continuation of Vitamin Shoppe's streak of SSS growth (currently 32 consecutive quarters) and a return to mid single digit growth in 2014 will be a strong signal that the company is performing well. In contrast, a continuation of low SSS results like the most recent quarter (or worse) would be a definite red flag that competition is chipping away at Vitamin Shoppe's niche.

Vitamin Shoppe is a compelling investment idea for investors that understand the growth opportunity and will monitor the company's progress in relation to the competitive environment. With investors regaining confidence in the company's growth prospects, there is also potential for near-term gains as the correlation resumes between revenue growth and share price.

Tired of watching your stocks creep up year after year at a glacial pace? Motley Fool co-founder David Gardner, founder of the No. 1 growth stock newsletter in the world, has developed a unique strategy for uncovering truly wealth-changing stock picks. And he wants to share it, along with a few of his favorite growth stock superstars, WITH YOU! It's a special 100% FREE report called "6 Picks for Ultimate Growth." So stop settling for index-hugging gains... and click HERE for instant access to a whole new game plan of stock picks to help power your portfolio.

The article A Healthy Outlook for Vitamin Shoppe originally appeared on Fool.com.

Brian Shaw owns shares of Amazon.com. The Motley Fool recommends Amazon.com. The Motley Fool owns shares of Amazon.com. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.