This Diabetes Giant Could Face 3 Major Challenges

Novo Nordisk , the world's largest manufacturer of insulin, slid nearly 8% on Thursday after it reported its third- quarter earnings.

For its third quarter, Novo's net income rose 14% year over year to 6.48 billion kroner ($1.18 billion), but missed the 6.55 billion kroner that analysts polled by Bloomberg had expected. Revenue rose 3.4% to 20.5 billion kroner ($3.7 billion), but also fell shy of the consensus estimate of 21.1 billion.

Sales of Novo's insulin analogs (also known as "modern insulins") -- NovoRapid/Novolog, NovoMix, and Levemir -- climbed 5.8% to 9.39 billion kroner ($1.7 billion), accounting for nearly half of the company's top line.

However, Novo's share of the global insulin market fell slightly from 49% to 48%, due to increased competition from Sanofi and other competitors.

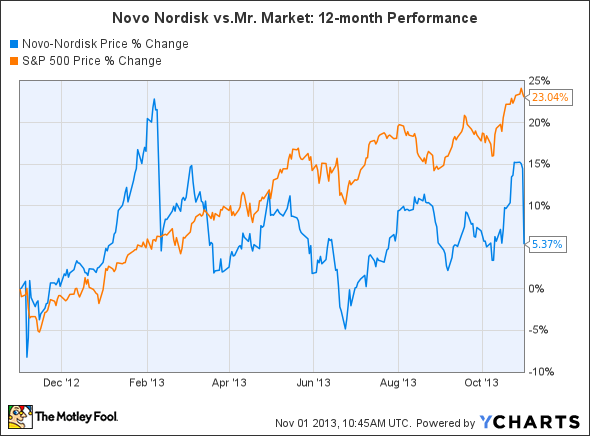

Bouncing back from the rejection of Tresiba

Over the past 12 months, shares of Novo Nordisk have declined 5%. The stock took a huge hit in February after the FDA rejected its new long-acting insulin, Tresiba, due to heart risk concerns.

Source: YCharts.

The FDA asked for new tests on Tresiba, pushing a potential U.S. launch back to 2016 or 2017. Tresiba was considered Novo's best chance at pushing back against Sanofi's top-selling insulin Lantus, which generated $6.8 billion in sales last year. Tresiba is currently approved in seven countries.

Focusing on the GLP-1 market

To bounce back from that disappointing setback, Novo has been focusing more on Victoza, a newer GLP-1 agonist treatment that stimulates natural insulin production within the body. GLP-1 drugs are rising in prominence, and their global market share of diabetes treatments has risen from 5.6% to 6.8% over the past year.

At the end of the third quarter, Victoza remained the dominant GLP-1 treatment on the market with a 70% global market share, up from 66% a year earlier. Sales of Victoza climbed 20% to 2.84 billion kroner ($520 million), accounting for 14% of Novo's top line.

Yet Victoza's dominance of the GLP-1 market might not last much longer, since newer competitors have emerged. Bristol-Myers Squibb , AstraZeneca , and Sanofi now all have approved GLP-1 treatments on the market.

Bristol-Myers Squibb and AstraZeneca's Byetta/Bydureon generated $194 million in sales for Bristol-Myers and $100 million for AstraZeneca last quarter -- making it one of the fastest rising threats to Victoza. Meanwhile, Sanofi's Lyxumia is approved in parts of Europe, Japan, and Mexico, and generated $4.1 million in sales last quarter.

In addition, Eli Lilly is also working on a new GLP-1 drug, dulaglutide, which has shown favorable comparisons against Byetta/Bydureon and Merck's Januvia during clinical trials.

The threat of newer treatments

While it's clear that Novo Nordisk's two pillars of growth are insulin analogs and Victoza, both businesses could be threatened by next-generation diabetes treatments such as SGLT2 (sodium glucose co-transporter) inhibitors.

SGLT2 inhibitors help diabetes type 2 patients excrete glucose through the urine, which can keep blood sugar levels under control and possibly reduce the number of insulin injections needed daily.

Those two factors -- that they can control blood sugar levels, and reduce the need for insulin -- could become problems for Novo if they become an industry standard. To date, only one SGLT2 inhibitor, Johnson & Johnson's Invokana, has been approved in the United States. Bristol-Myers and AstraZeneca's SGLT2 inhibitor Forxiga is approved in Europe, but was rejected in the U.S. last February by the FDA with a request for additional safety data.

Meanwhile, other newer drugs like Merck's Januvia and Janumet (which is Januvia combined with metformin, another diabetes drug) are rising in popularity and now being compared favorably to Victoza. Januvia belongs to another new class of diabetes drugs known as DPP-4 inhibitors, but its ultimate goal is the same as Victoza -- to increase insulin production and decrease the production of the hormone glucagon, which raises blood sugar levels.

Diversifying into bleeding disorder treatments

Therefore, Novo might not be well-diversified enough to defend its top line against that upcoming market shift. A possible area of diversification is in treatments for hemophilia, or uncontrollable bleeding.

Novo currently has one major treatment for hemophilia A and B on the market, NovoSeven, which generated $1.5 billion in revenue in 2012. However, NovoSeven lost patent protection in the United States and several other regions in 2010 and 2011, and the company expects sales to continue declining. Nonetheless, NovoSeven sales still rose 7% year over year in the first nine months of 2013 to 7.0 billion kroner ($1.3 billion) -- or 11% of Novo's total sales.

To replace NovoSeven, the company is counting on its new hemophilia A treatment, NovoEight, to pick up the slack. NovoEight was approved by the FDA in October, but Novo does not plan to launch NovoEight in the U.S. until early 2015, out of fear of accidentally violating third-party patents. Nonetheless, this was an encouraging development for Novo in the U.S., after the FDA rejected rFXIII, a treatment for a rare bleeding disorder, on grounds that there were problems with its manufacturing process in August.

NovoEight has also received a positive recommendation from Europe's Committee for Medicinal Products for Human Use, which could put it on track for a European launch and approval by early next year.

However, investors shouldn't expect Novo to have an easy time breaking into the market for bleeding disorders as easily as it dominated the one for diabetes. Companies such as Baxter, Pfizer, and Bayer are already firmly entrenched in this fairly mature market.

The Foolish bottom line

On the surface, Novo Nordisk looks like a solid investment -- investing in the world's largest insulin maker as global diabetes rates climb, seems like a no-brainer. Yet the company has three major weaknesses:

Its market share in insulin may have peaked, due to rising competition from Sanofi and other competitors.

Victoza faces an onslaught of similar GLP-1 agonist drugs and other "next-generation" treatments.

The company's best hope for diversification -- bleeding disorder treatments -- could face some tough competition from entrenched competitors.

However, if it can hold the line against Sanofi, demonstrate that Victoza can remain the dominant GLP-1 treatment on the market, and that NovoEight can seamlessly replace NovoSeven, shares of Novo Nordisk -- which is up more than 200% over the past five years -- could keep rising.

The best way to play the biotech space is to find companies that shun the status quo and instead discover revolutionary, groundbreaking technologies. In The Motley Fool's brand-new FREE report "2 Game-Changing Biotechs Revolutionizing the Way We Treat Cancer," find out about a new technology that big pharma is endorsing through partnerships, and the two companies that are set to profit from this emerging drug class. Click here to get your copy today.

The article This Diabetes Giant Could Face 3 Major Challenges originally appeared on Fool.com.

Leo Sun has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.