The Scariest Stock I Own

In the spirit of Halloween, allow me to introduce the scariest stock I own: Ultra Petroleum . A natural-gas exploration and production company with about $1.9 billion in debt on its balance sheet, Ultra is essentially a leveraged bet on the future of natural-gas prices and production. Its fortunes swing largely with the price it can capture for producing the gas it pulls from the ground.

Natural gas is an incredibly volatile commodity, with prices in recent years ranging from less than $2 per thousand cubic feet to more than $10. The chart below from the U.S. Energy Information Administration shows just how large the swings have been in recent years:

So why own the stock?

Add the volatility in the price of its primary product to the leverage on its balance sheet, and there's no wonder why Ultra Petroleum's stock has moved around substantially in recent years. In spite of these very real points of concern, there are still several reasons why I'm holding on to those shares.

1: A hedge against natural-gas prices: In our home, our furnace, water heater, outdoor grill, and clothes dryer are all powered by natural gas. As a consumer, I'm thoroughly enjoying the current low prices, but I lived through -- and paid gas bills during -- the recent spikes above $10. Because Ultra Petroleum's fortunes are tied to natural-gas prices, by owning its shares, I as an investor stand to benefit from higher gas prices, even while I could get burned as a consumer.

2: Ultra Petroleum is a low-cost producer: If natural-gas prices stay down, the only companies that will be able to produce the commodity profitably are those that, like Ultra Petroleum, keep their overall costs low. If natural-gas prices increase, higher profits should flow to the company's bottom line fairly quickly, potentially rewarding shareholders through a higher stock price as a result of those improved earnings.

3: The likely energy of the future. Natural gas has key environmental advantages over coal and oil-based fuels, is abundant in the U.S., can be transported easily through pipelines, and can be used for power, heat, and transportation. The advantages of natural gas are amazingly clear, and I firmly believe that consumption will increase in the future as increased infrastructure is built around taking advantage of the fuel. Even if prices stay low, an increase in consumption means more production.

Other ways to invest in natural gas

If the idea of owning a debt-laden commodity-producer doesn't appeal to you but you still believe in the future of natural gas, there are other options for investing. One is to own shares in the pipeline infrastructure that moves that gas from producers to storage and ultimately to the consumers. Kinder Morgan is the largest natural-gas pipeline company in America. On top of its existing infrastructure, the company has identified about $13 billion in expansion opportunities.

The benefit of Kinder Morgan and its peers is that the pipelines get paid based more on the amount of gas that flows through them than on the price of that gas. If you believe natural-gas consumption will rise even if (or perhaps especially if) prices stay low, pipeline companies stand to benefit as more gas is moved around.

Of course, the pipeline companies come with their own challenges. One of the biggest is that building a new pipeline is a very capital-intensive proposition. As a result, pipeline companies -- Kinder Morgan included -- generally have lots of debt on their balance sheets.

Additionally, as TransCanada found when its permit request for the Keystone XL Pipeline was denied, building a pipeline takes political savvy, as well as technical skills. Unless and until the permit is approved, the money TransCanada has already spent on the Keystone XL is effectively a "sunk cost" that was spent but can't be used to its full potential.

As another alternative to either the producers or the pipelines, it is possible to invest in natural gas as a commodity itself, largely through exchange-traded funds that attempt to track the price of that commodity. Unfortunately, those ETFs also come with their own problems.

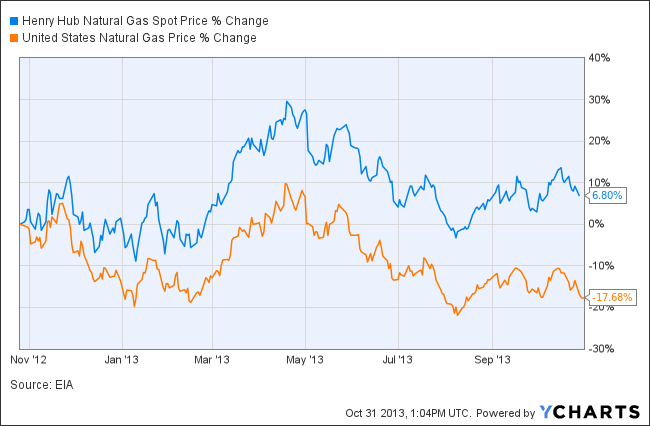

For instance, the United States Natural Gas ETF attempts to track the price of natural gas through investing in futures contracts.However, between contango (when futures prices are higher than spot prices) making that sort of strategy generally lose money over time and the ETF's 1.08% expense ratio, the fund generally underperforms the commodity's price over time. Check out this chart to see how badly the United States Natural Gas ETF has trailed the commodity's price in the past year:

Henry Hub Natural Gas Spot Price data by YCharts.

A structural underperformance like that makes the United States Natural Gas ETF an even scarier way to consider investing in natural gas than owning Ultra Petroleum's stock.

Get past fear and get invested

Ultimately, every investment has its potential pluses and minuses, and no stock is without risk. Investing can be scary, but the more you know about the company you're considering buying, how it makes its money, and what its future prospects are, the more you can replace fear with smart choices. Even if you never choose to invest in a leveraged producer of a volatile commodity, knowing how to look at a stock from the perspective of the business it operates is a great way to get started investing.

Don't let fear stand between you and a comfortable financial future

Millions of Americans have waited on the sidelines since the market meltdown in 2008 and 2009, too scared to invest and put their money at further risk. Yet those who have stayed out of the market have missed out on huge gains and put their financial futures in jeopardy. In our brand-new special report, "Your Essential Guide to Start Investing Today," The Motley Fool's personal finance experts show you why investing is so important and what you need to do to get started. Click here to get your copy today -- it's absolutely free.

The article The Scariest Stock I Own originally appeared on Fool.com.

Chuck Saletta owns shares of Ultra Petroleum and Kinder Morgan. The Motley Fool recommends Kinder Morgan and Ultra Petroleum. The Motley Fool owns shares of Kinder Morgan and Ultra Petroleum and has the following options: long January 2014 $30 calls on Ultra Petroleum, long January 2014 $40 calls on Ultra Petroleum, and long January 2014 $50 calls on Ultra Petroleum. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.