A Growth Company You Might Not Know About

When you think of Wal-Mart , you likely think of a mature company that pays a generous dividend. (For the record, it currently yields 2.50%.) While Wal-Mart is one of the safest dividend plays you will find in the market, its top-line growth potential isn't excitingly high. The company can grow its top line via international expansion into emerging markets, its small-box stores launching next year, its food offerings, and its Sam's Club brand. However, as stated above, it's a mature company.

Then there's Costco , a company that's growing a little faster on the top line because consumers are interested in high-quality products at discounted prices. Costco yields 1.10%, which is not as much as Wal-Mart, but its faster top-line growth makes up for that. Costco is a very impressive company in nearly every facet.

Imagine a similar company that's growing even faster than Costco, primarily thanks to its locations in high-growth markets. It's not a domestic off-price retailer or a dollar store. While one potential negative does exist, this company appears to be a younger version of Wal-Mart or Costco, just in a completely different market.

A company to keep on your radar

PriceSmart owns and operates membership shopping warehouse clubs in Latin America and the Caribbean. By its own admission, it's similar to Costco and Sam's Club. However, there are several key differences.

For one, PriceSmart's sales per square foot are just north of $1,000, versus $814 for Costco and $586 for Sam's Club. PriceSmart's warehouses are smaller, with the average store size ranging between 50,000 and 75,000 square feet. Costco's warehouses mostly range from 73,000 to 205,000 square feet and Sam's Club's warehouses from 70,000 to 190,000.

PriceSmart also offers lower membership fees than Costco and Sam's Club. The average membership fee at PriceSmart is $35. Membership fees for Costco's Gold Star individual and Business memberships are $55, and membership fees for Sam's Savings and Sam's Business are $45. Additionally, PriceSmart uses a different merchandising approach, which targets local consumer demands.

However, the biggest benefit for PriceSmart is that its warehouses are located exclusively in Latin America, where consumers have increasing purchasing power thanks to growing economies and the emergence of the middle class. Consider the company's top-line growth over the past several years:

PSMT Revenue (TTM) data by YCharts.

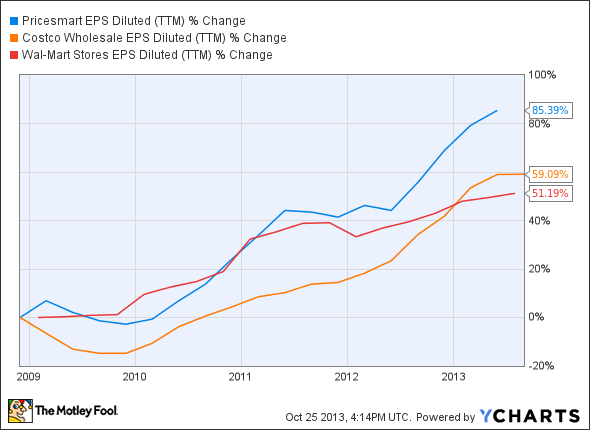

If you're worried about the bottom line, then you worry too much:

PSMT EPS Diluted (TTM) data by YCharts.

As far as PriceSmart's recent performance is concerned, the past few months have been impressive (all year over year):

July Net Sales: Up 11.9%

July Comps: Up 8.9%

August Net Sales: Up 15.5%

August Comps: Up 9.4%

September Net Sales: Up 11%

September Comps: Up 9.1%

Looking ahead, a lot of potential exists for PriceSmart. It only has 31 warehouses in 12 countries at the moment. These numbers are likely to increase. If a retailer sees success at its current locations, it's going to expand.

That one potential negative

PriceSmart trades at 32 times forward earnings. Considering the company's rampant growth, this is only a potential negative, but it does mean that high expectations need to be met.

If you're looking for a little more comfort with your next investment without sacrificing growth potential, note that Costco only trades at 21 times forward earnings. Wal-Mart trades at just 13 times forward earnings.

PriceSmart does yield 0.60%, but that's not likely to sway your decision, especially when Costco and Wal-Mart yield 1.10% and 2.50%, respectively.

As far as debt management, PriceSmart sports a debt-to-equity ratio of 0.16, which is much stronger than the industry average of 0.60. Investing in a company with top- and bottom-line growth potential that's also showing quality debt management is always a plus. Costco and Wal-Mart sport debt-to-equity ratios of 0.47 and 0.74.

The bottom line

PriceSmart seems to be doing everything right. Its warehouses are located in high-traffic areas in cities throughout Latin America and the Caribbean. With only 31 warehouses, there is a lot of room for growth. The one potential negative is its valuation. If any surprise negative news comes out, the stock could drop quickly. However, savvy investors know not to pay attention to short-term moves in stock prices. If anything, these drops provide opportunities to add to positions in strong underlying companies. All that said, Costco and Wal-Mart are likely to be safer long-term investments thanks to their size, brand strength, and marketing power. It all comes down to your risk tolerance.

6 more growth stocks for your portfolio

Tired of watching your stocks creep up year after year at a glacial pace? Motley Fool co-founder David Gardner, founder of the No. 1 growth stock newsletter in the world, has developed a unique strategy for uncovering truly wealth-changing stock picks. And he wants to share it, along with a few of his favorite growth stock superstars, WITH YOU! It's a special 100% FREE report called "6 Picks for Ultimate Growth." So stop settling for index-hugging gains... and click HERE for instant access to a whole new game plan of stock picks to help power your portfolio.

The article A Growth Company You Might Not Know About originally appeared on Fool.com.

Fool contributor Dan Moskowitz has no position in any stocks mentioned. The Motley Fool recommends Costco Wholesale and PriceSmart. The Motley Fool owns shares of Costco Wholesale. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.