What If Lululemon, Under Armour, and Nike Are All Overvalued?

Under Armour reported earnings Thursday, and while results were strong, shares tumbled. The stock fell as much as 7.9% even as the apparel-maker raised its outlook, and beat top- and bottom-line estimates on 26% sales growth. What seemed to throw off the market was the company's lower-than-expected preliminary guidance for 2014, as CFO Brad Dickerson said Under Armour was targeting the lower end of its 20% to 25% long-term revenue and operating income growth range.

Shares of Under Armour have surged this year, gaining 74% before yesterday's sell-off. That jump has come on little more than delivering solid results, beating earnings estimates in each of its last five quarters, and growing its top line at a clip near 25%. But with that strong share price appreciation has come a vertigo-inducing valuation. Under Armour now trades at a trailing P/E of 58, and its forward P/E of 43 still bakes in high expectations.

But this lofty valuation isn't just a trait of Under Armour stock. Its two primary rivals also carry steep price tags, as the chart below shows.

Company | Market Cap | P/E Ratio |

|---|---|---|

Under Armour | $8.4 billion | 58.4 |

Nike | $67.2 billion | 25.5 |

lululemon athletica | $10.5 billion | 39.2 |

Industry | $86.1 billion | 30.4 (weighted average) |

Source: Yahoo! Finance, author calculations.

It's rare to find a $86 billion company trading at a P/E of 30, twice the long-term average of the S&P 500. Essentially, only a handful of tech stocks such as Amazon.com and Facebook are this large and expensive, and the market assigns them such valuation because of their monopoly-like position in fast-growing markets. By contrast, the apparel industry offers little in the way of an "economic moat," as each company has primarily sought to distinguish itself with brand recognition and product quality.

Is the sports apparel biz a zero-sum game for these players, or is there enough room in the market to make them all winners?

Stretching to the limit

As the elephant in the room, with revenue dwarfing both Under Armour and Lululemon, Nike would seem to have the most to say about the industry's future. The Swoosh recently laid out a bold plan to reach $36 billion in sales by fiscal year 2017, a more than 40% increase from fiscal 2013. Nike said it expects $20 billion of those sales to come from North America and Western Europe, where it sees high-single-digit growth, and most of the rest to come from developing markets, including China and Eastern Europe, where it sees growth in the low double digits. It expects e-commerce sales to nearly double to $8 billion.

In its presentation, Nike noted that the middle-class population in the so-called BRIC countries (Brazil, Russia, India, China) will expand by 1 billion over the next decade, and also remarked that sports like running and basketball have never seen more interest around the world. Nike was also optimistic about the effect that hosting the World Cup and Summer Olympics would have on Brazil, a sport-loving country with a population of 200 million.

Under Armour and Lululemon are much more focused on the North American market than Nike, but Nike was similarly optimistic about its home region, noting that sales have grown there by 40% over the last three years even as naysayers said that that market had already reached maturity.

As Under Armour competes in many of the same categories as Nike, it will likely benefit from any market expansion in North America as demand for sports and exercise apparel increases.

Lululemon, meanwhile, is a brand nearly synonymous with yoga, an activity that has exploded in popularity over the last decade. Money spent on yoga products has increased 87% over the last five years in the U.S., and the number of Americans who practice is increasing at a rate of 20% each year. Lululemon helps promote the ancient practice by offering free classes in its stores, and reimbursing employees for any outside classes that they take.

Lululemon's next frontier appears to be abroad, where its initial showrooms and stores in Europe and Asia have gotten an overwhelmingly positive response.

Notably, both Nike and Under Armour believe the women's market, Lululemon's forte, is a huge growth opportunity.

Wearable technology

Though readers may think of Google Glass or smart watches when they hear the phrase "wearable technology," companies like Nike and Under Armour are just as much a part of this transformative shift. With its Nike+ family of products such as its Fuelband, the sneaker king is taking performance measurement to the next level. The wristband tracks athletic activity, the intensity of your workout, and even monitors your sleep, giving you a Fuel score based on your total activity. The product is just one component of Nike+ , which the company calls "an ecosystem of digital products and experiences designed to measure, motivate, and empower you to improve," Above all, Nike+ and the Fuelband serve as an example of an entirely new category Nike has been able to create simply by harnessing technological advances.

Under Armour, similarly, makes no bones about its ambitions in wearable technology. In a new commercial, it tells viewers, "The next great athletic innovation isn't available yet, but it's being built at Under Armour right now." Among other ideas, the company is working on a shirt with lights built into it so runners or other users can be seen at night. Under Armour solicits such ideas at its annual "Future Show," and CEO Kevin Plank is well aware of how fast things change in the industry, saying:

Our consumers' expectations shift constantly higher and they count on their favorite brands to consistently take them someplace new. The company that we are building to deliver on that promise is in constant evolution. We are a different company every six months.

Lululemon, on the other hand, has avoided the wearable technology field, a sensible move seeing as the brand is aligned with the spirituality of yoga. Still, the opportunity exists if it should so seek it.

Foolish takeaway

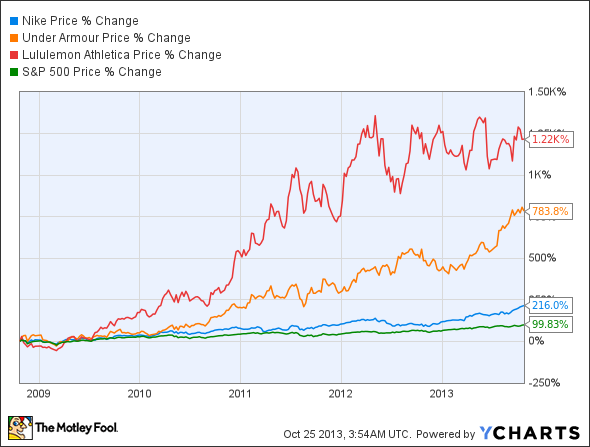

All three of these companies are great brands, and their stocks' performance over the past five years reflects their strength.

Notably, all three have seen their share price appreciation outpace their earnings-per-share growth. Given that, we are likely to see more pullbacks in the future for these stocks like we saw today with Under Armour. Despite the likely multiple compression ahead, their brand strength and growth opportunities should be enough to enable them to outperform the market over the long run, though most likely not by the huge margins we've seen in the last five years.

Stocks that are ready to rule the world

The global marketplace represents a huge opportunity for Nike, Lululemon, and Under Armour. With a billion new middle-class consumers sprouting up over the next decade, these companies could have a field day. In fact, The Motley Fool recently named Nike as one of "3 American Companies Set to Dominate the World." To find out who the other two are, just click here to get your free copy of the report before it's gone.

The article What If Lululemon, Under Armour, and Nike Are All Overvalued? originally appeared on Fool.com.

Fool contributor Jeremy Bowman owns shares of Nike. The Motley Fool recommends Amazon.com, Facebook, Google, lululemon athletica, Nike, and Under Armour. The Motley Fool owns shares of Amazon.com, Facebook, Google, Nike, and Under Armour. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.