A Company Capable of Outperforming Harley-Davidson

When you invest in a company that is seeing increased demand while also improving the bottom line, your odds of success greatly increase. When a dividend is added to the scenario and the balance sheet is clean, strongly consider an investment in that company.

In the current economic environment, you probably wouldn't expect a recreational vehicle company to be performing well. However, the company featured in this article has defied the odds and rewarded its investors handsomely.

High expectations

The following company recently saw its third-quarter revenue jump 25% year over year, seeing strength both domestically and internationally. Part of the international strength has been thanks to acquisitions. However, as long as the top and bottom lines grow in tandem, it doesn't matter if it's organic growth or inorganic growth. This company's gross margin also improved 90 basis points to 30.40% thanks to higher selling prices and lower costs. Furthermore, it recently raised guidance.

This company is none other than Polaris . The name wasn't brought up until now because it's not often talked about on the street. If the name had been revealed first, then you might have disregarded it.

Polaris designs, manufactures, and sells off-road vehicles, snowmobiles, motorcycles, and more. Its off-road vehicles are by far the biggest part of the operation. Therefore, it's good to see that off-road vehicle sales jumped 23% year over year, thanks to strong demand for ATVs. However, that already happened. Investors want to know about the future. The future looks bright.

Polaris had $3.2 billion in sales in fiscal-year 2012. That's a big number for a company focused on off-road vehicles. However, Polaris recently relaunched its Indian motorcycles (Chief Classic, Chief Vintage, and Chieftain), it has its Victory motorcycles, and it's seeing high demand for almost everything it sells.

Based on these trends, Polaris now expects sales to total $8.0 billion by 2020. If this prediction comes to fruition, Polaris would more than double its sales in seven years. Considering that the company came into existence in 1987, that would be quite a feat. Of course, there are no guarantees. If the real estate and stock markets don't hold, then all bets are likely off. Polaris can't worry about that. It can only grow its business to the best of its ability, and it's very good at doing so.

For fiscal year 2013, Polaris expects diluted earnings per share to grow at a 20%-22% clip, and for sales to increase 15%-16%.

Polaris vs. peers

When you think of recreational vehicles, you likely think of Harley-Davidson. While Polaris' motorcycles have the potential to steal some share from Harley-Davidson, they're not likely to make a significant impact. Harley-Davidson is doing well itself with its third-quarter revenue increasing 7.5% and its diluted EPS jumping 23.7%. Retail motorcycle sales improved 15.5% globally as well as 20.1% domestically.

For the year, Harley-Davidson expects to ship 259,000-264,000 motorcycles to dealers and distributors. That being the case, it might have crossed your mind as to why Polaris would present a better investment opportunity than Harley-Davidson. We'll get to that soon. Let's first take a look at Arctic Cat , a recreational vehicle company that designs, manufactures, and sells snowmobiles, ATVs, and UTVs.

Arctic Cat has also been a strong performer lately. It's looking to spend more on research and development (16% increase over last year) in order to help drive sales. At the same time, Arctic Cat is moving toward in-house manufacturing to help reduce costs. It would be impressive if Arctic Cat could grow its top and bottom lines at the same time. It has already done so. Actually, all three companies mentioned here have accomplished this goal:

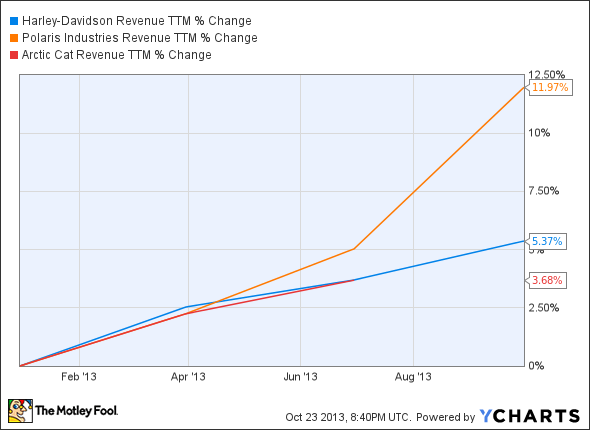

Top line

HOG Revenue TTM data by YCharts

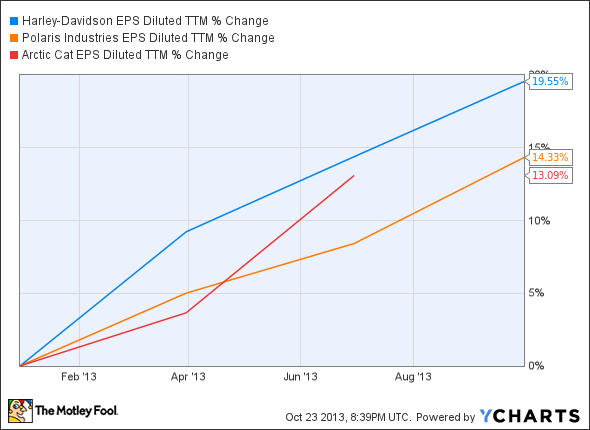

Bottom line

HOG EPS Diluted TTM data by YCharts

While Arctic Cat is a solid company, it doesn't have the marketing power of its peers. While the company sports an ideal debt-to-equity ratio of zero, it only yields 0.70%. Polaris yields 1.20% while sporting a debt-to-equity ratio of 0.13 -- also impressive. Harley-Davidson yields 1.30%, but its debt-to-equity ratio of 1.96 isn't nearly as comforting.

If you're thinking that Polaris doesn't stand a chance at outperforming Harley-Davidson going forward, you might want to compare their stock performances over the past decade:

The bottom line

Harley-Davidson is one of the strongest brands around, and it's highly likely to remain a long-term winner. However, it makes a lot of sense to go with a recreational company seeing similar growth, a similar yield, and a much cleaner balance sheet -- Polaris.

Looking for the some of the safest dividends around?

If you're looking for some long-term investing ideas, you're invited to check out The Motley Fool's brand-new special report, "The 3 Dow Stocks Dividend Investors Need." It's absolutely free, so simply click here now and get your copy today.

The article A Company Capable of Outperforming Harley-Davidson originally appeared on Fool.com.

Dan Moskowitz has no position in any stocks mentioned. The Motley Fool recommends Polaris Industries. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.