3 Red Flags for This Biotech IPO

What if I told you that a single company could transform the way the world manufactures pharmaceuticals and chemicals and grows major agricultural crops and fish? What if the same company could change the way in which governments respond to defense threats, public health pandemics, and industrial and natural disasters? It may sound perplexing and confusing, but Intrexon is just such a company.

The synthetic biology leader designs living organisms that are more efficient and productive at performing a given task, which could be creating chemicals and pharmaceutical compounds, remediating an oil spill, identifying bioweapons, or resisting droughts and pests (for crops and fish). Intrexon is at the forefront of creating and capturing value from the budding bioeconomy. The company's scientific capabilities may be astounding, but that doesn't always translate into a great investment. Here are three risks to evaluate when considering Intrexon for your portfolio.

1. Partnerships with unproven companies

Intrexon's business model is pretty simple: form exclusive channel collaborations, or ECCs, with companies that can benefit from its proprietary synthetic biology technologies and collect royalties on the sale of products created within the collaboration. That takes a lot of expense and risk out of the equation, but it also takes time to build up a solid base of partners. Each will take a considerable amount of time to successfully develop and commercialize products and unfortunately, most of the 10 disclosed ECCs are with tiny and unproven companies.

Fibrocell Science, Synthetic Biologics, Oragenics, AmpliPhi, and Soligenix -- representing a combined market cap less than $400 million -- make up five of the ECCs. A small private company named Genopaver, which actually owns some pretty interesting intellectual property, brings the total to six, while an aquaculture company owned by Intrexon makes seven. Their small size doesn't mean they won't be successful (and Intrexon was able to wrestle away some excellent terms on potential future royalties), but these aren't big names that investors can feel great about.

What are the biggest names to brag about? ZiopharmOncology is currently executing two mid-stage trials in oncology using Intrexon's technology. The two molecules being developed are DNA therapeutics, which regulate interactions between proteins within the body to treat, control, and even cure cancer. There are several potential advantages of such therapies including a reduction in the toxicity of cancer treatments caused by introducing external proteins and chemicals to the body. That's enough for Intrexon to stick around because, despite Ziopharm's past failures, the synthetic biology leader owns more than 16% of the developmental biotech.

The ninth ECC is with Elanco, the animal health division of Eli Lilly . All revenue generated from the collaboration to date has been in the form of an upfront payment and reimbursed research costs. The pair has not disclosed the direction of the research, but judging from Elanco's business and Intrexon's technology I would guess it obviously has to do with antibacterials and other medications for animals. This may be the most promising partnership in terms of chances of success, given Elanco's global reach and $2 billion in sales last year.

Intrexon recently entered into ECC number 10 with India's Sun Pharma, but similar to the others, it will take years to bear meaningful fruit. Simply put, the company's business model is just not very investor friendly in the early stages of development.

2. Wall Street (...sigh)

I'm not sure why Wall Street analysts love to set up developmental industrial biotech and synthetic biology companies to fail, but it seems as if Intrexon will be at the mercy of such estimates until expectations are scaled back. Once again, that is going to really hurt investors. Analysts at JPMorgan called for second quarter revenue of $22 million. Actual revenue came in at $6.8 million (those same analysts were calling for sales of $85 million in the second half of the year). The average of four estimates currently calls for total fiscal year sales of $76 million with a low estimate of $27 million, according to Yahoo! Finance.

To put those gaudy numbers in perspective, first half sales actually totaled $10.8 million. Meanwhile, Intrexon has never exceeded $14 million in annual revenue. While the company is certainly on pace to set a new watermark in 2013 you have to wonder where Wall Street is expecting an additional $16 million to $105 million in sales to come from in the last two quarters. Unless a microbe that prints money (with watermarks and security threads) is about to be launched that I don't know about, there is absolutely no way the company can meet current estimates.

3. Are shares too expensive?

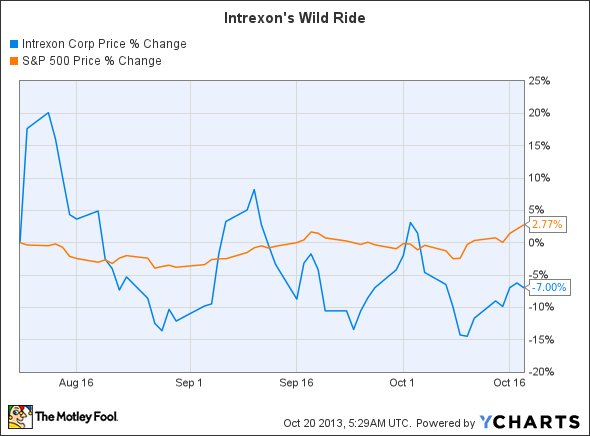

If Wall Street's unrealistic expectations aren't enough to scare you away (hint: they should be) then consider Intrexon's expensive valuation. It isn't surprising for a biotech IPO to be priced at such a lofty premium, but it doesn't make the company investment worthy either. Let's consider where the company's $2.1 billion market cap stands in term of sustainability.

We don't have 12-month trailing revenue figures to judge a P/S estimate on, so we'll use a combination of actual first half sales and a generous estimate of second half sales. Intrexon's valuation on December 31, 2013 would become:

Financial metric | Amount |

|---|---|

1H13 sales (actual) | $10.8 million |

2H13 sales (estimate, $10 million per quarter) | $20.0 million |

TTM Sales on Dec. 31, 2013 (estimate) | $30.8 million |

Shares outstanding (Oct. 18, 2013) | 93.82 million |

P/S (using current $2.1 billion market cap) | 70.1 |

Sources: SEC filings, Google Finance, author's calculations.

Remember, this is an extremely generous estimate and Intrexon's P/S would still be 70. Sure, the long-term potential is likely worth well over $2 billion. I just don't see the current business sustaining such a high valuation over the next few quarters and would rather wait for shares to pullback before starting a position, which I do plan on doing eventually.

Foolish bottom line

The long-term potential is incredible if Intrexon can attract more big names to its technology platform. Even then, it will take years to develop stable revenue streams. For now, investors probably shouldn't put too much faith in the majority of the companies developing products with it. That's why I think there is plenty of time to wait for Intrexon to develop its business and become a worthwhile company to hold for the long term. I'm a firm believer in industrial biotech and synthetic biology, but I won't be going anywhere near shares at current prices. Given analyst expectations, it is almost a certainty that shares will get crushed in the coming quarters. Buyer beware.

Can't wait for Intrexon?

This incredible tech stock is growing twice as fast as Google and Facebook, and more than three times as fast as Amazon.com and Apple. Watch our jaw-dropping investor alert video today to find out why The Motley Fool's chief technology officer is putting $117,238 of his own money on the table, and why he's so confident this will be a huge winner in 2013 and beyond. Just click here to watch!

The article 3 Red Flags for This Biotech IPO originally appeared on Fool.com.

Fool contributor Maxx Chatsko has no position in any stocks mentioned. Check out his personal portfolio, his CAPS page, or follow him on Twitter @BlacknGoldFool to keep up with his writing on biopharmaceuticals, industrial biotech, and the bioeconomy.The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.