Can Talisman Catch up to Its Canadian Counterpart?

Shares of Talisman Energy (NYSE: TLM) spiked after iconic, activist investor Carl Icahn revealed that he acquired nearly 6% of the Canadian energy company. But, it will take more than the billionaire who forced a management change-up for U.S. driller Chesapeake Energy for Talisman to compete with its national counterparts, notably Suncor Energy (NYSE: SU).

Canada dry is not true for energy companies

Partly thanks to Warren Buffett Suncor Energyis now on many investors' radar, and rightfully so. In August, the Oracle of Omaha revealed he acquired a $500 million stake in the multi-faceted energy company mostly known for pioneering Canada's commercial oil sands. In addition to its oil sand operations, though, Suncor explores and produces natural gas in regions around the globe and operates plants with wind and other renewable energy sources—giving it further protection from commodity price swings or bearish geographic trends.

But, Suncor's cash management system sets it apart from competition, a priceless advantage in the capital intensive business.

SU Cash from Operations TTM data by YCharts

For example, Suncor will fully fund its 2013 capital expenditures solely from cash generated from operations. Additionally, the firm is using its excess capital (up to $2 billion) to continue repurchasing its shares—generating even more value for investors. Competitor Canadian Natural Resources (NYSE: CNQ) also prides itself on its "strong free-cash flow generation ability." However, Canadian Natural Resources doesn't boast growth or earnings potential as strong as Suncor.

Suncor | Canada Natural | Enerplus | Talisman | |

|---|---|---|---|---|

EV/Rev | 1.55 | 3 | 3.74 | 3.02 |

P/S | 1.37 | 2.37 | 2.77 | 2.14 |

EPS | $1.86 | $1.30 | $- | $- |

*Data from Yahoo! Finance | ||||

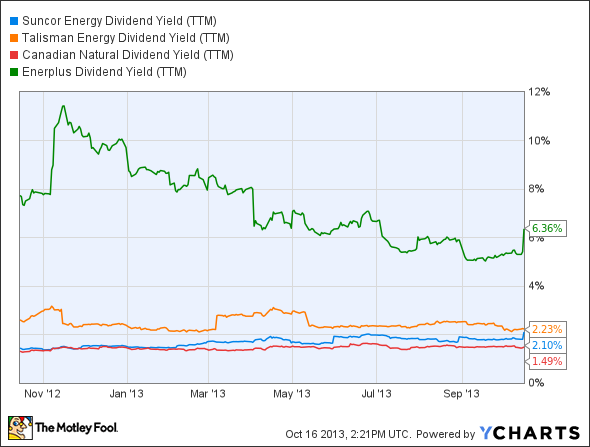

One explanation for the lower metrics is that Canadian Natural sells its oil via WTI prices, which sell at a discount to Brent prices (which Suncor utilizes). Additionally, as mentioned before, Suncor's various lines of business enable it to survive better through difficult times . But, Canadian Natural is still earning investors a return—unlike Enerplus Resources (NYSE: ERF)and Talisman. However, it is important to recognize Enerplus' unique value proposition; it offers investors an unorthodox dividend payment. Plus, because it is only about 3% above its book value, investors could consider it a safe haven compared to firms trading at higher prices.

SU Dividend Yield (TTM) data by YCharts

So, risk averse or income seeking investors may discover that Enerplus meets their needs, even though it isn't generating a profit.

Can Talisman get on track?

In light of declining shares, revenues, and earnings, Talisman brought Hal Kvisle, a former energy executive, out of retirement last year to turn around the company. Progress is still slow. Around $3 billion of assets in its offshore properties are up for sale (to generate much needed cash) while Moody's just reduced its credit rating from stable to negative. The sale is a late effort sign revealing that the leveraged company is trying to improve its weak financial performance while Moody's decision casts further doubt and concern over Talisman's future.

To be fair to Kvisle, though, redirecting a capital-intensive, upstream energy company takes patience and cash, along with a nearly endless list of good decision making and fortune. So, the attention from Icahn could be the spark Talisman needs.

In fact, as Icahn tweeted, "May have conversations with mgmt.(management) re(regarding) strategic alternatives, board seats, etc." Talisman is in a tough situation, and only time will tell if Icahn's efforts will prove fruitful. In the meantime, Suncor looks as good as ever.

Bottom line

Canadian energy companies are becoming more popular among investors. Even with different objectives or asset allocations (income seeking, high risk, diversification, etc), Suncor and Enerplus could fit into your portfolio. It still remains to be seen, though, if Talisman will make the cut too.

OPEC's worst nightmare

Imagine a company that rents a very specific and valuable piece of machinery for $41,000... per hour (that's almost as much as the average American makes in a year!). And Warren Buffett is so confident in this company's can't-live-without-it business model, he just loaded up on 8.8 million shares. An exclusive, brand-new Motley Fool report reveals the company we're calling OPEC's Worst Nightmare. Just click HERE to uncover the name of this industry-leading stock... and join Buffett in his quest for a veritable LANDSLIDE of profits!

The article Can Talisman Catch up to Its Canadian Counterpart? originally appeared on Fool.com.

Brendan Marasco has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.