Is Piper Jaffray Right About Clean Energy Fuels?

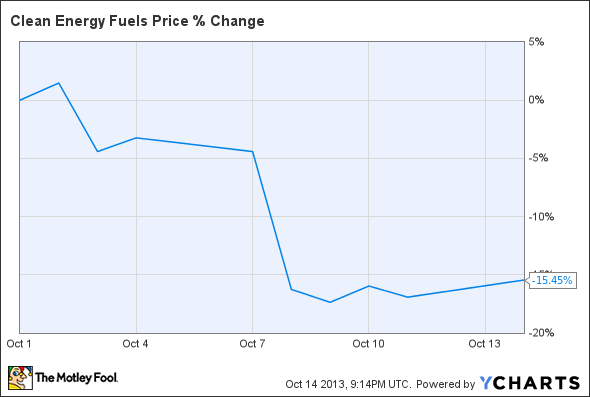

Last week, shares of Clean Energy Fuels took a beating when Piper Jaffray reiterated its "sell" call on the shares. Follow that up with Jim Cramer parroting the call, which was based on faulty analysis, and the stock price has fallen over 15% since the beginning of October:

Here's the rub: Just because the analysis was way off base, don't assume this means Clean Energy is a guaranteed success. Let's take a closer look.

Counting on someone else for your success is risky

Clean Energy Fuels, right now, is a play on two things: First, it's legacy business as a CNG (compressed natural gas) supplier for "return-to-base" vehicles like municipal transit, refuse pickup, and airport transit vehicles, and second, a very large bet on the trucking market transitioning away from diesel, and to LNG (liquefied natural gas) for long-haul shipping. So while Piper Jaffray and Cramer got their facts wrong, the company is still facing an uncertain future that is heavily tied to things that are largely outside of the company's control. For example:

The Westport Innovations - Cummins NG engines -- the only serious game in town right now -- will meet both reliability and performance expectations.

Shippers will have to be convinced that the cost-savings of NG outweigh the additional expense of NG-powered trucks, and that the cost-savings can be expected to continue over the life of the truck (five to 10 years or more.)

Shippers need to trust that there will be access to fuel wherever they make deliveries.

The only thing Clean Energy can directly control is the third one -- access to fuel -- by opening as manly locations on shippers' routes as it can. The first two, at best it can only influence. While management is doing a commendable job of getting as much positive information in the market as it can, the end-game is waiting for things to play out.

And while Clean Energy has been working closely with Westport to meet with customers and explain how the price of NG as a commodity has a much smaller effect on "at the pump" prices than oil does to diesel, it's still a matter of the shippers deciding to buy something from another company (the truck maker) before its product becomes an option. And frankly, that's a lot of counting on other companies for your own success.

And Westport has been facing plenty of challenges lately as it attempts to transition from a heavy R&D phase to an integrated manufacturer, and licensor of its proprietary technology. Never profitable as a public company, Westport disappointed investors recently with an unexpected public offering, diluting shareholders 10% through the 6 million shares sold to raise $175 million. The good news is that this should be the last hit to dilution, as management told investors that all its operating segments would be profitable, or at least cash-flow neutral by the end of 2013.

Building an infrastructure: Targeted or diversified? Chicken or the egg?

Solar City is targeting a much larger market with solutions for government, commercial, and residential customers. While Clean Energy's "America's Natural Gas Highway," or ANGH, is aimed at a small segment of the total transportation market (though it's one that uses a LOT of fuel) and spending big on the infrastructure in advance of the adoption, Solar City is building, as Chairman Elon Musk has described it, a "massive, decentralized utility," through its network of solar panels.

The basic premise is that each customer is signing an agreement that allows Solar City to sell the additional power that each installation generates back to the utility, while guaranteeing that the customer will pay less for the new system and their electricity than they were paying for electricity alone before. The biggest difference, is compared to Clean Energy's investment in the ANGH -- which is just a series of assets sitting unused until NG adoption picks up -- every installation that Solar City makes is immediately an asset that is producing energy and revenue.

And as the Fool's Travis Hoium says, combining the immediate value of each installation with the incredible growth that the company is projecting gives us a company with immense potential value.

Final thoughts

The biggest challenge that Clean Energy faces is the immense cost of building out infrastructure without any guarantees your customers will switch, where Solar City is in position to immediately capture customers and revenue -- with contracts that are measured in decades -- with every installation. The point? Don't immediately assume that just because Cramer and Piper Jaffray are terribly wrong on their analysis that the end result will be Clean Energy's stock price going up, because that's a matter of something else entirely -- and in many ways it's something that Clean Energy doesn't really have much control over.

A company you can count on

Imagine a company that rents a very specific and valuable piece of machinery for $41,000... per hour (that's almost as much as the average American makes in a year!). And Warren Buffett is so confident in this company's can't-live-without-it business model, he just loaded up on 8.8 million shares. An exclusive, brand-new Motley Fool report reveals the company we're calling OPEC's Worst Nightmare. Just click HERE to uncover the name of this industry-leading stock... and join Buffett in his quest for a veritable LANDSLIDE of profits!

The article Is Piper Jaffray Right About Clean Energy Fuels? originally appeared on Fool.com.

Jason Hall owns shares of Westport Innovations, Clean Energy Fuels, and SolarCity. The Motley Fool recommends Clean Energy Fuels and Westport Innovations. The Motley Fool owns shares of SolarCity and Westport Innovations. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.