Is the For-Profit Education Mess About to Repeat Itself?

More than two and a half years ago, I warned Fools that investing in for-profit education companies -- specifically for-profit colleges and universities -- was a bad idea. As you'll see, that prediction has proven true. But more importantly, it seems a new company might be on the verge of repeating the exact same mistakes.

A swift downfall

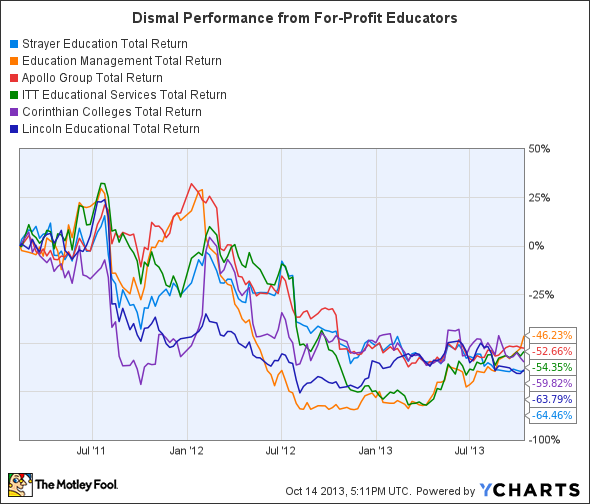

Back in February 2011, I focused on six specific companies that ran for-profit colleges and universities: Apollo Group , Corinthian Colleges , Education Management , Lincoln, ITT , and Strayer.

Here's how they have performed since then:

STRA Total Return Price data by YCharts.

Averaged out between these six companies, the average stock has lost 57% of its value. Over the exact same time frame, the S&P 500 has returned 35%. That means an investment in these companies is underperforming the market by an astounding 92% since February 2011!

The surface reasons for this downfall are fairly simple to see: The colleges rely too heavily on government funding, they have severely declining enrollments, and an alarmingly high percentage of their students are defaulting on their loans.

But couched underneath these surface factors was an even more pernicious fact: The Government Accountability Office uncovered admissions recruiters at Apollo, Corinthian, and Education Management who were misleading potential students and/or encouraging them to falsify their federal financial aid forms. Tens of thousands of students were being recruited for a service that wasn't fit for their personal circumstances -- leaving them with little to show for their decision but a boatload of debt.

Ostensibly, this practice owed to the fact that these counselors were incentivized to recruit as many students as possible; their commissions were based on how many students they could bring in. When the Obama administration outlawed the commission-based system, things started heading south for these schools.

History repeating itself?

With that as a backdrop, let's now consider why famed value investor Whitney Tilson (who used to occasionally write for the Motley Fool) thinks that shorting shares of K12 is a good idea.

The company has several revenue streams, but its most important one -- accounting for 86% of this year's estimated revenue -- comes from providing managed public schools via online charter schools. It is this segment that Wilson thinks is bound to implode.

The original idea behind these schools was simple: Some kids learn better when allowed to explore on their own, especially gifted students. For a few years, that plan attracted a decent number of students and growth to the company -- with most funding coming from state and local governments in the form of per-pupil monies.

But interviews with former administrators and teachers from K12 paint a picture of a company that changed course dramatically once it went public. Jeff Shaw, a former head of school for an Ohio K-12 school, said that K12 is "best suited for students who are hard-working, internally motivated self-starters, and who have at least one parent in the home during the school day."

And yet a few years after the company's IPO, "corporate assumed control of ... the enrollment process ... via call centers that were encouraging enrollment and enrolling students who were obviously ill-suited for learning in a virtual environment."

Sound familiar?

Tilson thinks so, and as he stated in a recent presentation, "States (and the IRS) are waking up to what K12 is doing and the company is coming under increased scrutiny ... and I believe this trend will accelerate."

Speaking as a former teacher at a KIPP charter school (full disclosure: Tilson donates to KIPP), I can unequivocally tell you that Tilson is right about his assertions. High-risk students rarely flourish in unstructured, unsupervised settings, and it's only a matter of time before the enrollment numbers start to show this.

In fact, it seems those problems are already starting to crop up: Shares of the company plummeted last week on news that enrollment numbers weren't as high as expected and guidance was cut for the full year.

I generally think investing in any for-profit education company is a bad idea. There are much better options out there for investors -- including companies that you can buy and comfortably own for decades.

We've uncovered the pillars of such a portfolio today, and we're willing to share "The Motley Fool's 3 Stocks to Own Forever." I personally own one of these stocks, and it accounts for 3% of my real-life holdings. Simply stated, we think these three are the best stocks for true long-term investors to know about, and you can uncover them for free today, instantly; just click here now.

The article Is the For-Profit Education Mess About to Repeat Itself? originally appeared on Fool.com.

Fool contributor Brian Stoffel has no position in any stocks mentioned. The Motley Fool recommends K12. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.